Defining crypto credit scores 2026

The concept of a crypto credit score 2026 marks a structural shift in how financial risk is evaluated within decentralized finance. Unlike traditional FICO-style scoring models that rely on private financial records and legal identity verification, these systems measure counterparty risk through transparent, immutable data. This approach allows lenders to assess the reliability of a wallet address based on its historical behavior rather than the individual's real-world identity.

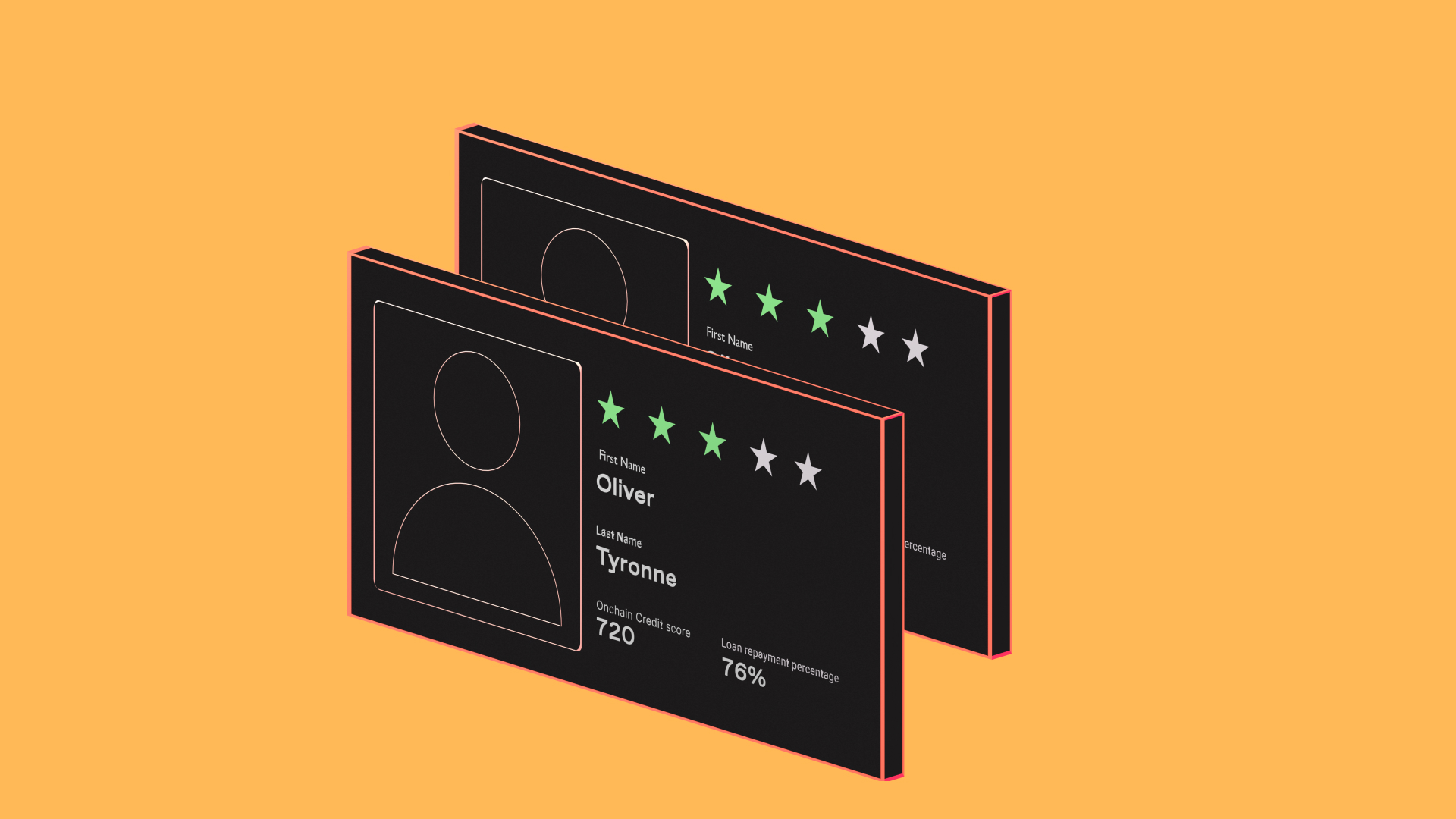

These scores are built on a foundation of on-chain analytics. As noted by industry analysts, crypto credit ratings augment traditional inputs with specific wallet data, including balance history, transaction flows, reserve composition, and overall transaction behavior. This data provides a clear, auditable trail of how an entity interacts with the blockchain, offering a level of transparency that off-chain credit bureaus cannot match.

The primary objective of these systems is to address the gap in risk assessment, rendering DeFi lending more robust and inclusive. By focusing on wallet behavior and historical performance, protocols can determine lending limits and interest rates without requiring the user to reveal personal identifiable information. This method prioritizes financial conduct over legal identity, creating a new standard for trust in digital asset markets.

This shift does not replace legal compliance but operates alongside it. The data used to generate these scores is public by nature, meaning that any wallet activity is visible to the network. This visibility allows for the creation of a "crypto-native credit score" that aims to make decentralized lending more accessible to users who may lack traditional credit histories but demonstrate responsible financial behavior on-chain.

How on-chain credit history works

Institutional risk assessment in decentralized finance relies on transparent, immutable ledger data rather than traditional credit bureau reports. Unlike centralized finance, where creditworthiness is often obscured by opaque reporting mechanisms, on-chain reputation is derived directly from wallet behavior. Agioratings notes that crypto credit ratings augment standard inputs with on-chain data, such as wallet balances, fund flows, reserve composition, and transaction behavior [1]. This transparency allows lenders to verify asset solvency and counterparty reliability in real time.

The mechanics of these crypto credit scores 2026 models prioritize three core metrics: liquidity depth, transaction frequency, and repayment discipline. A wallet holding substantial, stable assets relative to its debt load demonstrates lower default risk. Frequent, consistent transaction history provides a longer data set for statistical analysis, reducing the noise associated with sporadic trading activity. Most critically, the history of on-time repayments on decentralized loans serves as the primary indicator of future reliability.

This data-driven approach aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive for participants lacking traditional financial identities [2]. By quantifying reputation through code and transactions, the ecosystem creates a verifiable credit history that can be audited by any party, establishing a new standard for counterparty risk in digital assets.

Collateral-only lending vs reputation-based models

The traditional DeFi lending framework relies on over-collateralization. Borrowers must lock digital assets—often at a 150% to 200% ratio—to secure a loan. This model removes the need for identity verification but ties up capital that could otherwise be deployed. As noted in industry analyses, crypto-backed loans are fundamentally collateral-based rather than credit-based, effectively bypassing traditional credit checks but limiting access for users without significant liquid assets [src-serp-2].

Reputation-based lending, often facilitated through tranched credit markets, introduces a new variable: on-chain history. In this model, protocols analyze transaction patterns, repayment behavior, and wallet age to assign a risk score. This allows for under-collateralized or even unsecured loans. The growth of these markets, which saw outstanding loans rise 37% in 2025, signals a shift toward institutional-grade credit assessment in decentralized finance [src-serp-7].

The following comparison highlights the structural differences between these two approaches.

| Metric | Collateral-Only | Reputation-Based |

|---|---|---|

| Required Collateral | High (150-200%+) | Low or None |

| Approval Speed | Instant | Minutes to Hours |

| Capital Efficiency | Low | High |

| Identity Requirement | None (Pseudonymous) | Often Required |

| Risk Assessment | Asset Price | On-Chain History |

For users with strong on-chain history, reputation-based models offer superior capital efficiency. Instead of locking up $200 of Bitcoin to borrow $100, a borrower with a verified high credit score might access the same liquidity with minimal collateral. This shift is central to the evolution of crypto credit scores 2026, moving the industry from pure asset-backed security toward nuanced, behavior-based risk pricing.

Market trends in on-chain credit

The landscape for crypto credit scores 2026 is defined by a shift toward institutional-grade structures. Galaxy Research data from Q1 2026 indicates that DeFi lending app dominance over CeFi venues stood at 52.6%, down 183 basis points from the end of Q4 2025 [src-serp-4]. This contraction reflects regulatory pressures and security audits rather than a collapse in demand.

Simultaneously, DeFi outstanding loans grew 37% in 2025, driven largely by real-world asset (RWA) tokenization and institutional yield requirements [src-serp-7]. The market is moving away from simple over-collateralized loans toward tranched credit structures, which allow for more nuanced risk assessment. This evolution supports the development of more sophisticated on-chain reputation systems.

The integration of these complex lending instruments requires robust credit scoring models. As protocols adopt tranched credit, the ability to accurately score on-chain behavior becomes a critical infrastructure component. This shift is essential for maintaining stability in high-stakes financial environments.

Legal and regulatory risks in crypto credit scores 2026

The shift toward on-chain reputation systems introduces significant legal ambiguities. Unlike traditional banking, where credit reporting is governed by the Fair Credit Reporting Act (FCRA) and strict data privacy laws, decentralized finance (DeFi) operates in a regulatory vacuum. This lack of oversight means that the mechanisms used to calculate crypto credit scores 2026 are largely unstandardized and unverified by independent auditors.

This transparency creates a dual-edged sword. While it allows for more inclusive risk assessment, as noted by legal scholars like Nizan Geslevich Packin, it also exposes users to permanent financial profiling. There is no "right to be forgotten" in immutable blockchain ledgers. If a protocol misinterprets your transaction history or if your wallet is linked to illicit activity, your reputation score may be permanently damaged without a clear recourse for appeal.

Additionally, the legal status of on-chain credit contracts remains unsettled. Courts have yet to establish clear precedents for enforcing smart contract-based lending agreements when disputes arise. This uncertainty increases the risk for both lenders and borrowers, as traditional legal protections may not apply to decentralized protocols. As on-chain credit markets become a major trend in 2026, participants must navigate these unresolved legal waters with caution.

Building your on-chain reputation

Improving your crypto credit scores 2026 requires treating digital assets with the same discipline as traditional finance. Unlike centralized systems, on-chain reputation is transparent and immutable. You build this history through consistent repayment, diversified wallet activity, and engagement with reputable protocols. Institutional risk assessment relies heavily on these verifiable signals to gauge counterparty reliability.

Settle all loans and lending positions on time. Payment history is the strongest predictor of future behavior. Late payments or defaults are permanently recorded on the blockchain, severely limiting your access to future capital.

Maintain a healthy mix of assets and transaction types. Institutional models analyze wallet balances, reserve composition, and transaction flows to assess stability. A diversified portfolio signals lower risk than a single-asset dependency.

Engage only with protocols that have undergone rigorous security audits. Reputable platforms provide transparent data feeds for credit scoring. Interacting with unverified or unaudited contracts introduces unnecessary counterparty risk that can negatively impact your credit profile.

Crypto-native credit scoring aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive for users who maintain a strong on-chain identity. By adhering to these principles, you establish a verifiable track record that institutions can trust.

Common questions about on-chain credit

The landscape of crypto credit scores 2026 is shifting from experimental protocols to regulated financial infrastructure. While traditional credit bureaus remain the standard for fiat lending, on-chain reputation systems are gaining traction as a primary mechanism for DeFi borrowing. These scores leverage transaction history, collateralization ratios, and wallet age to assess risk without exposing personally identifiable information.

Can I use my crypto credit score for traditional loans?

Currently, most centralized banks do not recognize on-chain reputation scores for conventional mortgage or auto loans. However, hybrid financial institutions are beginning to integrate blockchain data into their underwriting processes. A robust on-chain history can serve as supplementary evidence of financial stability, potentially improving approval odds in niche lending markets that bridge TradFi and DeFi.

How are crypto credit scores calculated differently?

Unlike FICO scores, which rely heavily on debt-to-income ratios and payment history on fiat accounts, crypto credit scores prioritize wallet longevity, consistent collateralization, and smart contract interaction frequency. A user who maintains a healthy loan-to-value ratio across multiple DeFi protocols demonstrates reliability. These metrics are transparent and verifiable on-chain, offering a different risk profile than traditional credit reports.

Is my on-chain data private?

On-chain reputation systems are designed to be pseudonymous. They analyze transaction patterns and wallet behavior without linking directly to your real-world identity. This approach aligns with regulatory requirements for data minimization. You retain control over which protocols can view your credit score, ensuring that your financial history remains accessible only to authorized lending platforms.

No comments yet. Be the first to share your thoughts!