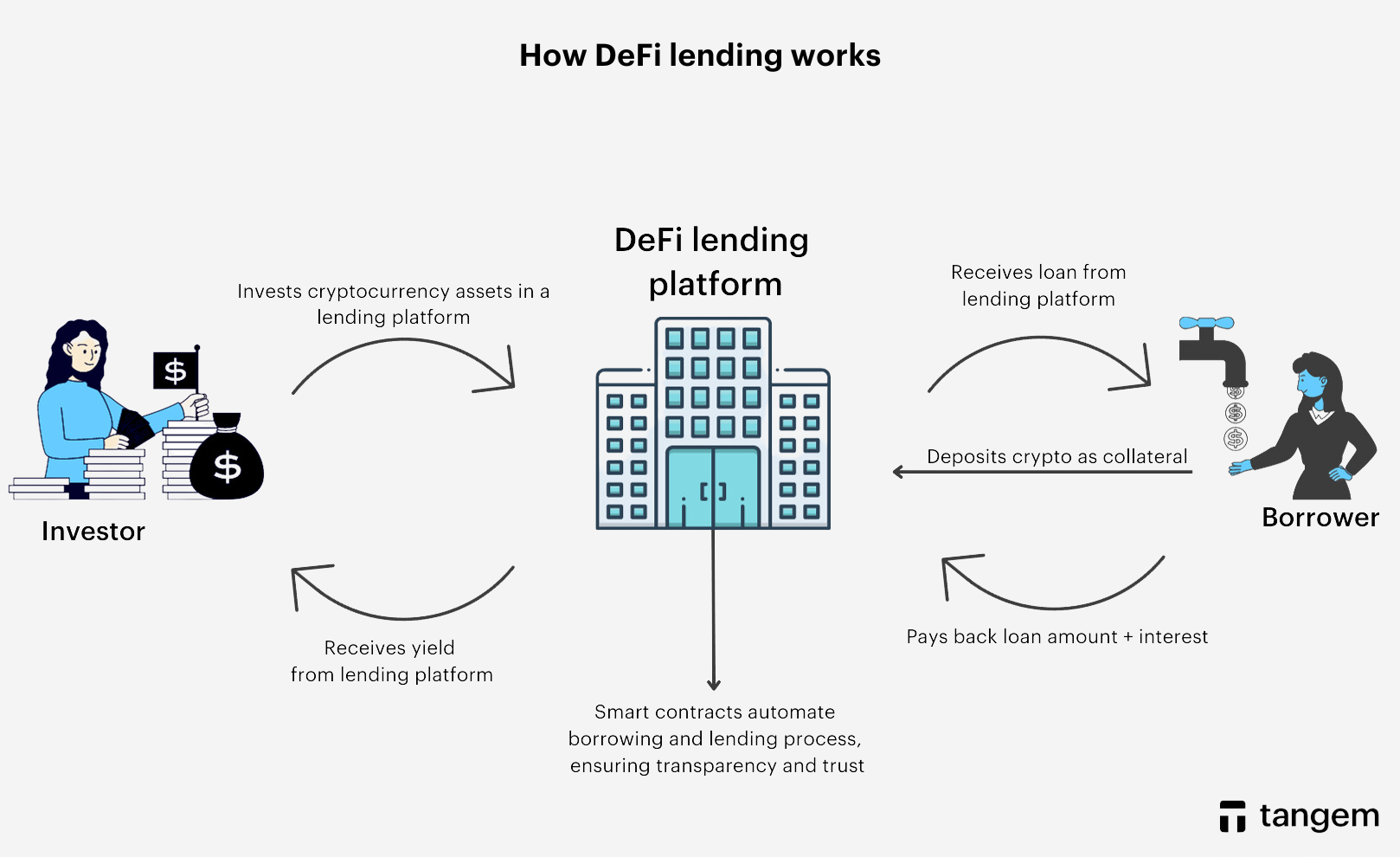

Connect your wallet to a reputation protocol

Building a DeFi credit score requires an on-chain reputation aggregator to track your financial history. Unlike traditional credit bureaus that pull data from banks, these protocols read your wallet activity directly from the blockchain. This data is permanent; every transaction you authorize becomes part of your immutable financial record.

The protocol you choose determines how your borrowing costs are calculated. A high on-chain reputation can lower interest rates across lending platforms, while a poor score can restrict access to liquidity. Establishing this profile early is critical because reputation accumulates over time, not instantly.

Identify a protocol that supports the lending markets you plan to use. Credora and DeTrust are established aggregators that feed data to major DeFi lending platforms. Ensure the protocol you select is recognized by the specific lending markets where you intend to borrow, as scores are not always portable across all platforms.

Most reputation protocols require a browser extension to interface with your wallet securely. Download the official extension from the protocol’s verified website or app store. Avoid third-party links, as malicious extensions can compromise your private keys. The extension will act as the bridge between your wallet and the reputation scoring engine.

Open the extension and click "Connect Wallet." Select your preferred wallet provider (e.g., MetaMask, Rabby, or WalletConnect). You will need to sign a message to prove ownership of the address. This signature does not cost gas but authorizes the protocol to read your public transaction history.

After connecting, the protocol will begin indexing your past transactions. This process may take several minutes depending on your wallet’s history length. Check the dashboard to confirm that your assets and transaction history are being tracked. If data is missing, ensure you are connected to the correct network (e.g., Ethereum Mainnet, Arbitrum, or Base).

Once connected, your wallet’s history is being analyzed. The protocol looks for patterns such as consistent repayment of loans, healthy collateralization ratios, and active participation in governance. These behaviors signal reliability to lenders, forming the foundation of your DeFi credit score.

Generate on-chain lending history

You cannot wait for a score to appear; you must create the data that scoring models analyze. On-chain reputation is permanent. Every transaction is recorded on the blockchain, meaning a single default can permanently damage your borrowing costs and limit access to future liquidity.

To build a positive history, you need to treat DeFi lending like a traditional loan. The goal is to generate a consistent record of on-time repayments. This section outlines the concrete steps to establish that history using established protocols and recognized credit bureaus.

Choose a lending protocol that actively reports to a recognized DeFi credit bureau. Not all platforms do this. Look for partnerships with established identity and credit infrastructure providers. This ensures your repayment history is aggregated into a score that other lenders will actually recognize.

Take out a loan size you can comfortably repay within a few weeks. The goal is not to maximize leverage but to generate a clean repayment record. A small, fully repaid loan is worth more to a credit model than a large, risky one.

DeFi transactions require manual action. Set up calendar reminders or use protocol features to automate repayments before the due date. Missing a single payment can create a negative mark on your on-chain history that is difficult to offset later.

After repayment, check your profile on the credit bureau’s dashboard. Ensure the transaction is recorded and your score reflects the positive behavior. If the data is missing, contact the protocol’s support team to resolve the reporting gap.

The mechanics of score building are straightforward: borrow responsibly, repay on time, and verify the data. As DeFi outstanding loans continue to grow, driven by institutional demand and real-world asset tokenization, the quality of your on-chain history will directly determine your access to capital. DeFi Prime tracks these market shifts, highlighting how creditworthiness is becoming a primary filter for liquidity.

Bridge traditional credit data

A history of missed payments or high utilization on a decentralized loan cannot be deleted, and it directly dictates your borrowing costs for years. By linking off-chain credit data, you can leverage established payment history to lower interest rates on DeFi protocols, but the process requires careful execution to ensure the data is accurate and securely integrated.

1. Verify your identity with an approved provider

The first step is connecting your wallet to a recognized credit bureau or identity verification service. Providers like TransUnion have begun integrating with blockchain-based lending protocols to deliver traditional credit scores without compromising privacy. You will need to complete a Know Your Customer (KYC) process, which typically involves uploading government identification and verifying your address. This step establishes the legal link between your real-world identity and your digital wallet address.

Select a DeFi lending platform that explicitly supports traditional credit data integration. During the onboarding or profile setup phase, choose the option to link external credit history. You will be redirected to a secure verification portal where you authenticate your identity. Ensure you are using a reputable partner, such as TransUnion or Equifax, to guarantee the data source is authoritative.

2. Authorize data sharing securely

Once your identity is verified, you must explicitly authorize the sharing of your credit report with the DeFi protocol. This is done through a smart contract permission or a signed message that grants the protocol read-only access to your credit score. This permission is crucial because it allows the lending algorithm to factor in your off-chain payment history when calculating your on-chain credit score. Review the data access permissions carefully to ensure you are only sharing the necessary financial metrics.

After identity verification, the platform will request permission to access your credit data. Review the specific data points being shared, such as payment history, credit utilization, and account age. Confirm the transaction in your wallet. This action creates a permanent record of your consent, allowing the protocol to pull your traditional credit score into your DeFi profile.

3. Monitor your integrated score

With the data linked, your DeFi credit score will begin to reflect your traditional credit behavior. On-time payments on traditional loans will boost your score, potentially lowering your borrowing costs on decentralized platforms. However, negative marks like late payments or high credit utilization will also impact your on-chain reputation. Regularly monitor your score through the platform’s dashboard to ensure the data is being updated correctly and to identify any discrepancies.

Access your DeFi profile dashboard to view your integrated credit score. The score should update periodically as new credit report data is received from the bureau. Set up alerts if available to notify you of significant changes. Consistently making on-time payments on both traditional and decentralized loans will help build a robust, multi-faceted credit history that lowers your borrowing costs over time.

Check your score before applying

Unlike a traditional credit report, every transaction, loan, and repayment is etched into the ledger. A low score today doesn't just mean higher interest rates; it signals risk to lenders for years, potentially locking you out of high-stakes DeFi loans or forcing you to post excessive collateral. Reviewing your metrics before applying is not optional—it is the difference between securing favorable terms and overpaying for capital.

Start by logging into the DeFi protocol or credit bureau that generated your score. Look beyond the final number. You need to understand the underlying mechanics: utilization and payment history. High utilization—using most of your available credit limit—signals financial stress, even if you are current on payments. Conversely, a flawless payment history with low utilization is the gold standard. If your score seems lower than expected, dig into the breakdown. Is it a single missed payment from months ago? Is your debt-to-income ratio skewed by a recent large position?

Once you identify the drag on your score, you have a narrow window to correct errors or improve metrics before submitting your loan application. If there is a genuine error, such as a misattributed transaction, contact the protocol's support team immediately with proof. If the score reflects your actual behavior, focus on reducing utilization by paying down balances or increasing your credit limit through additional on-chain activity. Remember, this data is public and immutable; you cannot erase history, but you can build a stronger present.

Treat this review as a final audit. Ensure all your linked wallets are accounted for and that your identity verification (KYC) status is current if the protocol requires it. Lenders will cross-reference your on-chain activity with your verified identity. Any mismatch can lead to immediate rejection or manual review, delaying your access to capital. By taking this step, you ensure that your application reflects your true creditworthiness, maximizing your chances of approval and minimizing your cost of borrowing.

Common mistakes to avoid

Unlike a FICO score that might drift over time, on-chain reputation is immutable. A single reckless move can lock you out of favorable borrowing rates for months or years. To protect your standing, steer clear of these three pitfalls.

Over-leveraging your position

It is tempting to max out your collateral to borrow as much as possible, but this spikes your liquidation risk. If the market dips, your DeFi credit score takes a direct hit from the default or forced liquidation. Keep your loan-to-value ratio conservative. A healthy score comes from consistent, manageable repayments, not from stretching your capital to the breaking point.

Ignoring gas fees for timely repayments

Missing a repayment window because you ran out of ETH or BNB for transaction fees is a common error. The protocol does not care about your wallet balance; it only sees the missed payment. Always keep a buffer of native gas tokens separate from your collateral. Automate reminders or set up small, frequent repayments to ensure you never miss a deadline due to network congestion.

Using unverified protocols

Not all platforms calculate credit scores the same way. Using obscure or unaudited protocols can lead to data that is either inaccurate or ignored by major lenders. Stick to established DeFi credit bureaus and protocols with transparent, verified code. Your reputation is only as strong as the trust placed in the system recording it.

No comments yet. Be the first to share your thoughts!