Get DeFi Credit Scoring 2026 Right

Before you deposit funds or request a loan, you need to understand how on-chain reputation actually works. Unlike traditional credit scores, which rely on a few centralized bureaus, DeFi credit scoring aggregates your entire blockchain history. This transparency is powerful, but it also means every transaction is permanent. If you approach this without a clear strategy, you risk locking capital in inefficient protocols or damaging your reputation score through accidental defaults.

Follow these steps to build a strong on-chain reputation.

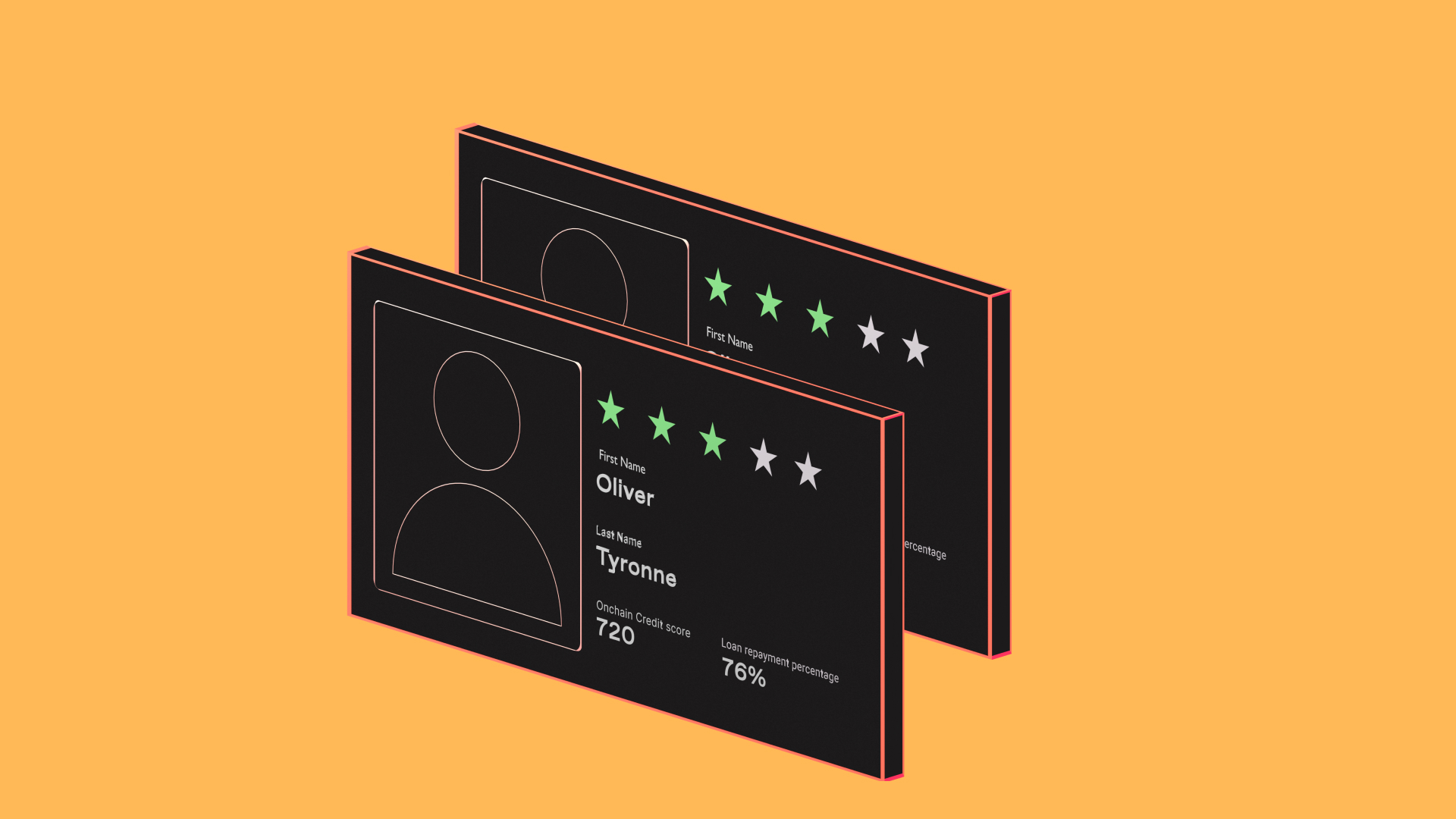

Choose a protocol that aggregates your on-chain activity. Platforms like ChainAware or Credix scan your wallet for transaction history. Connect your wallet carefully. Review the permissions you are granting. Most protocols only need read access to your public address. They do not need private keys or the ability to spend your funds. Ensure the protocol is reputable and audited before connecting.

Reputation systems need data. If your wallet is empty, the algorithm has nothing to score. Deposit stablecoins like USDC or major assets like ETH. These assets are widely recognized by credit scoring models. Avoid holding only obscure or volatile tokens. A balanced portfolio shows financial stability. The system uses these holdings as proof of net worth and liquidity.

This is the most critical step. You must borrow money to prove you can repay it. Start with a small amount that you can easily afford to return. Choose a short duration, such as 30 days. This minimizes your risk while maximizing the signal you send to the protocol. A successful loan creates a positive data point in your history. It shows the system that you are a low-risk borrower.

Never miss a payment. On-chain credit scores are unforgiving. If you default, your score drops significantly, making future borrowing expensive or impossible. Pay back the principal and interest before the deadline. If you can, repay early. Early repayment is a strong positive signal. It demonstrates discipline and financial strength. This single action can boost your score more than any other factor.

One good loan is not enough. You need a track record. Continue to use the protocol for lending, borrowing, or providing liquidity. Consistency builds trust. The longer your history, the more accurate your score becomes. Avoid large, erratic withdrawals that suggest instability. Keep your wallet active and your behavior predictable. Over six to twelve months, your on-chain credit score will solidify.

Fix common mistakes

On-chain reputation systems are unforgiving because they lack the chargeback protections of traditional banking. A single misstep in how you structure your protocol interactions can permanently damage your credit score or lock your capital. Most borrowers fail not because they lack assets, but because they misunderstand the technical requirements of the lending platform.

Ignoring the health factor buffer

The most frequent error is borrowing up to the absolute maximum limit. Protocols calculate a health factor to ensure the loan remains solvent if collateral prices drop. If you borrow 100% of the allowable limit, even a 1% dip in your asset’s price can trigger an immediate liquidation.

Always maintain a health factor above 1.5. This buffer gives your position room to breathe during normal market volatility. Think of it as a safety margin; if your health factor drops below 1.0, the protocol will sell your collateral to cover the debt, often at a loss.

Overlooking protocol-specific rules

Not all DeFi lending platforms treat collateral the same way. One protocol might accept a specific NFT collection as 50% collateral, while another rejects it entirely or values it at 0%. Assuming your reputation score transfers seamlessly across platforms is a dangerous assumption.

Before depositing assets, check the specific collateral factors for each platform. Some protocols also require you to hold a native governance token to access lower interest rates. Failing to hold these tokens means paying higher fees, which eats into your returns and can indirectly affect your repayment capacity.

Using unstable collateral

High volatility is the enemy of on-chain credit. Using assets like meme coins or low-liquidity altcoins as collateral is a fast track to liquidation. These assets can swing 20% or more in a single hour, leaving no time to react.

Stick to established assets with deep liquidity, such as Bitcoin, Ethereum, or major stablecoins. Stablecoins are generally safer for maintaining a consistent health factor, but be aware of de-pegging risks. Never use assets you cannot afford to lose instantly, as the liquidation process is automated and immediate.

DeFi credit scoring 2026: what to check next

On-chain reputation systems are changing how lenders assess risk, but they introduce new trade-offs for borrowers. Before integrating these tools into your financial strategy, it helps to understand the practical limitations and security realities of 2026’s credit scoring landscape.

Understanding these nuances ensures you can manage your decentralized finance portfolio with confidence and clarity.

No comments yet. Be the first to share your thoughts!