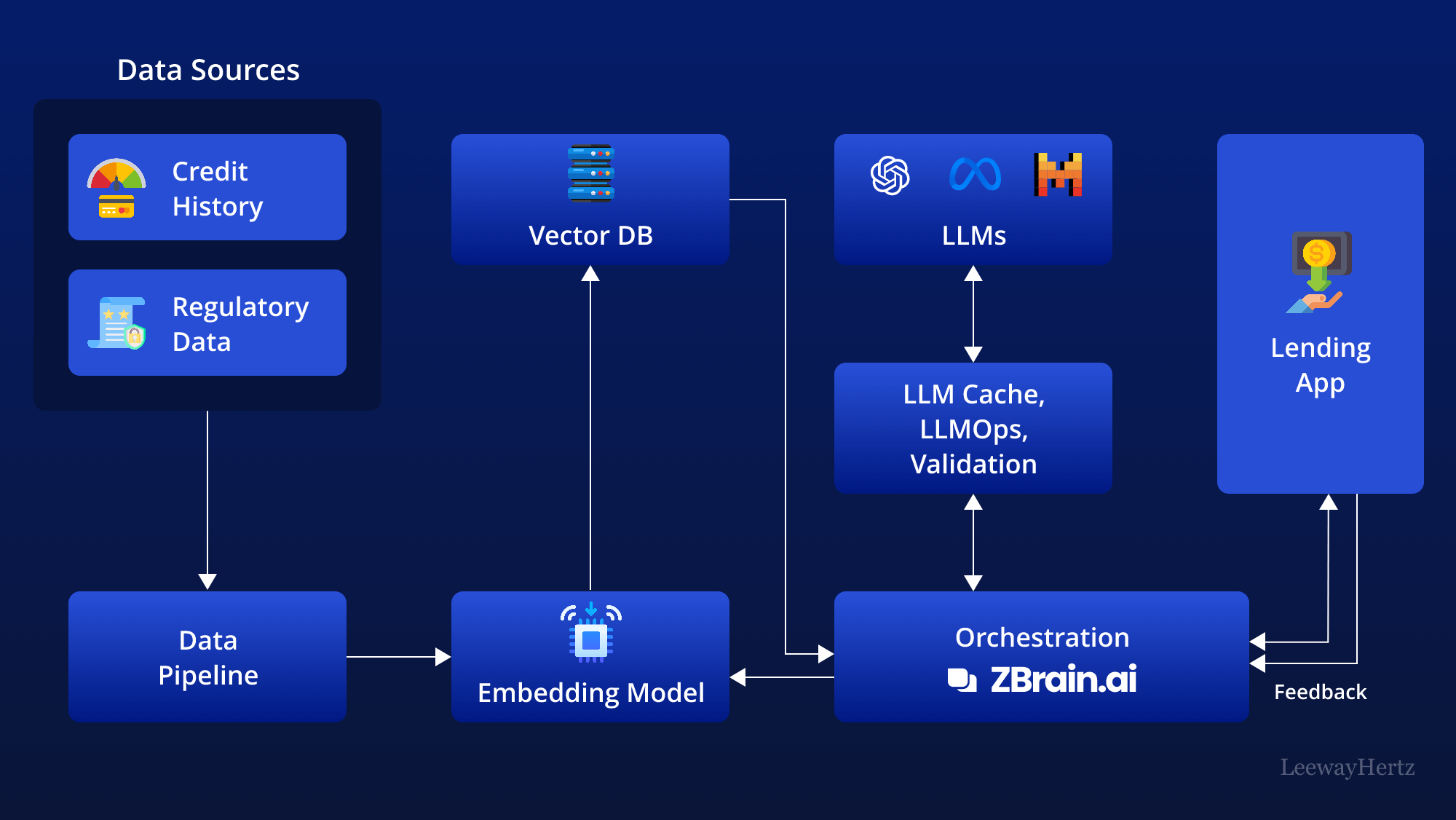

How AI Credit Scoring Crypto Works in 2026

AI-driven credit scoring crypto models are moving beyond static FICO scores to analyze real-time on-chain behavior. In 2026, lenders use alternative data points—like consistent DeFi repayments, wallet age, and stablecoin holdings—to assess risk. This shift allows for faster approvals and more personalized loan terms, particularly for borrowers with thin traditional credit files.

The data shows organizations using AI credit scoring achieve 15–25% better accuracy compared to traditional methods. Decisions that once took days now happen in minutes. However, this speed comes with tradeoffs. While AI can spot errors and help improve your credit score by identifying reporting issues, it also introduces new risks around algorithmic bias and data privacy that borrowers must understand before signing.

| Feature | Traditional Credit Scoring | AI-Driven Crypto Scoring |

|---|---|---|

| Data Source | Bureau reports, payment history | On-chain transactions, DeFi history |

| Speed | Days to weeks | Minutes to hours |

| Accuracy | Static, historical view | Dynamic, real-time risk assessment |

| Access | Limited to credit history | Includes alternative financial data |

For crypto-native borrowers, this means your wallet activity is now your collateral. Lenders are increasingly looking at your ability to repay through consistent on-chain behavior rather than just your past credit history. This creates a more inclusive lending environment but requires you to maintain a clean and verifiable on-chain record.

Ai credit scoring crypto choices that change the plan

AI-driven credit scoring for crypto loans shifts the evaluation from static FICO history to dynamic behavioral data. Lenders now analyze on-chain transaction patterns, wallet age, and DeFi interaction frequency to assess risk in minutes rather than days. This speed comes with distinct tradeoffs regarding privacy, model bias, and regulatory clarity that borrowers must weigh before applying.

The primary advantage is accessibility. Traditional underwriting often rejects borrowers with thin credit files or volatile income, common in crypto-native communities. AI models can identify creditworthiness through consistent repayment behavior on decentralized platforms, even if that activity is invisible to Equifax or Experian. This allows for personalized loan terms that reflect actual risk rather than historical averages.

However, this shift introduces complexity. On-chain data is public, meaning your financial history is permanently visible to anyone. While AI models use pseudonymous addresses, the linkage between real-world identity and wallet activity can create privacy risks. Additionally, algorithms trained on limited or biased datasets may inadvertently penalize users from specific geographic regions or those using newer, less common DeFi protocols.

Key Tradeoffs to Evaluate

| Factor | Traditional FICO | AI-Driven Crypto Scoring |

|---|---|---|

| Data Source | Credit bureaus, loan history | On-chain transactions, wallet age |

| Decision Time | Days to weeks | Minutes to hours |

| Privacy | Limited access to bureau data | Public ledger visibility |

| Bias Risk | Historical systemic bias | Algorithmic training bias |

| Accessibility | Requires established credit | Open to crypto-native users |

When AI Scoring Makes Sense

AI credit scoring is most beneficial for borrowers with limited traditional credit history but active, responsible participation in crypto markets. If you regularly repay DeFi loans or maintain a long-standing, low-risk wallet history, AI models may offer you better rates than traditional lenders who see a "thin file." It also suits those who need immediate liquidity and cannot wait for manual underwriting.

Conversely, stick to traditional lending if you have a strong FICO score and value privacy. Traditional lenders do not require you to expose your entire transaction history. If you are uncomfortable with the permanence of on-chain data or the opacity of black-box AI decisions, the slower, more transparent traditional process may provide greater peace of mind.

Making the Decision

Choose AI-driven scoring if speed and access are your priorities and you are comfortable with public ledger transparency. Opt for traditional lending if you have an established credit profile, prioritize privacy, or prefer the regulatory protections associated with regulated banks. Always compare the annual percentage rate (APR) and hidden fees, as AI lenders may charge higher premiums for the speed and convenience they offer.

How to choose the right AI credit model for crypto loans

AI-driven credit scoring is no longer experimental. Organizations using these models achieve 15–25% better accuracy than traditional methods, processing decisions in minutes rather than days [src-serp-1]. For crypto lenders, this speed is critical, but choosing the right model requires balancing speed, cost, and regulatory exposure.

The shift is moving from static historical data to real-time risk modeling. AI enables lenders to assess repayment ability independent of traditional FICO scores, offering clarity on borrowers who may lack credit history but have strong cash flow patterns [src-serp-2]. This creates a new tier of eligible borrowers, but it also introduces new risks around bias and data security.

To navigate this, lenders should follow a structured decision framework. This approach ensures that the chosen AI model aligns with your specific risk appetite and operational capacity.

AI models are only as good as the data they ingest. Before selecting a provider, audit your internal data pipelines. Are you capturing on-chain transaction history, off-chain income verification, or both? Poor data quality leads to model drift. Ensure your data is clean, consistent, and compliant with privacy regulations before training or selecting a model.

Not all AI models are built for the same trade-offs. High-frequency trading platforms need millisecond decisions, while mortgage-style crypto loans require deeper due diligence. Determine your acceptable loss ratio and the maximum time a borrower should wait for an answer. This defines whether you need a lightweight heuristic model or a complex neural network.

Black-box models are risky in regulated finance. Choose AI systems that offer explainability features, allowing you to see why a loan was approved or denied. This is crucial for regulatory compliance and customer trust. Ensure the model has been tested for bias against specific demographics or transaction types to avoid discriminatory lending practices.

Do not roll out a new AI model to your entire user base at once. Start with a small, controlled group of borrowers. Monitor the model’s performance against actual repayment outcomes. Compare the AI’s decisions with traditional underwriting to identify discrepancies. Use this pilot data to refine thresholds and adjust the model’s parameters before scaling.

Crypto markets are volatile, and borrower behavior changes. An AI model that worked last quarter may fail this one. Establish a continuous monitoring system to track key metrics like default rates and approval accuracy. Retrain the model regularly with new data to ensure it adapts to changing market conditions and remains accurate over time.

By following these steps, you can implement AI credit scoring that is both efficient and responsible. The goal is not just speed, but sustainable growth through better risk assessment.

Spotting Misleading Claims in AI Credit Scoring

The promise of AI-driven credit scoring in 2026 is faster crypto loan approvals, but the marketing often outpaces the reality. While some platforms claim 15–25% better accuracy than traditional models, this figure relies on specific, controlled datasets that rarely reflect the chaotic nature of crypto markets [[src-serp-1]]. You must distinguish between tools that simply automate existing checks and those that genuinely analyze alternative data streams. Many "AI" lenders are just using basic algorithmic filters, offering no real advantage over legacy systems while charging higher fees for the novelty.

A common mistake is assuming AI can directly boost your FICO score. It cannot. AI helps you spot errors on your credit report and manage debt repayment more efficiently, which indirectly improves your score over time [[src-serp-2]]. However, some platforms misleadingly suggest their models can instantly inflate your creditworthiness. In reality, AI provides lenders with real-time risk insights independent of FICO history, allowing for approvals based on cash flow and on-chain behavior rather than past credit mistakes [[src-serp-2]].

Be wary of platforms that hide their data sources. True AI credit scoring relies on transparent, diverse datasets, including utility payments and blockchain history. If a lender cannot explain how their model weighs these factors, it is likely relying on outdated or biased data. Always verify that the AI tool is being used for genuine risk assessment, not just as a sales tactic to approve high-risk borrowers without proper due diligence.

Ai credit scoring crypto 2026: what to check next

AI credit scoring in 2026 moves beyond static credit history to analyze real-time transactional data. This shift allows lenders to assess crypto borrowers more accurately, often leading to faster approvals and personalized loan terms that traditional FICO scores miss. However, understanding the mechanics helps you prepare for these dynamic evaluations.

No comments yet. Be the first to share your thoughts!