What crypto credit scores measure

Crypto credit scores aggregate on-chain behavior to create a probabilistic risk assessment of a wallet address. Unlike traditional FICO scores, which rely on static data points like payment history and credit utilization, crypto credit scores function as live telemetry feeds. They track interactions with decentralized finance (DeFi) protocols, collateral ratio management, and adherence to smart contract obligations.

Institutions use these scores to augment traditional inputs with on-chain data, such as wallet balances and transaction flows. This allows lenders to assess counterparty risk for unbanked or underbanked users by using verifiable digital footprints. The goal is to bridge the gap in risk assessment, rendering DeFi lending more robust by shifting the focus from "who you are" to "what you have done."

Step 1: Prepare your primary wallet

Building a valid crypto credit score in 2026 starts with data quality. Lenders and on-chain credit protocols rely on a clear, continuous history of your financial behavior. If your activity is scattered across dozens of addresses or mixed with anonymous transactions, scoring models cannot assign you a reliable reputation.

Choose a single mainnet and address

Select one primary blockchain (e.g., Ethereum, Solana, or Base) and one main address to be your "credit wallet." Use this address exclusively for activities you want to report: stablecoin payments, lending protocol interactions, and consistent transaction history. Avoid using this address for high-risk activities, airdrop farming, or interactions with known scam contracts, as these can negatively impact your on-chain reputation.

Clean up your history

Audit your current wallet before building your score. If you have a history of using mixing services, anonymous privacy tools, or frequent interactions with unverified contracts, consider creating a new address for your credit-building activities. A fresh start with a clean slate is often safer than trying to "clean" an old, messy history. Most on-chain credit models prefer to see consistent, positive behavior over a long period rather than a sudden spike in activity from a previously inactive address.

Fund and activate

Fund your primary wallet with a small amount of the native token for gas fees and a stablecoin for lending or payment history. Start by making small, regular transactions. Consistency is more valuable than volume. Lenders want to see that you can manage your finances predictably over time. This initial activity creates the baseline data needed for credit scoring algorithms to begin tracking your reliability.

Note: On-chain credit is still emerging as wallet reputation rather than a direct FICO equivalent. Your goal is to build a verifiable history of responsible behavior that protocols can trust. Reddit discussion on on-chain credit.

Choose one blockchain and one address to be your primary hub. Use this address exclusively for credit-building activities like stablecoin payments and lending. Avoid mixing high-risk or anonymous transactions in this wallet to maintain a clean reputation.

Review your current wallet for messy history, such as interactions with privacy mixers or unverified contracts. If your history is too cluttered, create a new address for your credit-building activities. A fresh start with a clean slate is often safer and more effective for scoring models.

Fund your wallet with gas tokens and stablecoins. Start making small, regular transactions to establish a baseline of reliability. Consistency over time is more valuable to lenders than large, sporadic transactions. This creates the initial data points needed for credit scoring algorithms.

Establish lending history

Building a crypto credit score 2026 requires proof that you can manage debt. Unlike traditional banking, DeFi protocols do not automatically report your behavior to Equifax or TransUnion. You must actively generate a track record of on-time repayments that third-party credit scoring engines can verify.

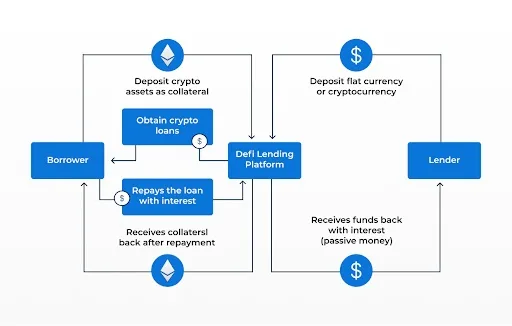

The process starts with depositing collateral—typically stablecoins or major assets like Bitcoin—into a lending protocol. You then borrow against this collateral. This creates a loan. To build your score, you must repay this loan consistently over time. Each successful repayment cycle adds positive data to your digital identity.

Choose a credit-reporting protocol

Not all lending platforms feed data into credit bureaus. You need to select a protocol that partners with a recognized crypto credit scoring agency. In 2026, the market has shifted toward specialized infrastructure. According to DefiPrime, AI-driven credit scoring in DeFi has grown significantly, with total value locked (TVL) in these credit markets surpassing $4 billion in 2025. This growth indicates that major protocols are now integrating credit reporting as a standard feature.

Look for platforms that explicitly state they report to agencies like Tally, CreditXP, or similar entities. Avoid generic lending pools that do not mention credit reporting in their documentation. Your goal is to create a public on-chain ledger of your repayment behavior.

Deposit collateral and borrow

Once you have selected a reporting-friendly protocol, deposit your collateral. Most platforms require over-collateralization, meaning you must deposit more value than you wish to borrow. For example, you might deposit $1,000 in USDC to borrow $500 in a stablecoin.

This step is not just about accessing funds; it is about creating the loan record. The protocol mints your loan and assigns it a unique identifier. This identifier is what credit agencies will later use to track your repayment history. Ensure you understand the liquidation thresholds. If the value of your collateral drops too low, the protocol will liquidate it, which can severely damage your credit score.

Repay on time and track your progress

Consistency is the core mechanic of building your crypto credit score 2026. Set up automatic payments or strict reminders to ensure you never miss a due date. Even one late payment can reset your progress or lower your score significantly.

As you repay, monitor your score through the agency’s dashboard. Many agencies provide a free tier that shows your current standing. Use this data to adjust your borrowing habits. If your score is stagnant, consider taking out a small loan and repaying it quickly to add another positive data point to your history.

Avoid common pitfalls

Do not max out your borrowing capacity. High utilization ratios can signal risk to credit algorithms. Keep your loan-to-value ratio conservative. Additionally, avoid borrowing in volatile assets unless you are prepared to manage the risk actively. Stablecoin loans are generally safer for building a clean credit history because they do not fluctuate wildly in value.

Remember, crypto-backed loans are collateral-based rather than credit-based in their initial setup. However, the repayment history you build can eventually unlock unsecured credit lines or better rates, effectively creating a traditional-style credit score from your on-chain activity.

3. Diversify protocol usage

Building a strong profile for crypto credit scores 2026 requires more than just using one platform. Relying on a single protocol creates concentration risk. If that platform experiences an exploit or a liquidity crunch, your entire on-chain history may appear unstable to scoring models.

Scoring algorithms, such as those used by AgioRatings, analyze wallet behavior and reserve composition to gauge counterparty risk. Interacting with multiple reputable lending venues signals that you are a sophisticated user who manages risk effectively. It demonstrates that your activity is consistent across the broader DeFi ecosystem, rather than dependent on a single point of failure.

Aim to distribute your lending and borrowing activity across at least three major protocols. This could include a mix of established platforms like Aave and Compound, or other reputable venues that prioritize security audits. By spreading your exposure, you provide credit bureaus with a more robust dataset of your financial habits.

This diversification helps smooth out the volatility inherent in crypto markets. When one protocol experiences a temporary dip in liquidity or a minor security scare, your activity on other platforms remains unaffected. This stability is a key factor in how institutions measure your reliability as a borrower.

| Feature | Aave | Compound | MakerDAO |

|---|---|---|---|

| Data Transparency | High (Open-source smart contracts) | High (Open-source smart contracts) | High (On-chain governance) |

| Credit Score Impact | Positive (Established track record) | Positive (Established track record) | Positive (Stablecoin issuance history) |

| Risk Profile | Low (Multi-tiered security) | Low (Audited) | Medium (Complex collateral types) |

Step 4: Verify identity selectively

Traditional credit reporting demands full Know Your Customer (KYC) disclosure, exposing your name, address, and government ID to every lender. For building crypto credit scores 2026, this creates a privacy risk that Zero-Knowledge Proofs (ZKPs) are designed to eliminate.

ZKPs allow you to prove you meet specific credit criteria without revealing the underlying data. Instead of sharing your entire financial history, you generate a cryptographic proof that confirms you are over 21, have a stable income, or have never defaulted, while keeping the actual numbers private.

This selective verification is the bridge between DeFi lending and institutional risk assessment. As noted by researchers at the Cardozo Law Review, crypto-native credit scoring aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive without forcing total transparency.

By using decentralized identity protocols, you maintain control over your data. You only share what is necessary for the credit check, preserving your privacy while establishing a verifiable reputation on-chain.

No comments yet. Be the first to share your thoughts!