The 2026 shift from collateral to reputation

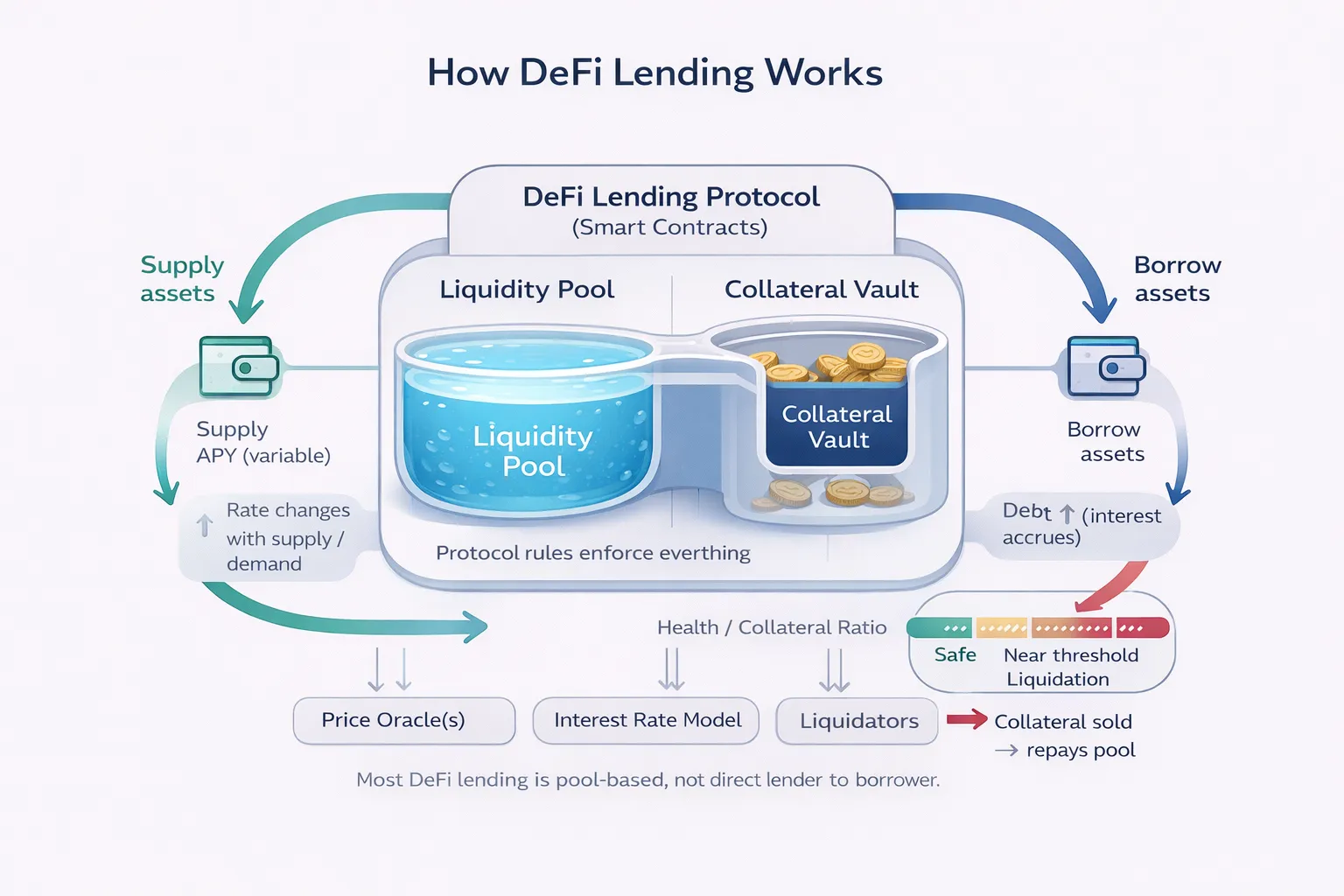

The DeFi lending landscape is undergoing a fundamental structural change. For years, the sector relied almost exclusively on over-collateralization to manage risk. Borrowers had to lock up assets worth significantly more than the loan amount to secure credit. This model limited access to capital and created inefficient capital allocation. In 2026, the industry is pivoting toward on-chain credit scoring. This shift allows lenders to assess borrowers based on their transaction history and behavioral reputation rather than just the value of their locked assets.

This transition is driven by growing institutional demand for yield and the tokenization of real-world assets (RWA). As DeFi matures, lenders need more nuanced risk assessments to serve sophisticated borrowers who cannot or do not want to tie up large amounts of capital in collateral. Verifiable repayment behavior, debt utilization, and financial stability enable uncollateralized or undercollateralized lending, opening the market to a wider range of participants.

The growth in outstanding loans reflects this changing dynamic. According to DeFi Prime, DeFi outstanding loans grew 37% in 2025, a surge largely attributed to RWA tokenization and institutional interest. This growth signals that the market is ready for more complex credit evaluation systems. Blockchain-based credit ratings are becoming the infrastructure for this new era, moving beyond simple collateral checks to a comprehensive trust evaluation framework.

The move toward reputation-based lending does not eliminate the need for collateral entirely. Instead, it reduces the collateral requirements for trusted borrowers. Lenders can now offer better terms to users with strong behavioral records. This efficiency improves capital utilization for both borrowers and lenders. As the ecosystem continues to develop, reputation-based scoring will likely become the standard for high-value DeFi transactions, bridging the gap between decentralized finance and traditional institutional lending practices.

Building behavioral credit profiles

A verifiable credit profile is not a single metric but a composite signal derived from a user’s entire transactional footprint. Unlike traditional credit bureaus that rely on sparse monthly reports, decentralized finance (DeFi) protocols access a continuous, immutable ledger of activity. This granular data allows for a more dynamic assessment of creditworthiness, shifting the focus from static identity to proven behavioral reliability.

The construction of this profile relies on several core mechanisms. First, repayment consistency is tracked across lending protocols. Users who consistently service loans on time, or repay them early, build a positive reputation score. Second, collateral health is monitored in real-time. Maintaining a high collateralization ratio without triggering liquidations signals financial discipline and risk management. Third, activity depth considers the diversity of interactions. A user who only engages with one protocol presents a narrower risk profile than one who navigates multiple DeFi ecosystems, providing a broader dataset for risk models.

This infrastructure matters because it solves the "cold start" problem for institutional lending. Traditionally, DeFi users lacked the verifiable history required for large-scale, low-interest loans. By aggregating on-chain behavior into a standardized credit score, protocols can now offer tiered interest rates and higher borrowing limits based on actual performance rather than just asset holdings. This transforms anonymous wallets into accountable economic agents, bridging the gap between speculative trading and institutional-grade credit.

The reliability of these scores depends on the quality of the underlying data. As noted in recent academic research on on-chain credit risk, systematic analysis of these patterns allows for more accurate risk assessments than traditional models (arXiv, 2024). However, users must understand that this history is permanent. Poor financial decisions on-chain are recorded forever, affecting future borrowing capacity across the entire ecosystem.

Decentralized lending protocol standards

The shift toward institutional-grade credit in DeFi has standardized how protocols evaluate borrower risk. Rather than relying solely on overcollateralization, leading platforms now integrate behavioral history and real-world asset (RWA) verification into their approval logic. This evolution allows for under-collateralized loans, provided the borrower’s digital footprint demonstrates consistent repayment behavior and liquidity stability.

Protocols differ significantly in their data sources and risk thresholds. Some prioritize wallet age and transaction volume, while others require identity verification through decentralized identity (DID) providers. The following table compares the primary credit scoring criteria, interest rate models, and target segments of major DeFi lending protocols as of 2026.

| Protocol | Credit Scoring Basis | Rate Model | Target Segment |

|---|---|---|---|

| Aave | On-chain reputation & collateral health | Variable & stable based on utilization | Retail & DAOs |

| Morpho | Peer-to-peer negotiation & history | Market-driven P2P rates | Sophisticated lenders |

| Goldfinch | Off-chain underwriting & RWA verification | Fixed & variable pools | Real-world businesses |

| Maple | Institutional due diligence & treasury analysis | Fixed rate auctions | Treasury managers |

Aave remains the benchmark for on-chain reputation scoring, utilizing smart contract logic to adjust borrowing power based on real-time collateral health and historical wallet activity. This approach favors high-frequency traders and DAOs that maintain strict liquidity ratios. In contrast, Morpho enables peer-to-peer lending where borrowers and lenders negotiate rates directly, relying on off-chain reputation signals to mitigate counterparty risk.

For real-world asset financing, Goldfinch and Maple diverge from pure DeFi mechanics. Goldfinch uses a mix of on-chain collateral and off-chain underwriting to serve small businesses, while Maple focuses on institutional treasuries, requiring rigorous due diligence before approving fixed-rate loans. These models reflect a broader industry trend: credit scoring is no longer just about code, but about verifying the economic reality behind the wallet.

Web3 credit reputation and risk assessment

The shift toward behavioral credit profiles represents a structural change in how lending risk is evaluated, moving from static identity checks to dynamic behavioral analysis. By treating transactional data as a credit ledger, protocols can assess borrower reliability without traditional infrastructure. This mechanism expands access for the unbanked, who often lack the documentation required by legacy systems, while simultaneously introducing new variables into risk modeling.

Financial inclusion is the primary driver of this model. Traditional credit scores exclude billions of people globally due to a lack of formal employment history or collateral. On-chain reputation systems, however, can utilize wallet activity, DeFi interaction history, and repayment patterns to generate a credit profile. As noted by the Center for Long-Term Cybersecurity (CLTC), this approach offers a pathway to integrate underserved populations into the formal financial system, provided data security and privacy protections are rigorously enforced.

However, the reliance on on-chain data introduces distinct risks. Smart contract vulnerabilities, oracle failures, and market volatility can distort credit metrics in real-time. A borrower’s on-chain reputation may appear strong during bull markets but deteriorate rapidly during liquidity crunches. Moody’s Analytics highlights that while default rates may stabilize in 2026, the financial system remains sensitive to shocks that could trigger rapid reassessments of creditworthiness. This volatility requires lenders to implement dynamic risk buffers and stress-testing frameworks that traditional institutions have developed over decades.

The convergence of these factors means that Web3 credit scoring is not merely a technological upgrade but a fundamental rethinking of trust. It demands a balance between openness and security, ensuring that the transparency of blockchain does not compromise user privacy or expose systems to systemic risk. As institutional lenders enter the space, the standardization of these reputation metrics will be critical to preventing fragmentation and ensuring that credit assessments remain reliable across different protocols.

No comments yet. Be the first to share your thoughts!