What Is a DeFi Credit Score?

A DeFi credit score is a risk assessment metric generated from your on-chain history rather than a traditional bank report. Instead of relying on a FICO score or a centralized identity, these protocols analyze your transaction patterns, collateral behavior, and repayment consistency across decentralized exchanges and lending platforms. This approach aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive for users without traditional credit histories.

The system works by aggregating data from multiple blockchains to create a "crypto-native credit score." This score helps lenders determine how much you can borrow and at what interest rate. It operates on transparency and open markets, allowing anyone to verify the underlying data while maintaining privacy through zero-knowledge proofs where applicable. This shift moves creditworthiness from a static, institution-controlled number to a dynamic, user-owned asset.

However, the landscape is still maturing. Unlike traditional credit, where a missed payment immediately hits a central bureau, DeFi scoring often relies on smart contract logic. If you fail to repay a loan, your collateral is liquidated automatically, but this event may or may not negatively impact your score depending on the specific protocol’s rules. Understanding these mechanics is essential before borrowing, as the penalties for default can be immediate and irreversible, unlike the grace periods often found in traditional banking.

Defi credit scores choices that change the plan

Building a credit profile in decentralized finance requires balancing liquidity, privacy, and cost. Unlike traditional banking, where income verification often dictates your score, DeFi protocols rely on on-chain behavior. This shift offers greater access but introduces specific risks that borrowers must evaluate before locking up capital.

Liquidity vs. Capital Efficiency

The most significant tradeoff involves the amount of collateral you must post. High loan-to-value (LTV) ratios improve capital efficiency but increase your risk of liquidation during market volatility. Protocols like Aave and Compound use dynamic LTVs that adjust based on asset volatility. If you hold illiquid assets, you may need to lock significantly more value to secure the same loan amount compared to stablecoins.

Privacy vs. Reputation Building

Traditional DeFi lending is pseudonymous; your transaction history is public, but your identity is not. Newer "credit-native" protocols aim to link on-chain activity to verifiable identities or decentralized identifiers (DIDs). This allows for non-collateralized loans based on reputation. However, this approach sacrifices the anonymity inherent to early crypto culture. You must decide if building a portable credit score is worth exposing your transaction history to potential data aggregators.

Cost vs. Speed

Credit scores in DeFi are not static. They update with every transaction, but the speed of this update varies. Real-time scoring protocols offer faster access to better rates but may require more frequent gas fees for verification transactions. Older models that batch updates save on gas costs but delay access to improved loan terms. For short-term trading, the speed of score updates matters more than the absolute rate. For long-term holding, the cost of maintaining an active reputation profile is the primary concern.

Key Factors to Evaluate

When selecting a protocol, look beyond the advertised interest rate. Consider the following factors:

- Liquidation Thresholds: How much can the asset price drop before you lose your collateral?

- Update Frequency: How often does your credit score refresh? Real-time or daily?

- Asset Support: Does the protocol accept your specific collateral type?

- Reputation Portability: Can you use your score across multiple lending platforms?

| Protocol | Collateral Type | Max LTV | Privacy Level | Score Update |

|---|---|---|---|---|

| Aave V3 | Over-collateralized | 82% | Pseudonymous | Per-transaction |

| Compound V3 | Over-collateralized | 80% | Pseudonymous | Per-transaction |

| Kava Lend | Multi-asset | 75% | Pseudonymous | Batched |

| Goldfinch | Un-collateralized | N/A | Identity-linked | Periodic |

How to evaluate DeFi credit protocols

Traditional credit bureaus ignore on-chain history. DeFi credit protocols solve this by aggregating wallet activity into a verifiable score. This shift moves lending from collateral-heavy models to risk-based assessments, but it requires a different evaluation framework.

Use this decision matrix to assess protocol reliability. Focus on data transparency, oracle integrity, and regulatory alignment. These three pillars determine whether a protocol’s score reflects true creditworthiness or just temporary liquidity.

Check which blockchains and wallets the protocol indexes. Reputable systems pull from multiple chains (Ethereum, Solana, Arbitrum) to prevent score manipulation. If a protocol only looks at one chain, it misses cross-chain liabilities that could trigger insolvency.

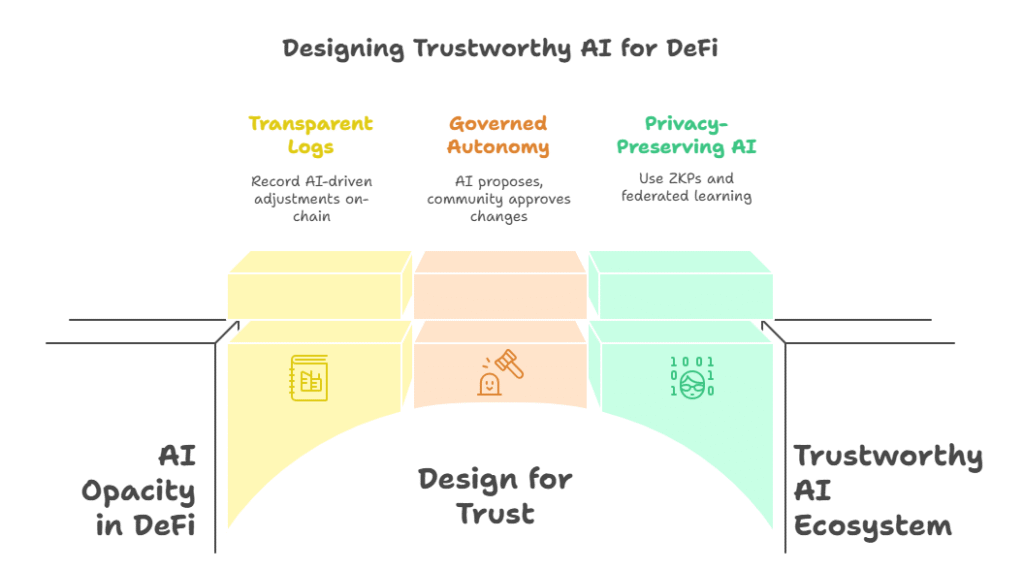

Look for open-source logic or third-party audits. The algorithm should weigh repayment history, debt-to-income ratios, and transaction frequency. Avoid protocols that use proprietary, black-box AI models without clear risk parameters.

Credit scores depend on real-time price feeds for collateral valuation. Ensure the protocol uses decentralized oracles (like Chainlink) rather than single-source feeds. Oracle failures can instantly liquidate positions or inflate credit limits.

Verify if the protocol adheres to KYC/AML standards where required. Non-compliant protocols face higher shutdown risks. Look for partnerships with regulated entities or clear legal frameworks in their jurisdiction of operation.

A reliable score should be easy to view and dispute. Check if the dashboard allows users to see exactly how each transaction impacts their score. Poor documentation or hidden fees often signal underlying structural weaknesses.

| Metric | Ideal Standard | Red Flag |

|---|---|---|

| Data Source | Multi-chain, verified wallets | Single-chain, unverified |

| Algorithm | Open-source, audited | Proprietary, black-box |

| Oracles | Decentralized (e.g., Chainlink) | Single-source feeds |

| Compliance | KYC/AML aligned | Anonymous, unregulated |

Spotting Weak DeFi Credit Options

The promise of "crypto-native credit scores" often masks protocols with opaque scoring models or insufficient liquidity. Before committing funds, verify that the scoring mechanism is transparent and audited. Look for protocols that explicitly define how on-chain activity translates to borrowing power. If the logic is buried in proprietary AI claims without open-source verification, treat it as a high-risk option.

Many new platforms overstate their risk mitigation capabilities. Check if the protocol uses real-time data feeds or relies on stale snapshots. A robust system adjusts limits based on current market volatility, not just historical balances. Avoid protocols that require excessive collateralization ratios without offering clear incentives for good behavior. The best options balance accessibility with strict, transparent risk parameters.

| Feature | Strong Protocol | Weak Option |

|---|---|---|

| Scoring Transparency | Open-source logic | Proprietary AI black box |

| Data Freshness | Real-time oracles | Daily or weekly snapshots |

| Collateral Flexibility | Dynamic LTV adjustments | Fixed, high ratios |

Defi credit scores: common: what to check next

Understanding how decentralized finance evaluates creditworthiness requires looking beyond traditional banking metrics. These protocols rely on on-chain behavior rather than social security numbers or bureau reports.

No comments yet. Be the first to share your thoughts!