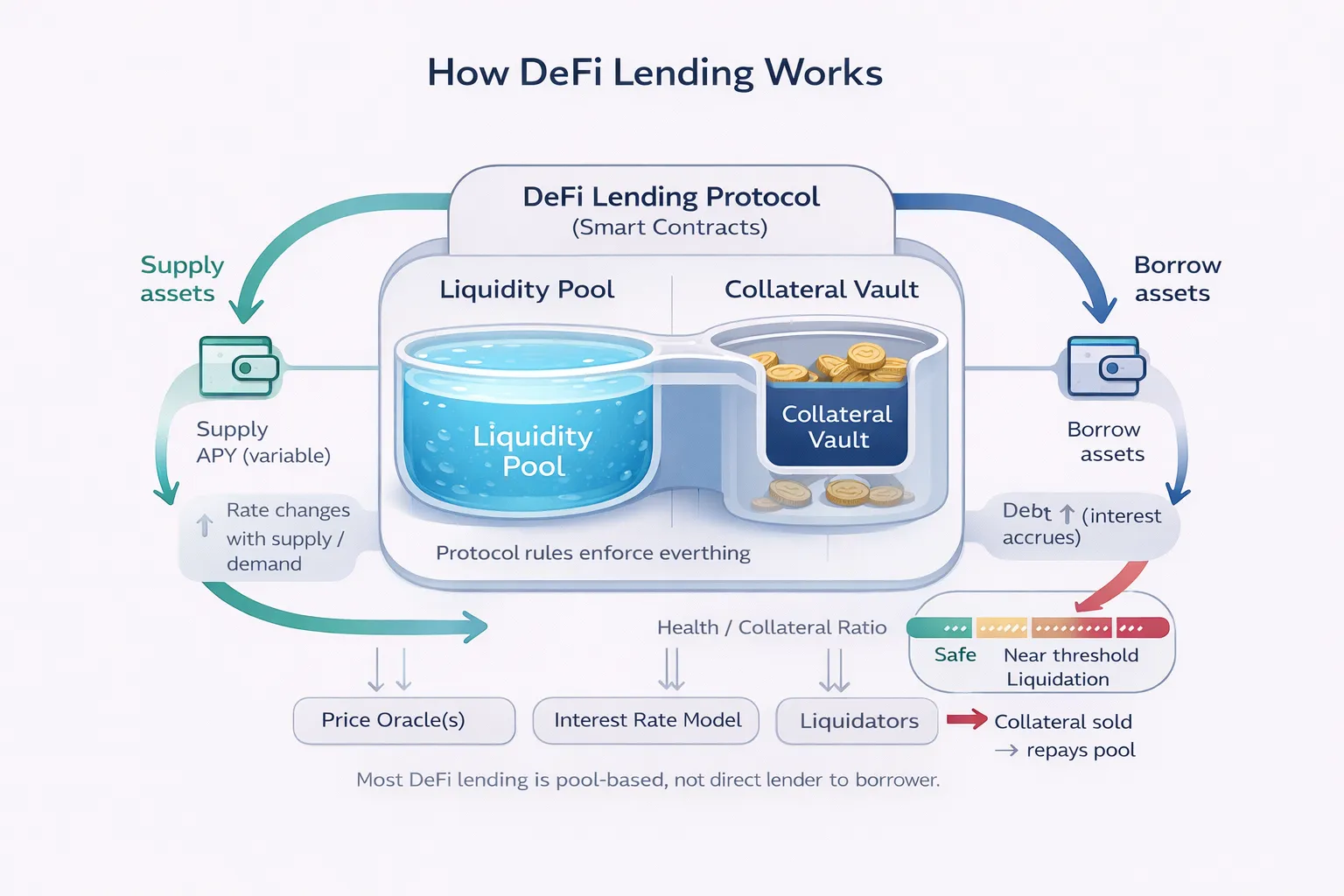

How on-chain credit scoring works

Traditional credit scoring relies on private bureau reports and historical debt repayment data, a system that excludes billions of unbanked individuals. Crypto credit scores 2026 shift this paradigm by treating the blockchain as a public ledger of financial behavior. Instead of waiting for a monthly statement, protocols now analyze wallet-based reputation systems in real time, assessing counterparty risk through transparent, immutable data points.

The foundation of this system is the analysis of wallet balances and flows. Institutions and decentralized finance (DeFi) protocols examine reserve composition and transaction behavior to gauge stability. A wallet that maintains consistent liquidity and avoids erratic large transfers is viewed as lower risk than one exhibiting speculative volatility. This data-driven approach allows for a more nuanced assessment of financial health than a simple credit limit.

Transaction history further refines this risk model. By tracking the frequency, size, and counterparties of past interactions, scoring algorithms can predict future reliability. This method bridges the gap in risk assessment, rendering DeFi lending more robust and inclusive for users who lack traditional credit history. The result is a dynamic reputation score that grows with every verified on-chain action.

DeFi lending market trends in 2026

The landscape of crypto credit scores 2026 is defined by a decisive shift toward decentralized finance. By the end of the first quarter of 2026, decentralized lending venues captured 52.6% of the market, surpassing centralized finance (CeFi) platforms for the first time in a sustained manner. This milestone, down slightly from 54.3% in late 2025, signals a structural change in how capital is allocated and risk is assessed, moving away from traditional custodial models toward on-chain transparency.

This dominance is fueled by the rapid expansion of the crypto-collateralized lending market, which reached $53 billion by mid-2025 according to Galaxy Research. The growth is not merely speculative; it reflects a maturing infrastructure where protocols like Aave and Compound serve as primary liquidity hubs. As on-chain reputation becomes the standard for underwriting, these platforms are integrating complex credit mechanisms that allow users to borrow against their historical behavior rather than just over-collateralizing every position.

The rise of tranched credit markets further illustrates this evolution. By slicing risk into different layers, DeFi protocols can offer lower borrowing costs to highly reputable users while maintaining safety margins for the system. This granular approach to risk management is essential for the scalability of crypto credit scores, enabling institutions to participate with confidence. The market is no longer just about moving assets; it is about building a reliable, auditable history of financial responsibility.

How credit models differ across protocols

The infrastructure behind crypto credit scores 2026 relies on two distinct methodologies: traditional overcollateralization and emerging uncollateralized on-chain reputation. Overcollateralized protocols, such as Aave and Compound, function similarly to secured bank loans. Borrowers must lock up more digital assets than the value they wish to borrow, effectively using their wallet balances as collateral to mitigate lender risk. This model prioritizes capital preservation over accessibility, ensuring that smart contract failures or market volatility do not leave lenders underfunded.

In contrast, uncollateralized lending models rely on wallet history and behavioral data to assess counterparty risk. These systems analyze transaction flows, reserve composition, and long-term holding patterns to assign a credit score. This approach aims to bridge the gap in risk assessment, rendering DeFi lending more inclusive by allowing borrowers with lower asset bases but strong transactional histories to access capital. However, it introduces new complexities in verifying identity and preventing Sybil attacks.

The following comparison outlines the structural differences between these two primary approaches to credit scoring in decentralized finance.

| Model Type | Collateral Requirement | Credit Assessment Method | Primary Risk Factor |

|---|---|---|---|

| Overcollateralized | >100% of loan value | Asset price and liquidity depth | Market volatility and liquidation cascades |

| Uncollateralized (Reputation) | None or minimal | Wallet history, flows, and on-chain behavior | Counterparty default and identity verification |

| Hybrid/Undercollateralized | <100% but >0% | Blended algorithmic scoring and partial assets | Algorithmic errors and oracle manipulation |

Institutional adoption of these models dictates the stability of the broader market. As noted by Agio Ratings, crypto credit ratings augment traditional inputs with on-chain data, such as wallet balances and flows, to measure counterparty risk more accurately. This shift from pure asset-backed security to behavioral-based credit scoring marks a significant evolution in how digital assets are leveraged.

Regulatory risks and institutional adoption

The regulatory landscape for crypto credit scores 2026 is defined by a tension between traditional banking safeguards and the unique mechanics of on-chain finance. Institutions are currently recalibrating their risk frameworks to navigate a high-stakes environment where regulatory clarity is evolving faster than legacy compliance tools can adapt. This shift is not merely about adherence; it is about survival for lenders integrating digital assets into their balance sheets.

A pivotal development in this space is the White House’s 2026 research on stablecoin yield prohibitions. The study indicates that banning yield on stablecoins could increase bank lending by $2.1 billion, albeit with a net welfare cost of $800 million. This suggests that regulatory restrictions on DeFi yield structures may inadvertently push capital back toward traditional banking channels, altering the risk profile of crypto-backed loans. Lenders must now account for these macro-level shifts when underwriting crypto credit, as the cost of capital and liquidity availability are directly tied to these policy outcomes.

To manage these risks, institutions are augmenting traditional credit inputs with on-chain data. As noted by Agio Ratings, crypto credit ratings now incorporate wallet balances, reserve composition, and transaction behavior. This data allows lenders to assess counterparty risk in real-time, providing a layer of transparency that traditional credit scores lack. The integration of these on-chain metrics is becoming a standard requirement for institutional-grade crypto credit, ensuring that risk assessments are both comprehensive and current.

As regulatory frameworks solidify, the institutions that successfully integrate these on-chain reputation signals will gain a competitive advantage. The ability to accurately price risk using real-time blockchain data will become a key differentiator in the crypto credit market. For borrowers, this means that maintaining a clean on-chain history is no longer optional—it is a critical component of accessing favorable lending terms in 2026.

Frequently asked questions about on-chain credit

How do crypto credit scores differ from traditional FICO scores?

On-chain credit does not replicate the traditional FICO model. Instead of relying on historical debt repayment or income verification, on-chain credit scores are derived from wallet reputation and transaction history. This approach removes traditional barriers such as credit scores and lengthy approval processes, allowing borrowers to access capital based on asset behavior rather than identity.

Will crypto credit scores replace traditional banking credit?

It is unlikely that on-chain credit will fully replace traditional banking credit in the near term. Current models are primarily collateral-based rather than credit-based. For example, borrowing against Bitcoin relies on the asset's value as security rather than the borrower's creditworthiness. This distinction limits the scope of on-chain credit to specific use cases rather than broad consumer lending.

What is the future trajectory of crypto credit in 2026?

In 2026, the gap between institutional and retail crypto services is expected to widen, particularly regarding privacy and data access. While stablecoins are projected to reach significant market caps, the integration of credit scores remains fragmented. On-chain reputation systems are emerging, but they operate independently of the centralized financial infrastructure that defines traditional credit.

No comments yet. Be the first to share your thoughts!