Why DeFi credit scores 2026 matter now

The financial world is shifting from identity-based trust to behavior-based trust. Traditional credit scores like FICO rely on a narrow set of banking history that leaves millions of people invisible to lenders. DeFi credit scores 2026 solve this by using on-chain reputation to evaluate borrowers based on their actual financial behavior rather than their demographic profile.

This transition is urgent because the limitations of FICO are becoming more apparent in a globalized digital economy. A FICO score only reflects past debt repayment on traditional loans. It cannot see your DeFi lending history, your consistent staking rewards, or your reliable participation in liquidity pools. In the DeFi space, your wallet address is your resume, and every transaction builds a verifiable track record.

The 2026 landscape demands this shift. As decentralized finance matures, lenders need a way to assess risk without the delays and biases of traditional underwriting. On-chain reputation provides a real-time, immutable record of reliability. This allows for faster loan approvals and more inclusive lending practices that reward consistent financial discipline, regardless of where you live or your credit history.

For borrowers, this means your financial reputation is no longer locked in a bureau database. It moves with you, accessible to any compliant DeFi protocol. This democratization of credit is not just a technological upgrade; it is a fundamental change in how value and trust are assigned in the modern economy.

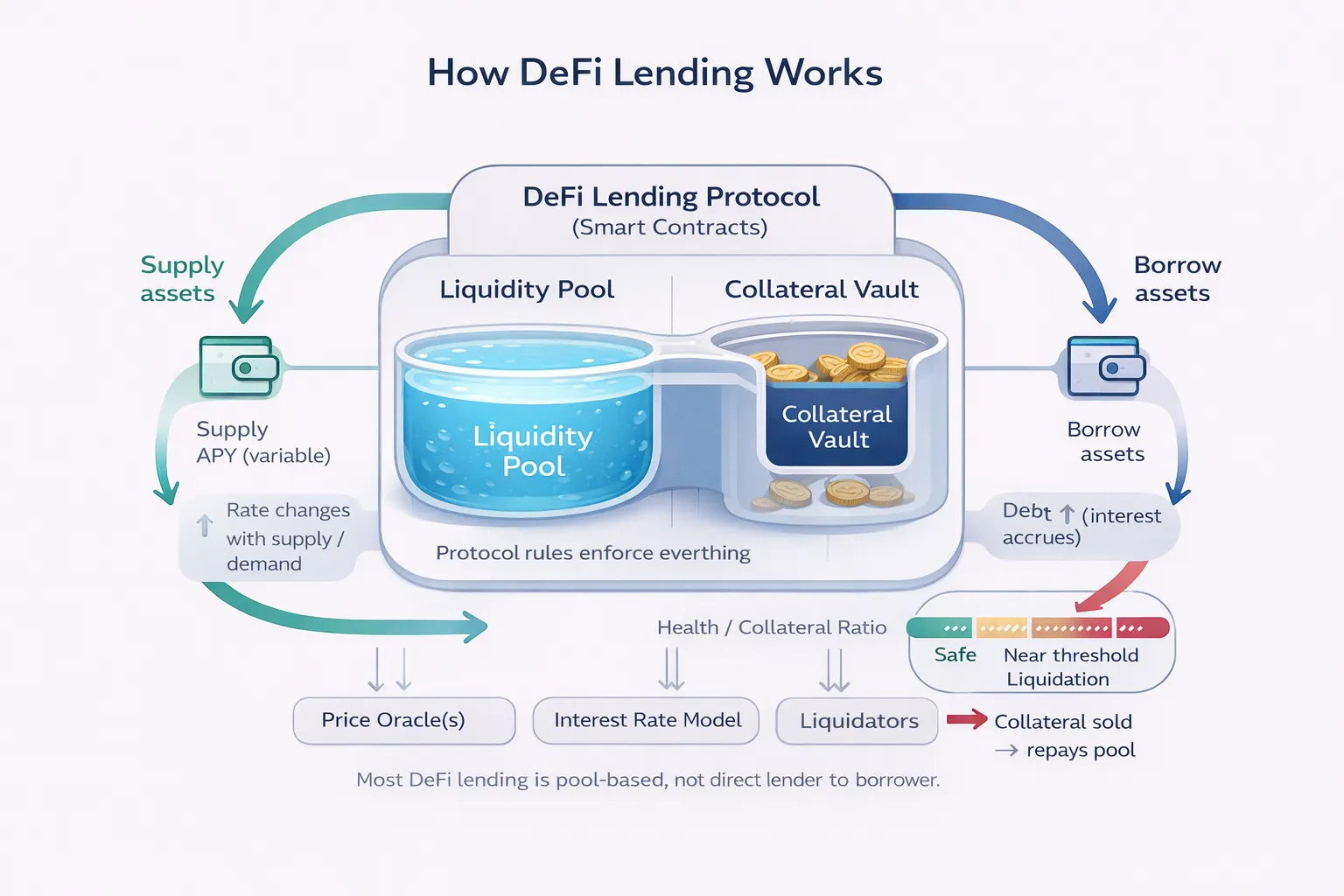

How on-chain history builds reputation

DeFi credit scores replace the static snapshot of a FICO report with a living ledger of wallet activity. Instead of relying on a single bureau’s assessment, these algorithmic scores evaluate a user’s financial behavior across multiple chains and protocols. The result is a dynamic trust score that updates in real time as transactions settle.

The foundation of this reputation is repayment history. In traditional finance, a missed payment stays on your report for years. In DeFi, the system tracks whether you have consistently met loan obligations, refinanced on time, or defaulted on positions. This historical data is transparent and immutable, allowing lenders to assess risk with far greater granularity than a simple credit score.

Collateralization ratios play a central role in determining borrowing power. Unlike unsecured personal loans, most DeFi credit is overcollateralized. The system monitors the ratio of your locked assets to the borrowed amount. A healthy ratio signals stability, while a dropping ratio triggers warnings or liquidations. This mechanism ensures that lenders are protected while rewarding users who maintain conservative leverage.

Wallet activity provides the final layer of context. Lenders look at the age of the wallet, the diversity of interactions, and the consistency of transaction volume. A wallet with a long history of steady, low-risk activity is viewed more favorably than one with sporadic, high-volume trades. This creates a verifiable on-chain identity that can unlock better loan terms and higher credit limits.

Leading DeFi Credit Scoring Protocols

The shift from traditional FICO scores to on-chain reputation systems has fragmented across several major DeFi lending platforms. While some protocols rely on over-collateralization, others are integrating sophisticated credit scoring layers to enable under-collateralized lending. This comparison focuses on the protocols actively building or utilizing credit scoring mechanisms.

Aave (G3) and Credit Delegation

Aave’s third-generation architecture introduces "credit delegation," a feature that allows trusted addresses to borrow on behalf of others. This effectively creates a delegated credit score based on the delegator’s on-chain reputation. The protocol leverages real-world asset (RWA) integrations and sophisticated risk modules to assess the reliability of these delegated relationships.

Compound Finance

Compound has historically relied on algorithmic interest rate models driven by supply and demand. However, recent iterations and associated reputation layers are exploring on-chain identity metrics to refine risk parameters. While not a standalone credit score, Compound’s governance and risk frameworks are increasingly incorporating wallet history to determine borrowing limits and interest rates.

Specialized Reputation Layers (e.g., Burrow, Goldfinch)

Protocols like Burrow and Goldfinch are built specifically for under-collateralized lending, making credit scoring their core functionality. Burrow uses a "borrower score" based on on-chain activity, while Goldfinch utilizes a combination of on-chain data and off-chain identity verification (KYC) to assess borrower reliability. These platforms represent the most direct application of DeFi credit scoring.

Comparison of Key Features

The table below compares the credit scoring approaches of these leading protocols.

Market Sentiment and Token Performance

The adoption of credit scoring features is closely tied to the market performance of these protocols' native tokens. Investors often view the integration of credit scoring as a bullish signal for long-term sustainability and user acquisition.

Technical Analysis: Aave (AAVE)

Understanding the technical outlook for Aave provides insight into market confidence in its credit delegation model. The following chart shows the daily price action and key indicators.

The Hidden Costs of Trustless Lending

DeFi lending promises permissionless access to capital, but it replaces identity verification with code. This shift introduces risks that traditional credit scores were designed to mitigate. Without KYC, protocols cannot assess a borrower’s true financial health or history of repayment. Instead, they rely on over-collateralization, where borrowers must lock up more value than they borrow. This mechanism protects lenders from default but traps capital and exposes borrowers to liquidation risks during market volatility.

Smart contract risk is the most immediate threat. Even with robust audits, code vulnerabilities can lead to total loss of funds. The 2022 Poly Network exploit, for example, resulted in a $610 million loss before funds were recovered. While rare, such events highlight the fragility of unsecured or semi-secured lending environments. Unlike traditional banks, DeFi protocols lack insurance funds or government backstops to absorb losses. Borrowers must assume that any smart contract they interact with could fail at any moment.

Over-collateralization creates a second layer of risk. Borrowers must maintain a health factor above a certain threshold to avoid liquidation. If the value of their collateral drops below this threshold, automated scripts sell their assets, often at a loss. This process can be exacerbated by flash loan attacks or oracle manipulation, where malicious actors distort price feeds to trigger unfair liquidations. The result is a system where borrowers bear the brunt of market swings, with little recourse for error or fraud.

The absence of identity verification also enables malicious actors to exploit the system. Sybil attacks, where one entity creates multiple identities to manipulate lending rates or drain liquidity pools, are common. Without KYC, it is difficult to trace these actors or hold them accountable. This undermines the integrity of the lending market and increases the cost of capital for legitimate borrowers.

To navigate these risks, borrowers must treat DeFi lending like a high-stakes game. Every transaction is a bet on the stability of the protocol, the accuracy of the oracle, and the resilience of the collateral. While the potential rewards are high, the risks are equally significant. Understanding these dynamics is essential for anyone considering unsecured or semi-secured DeFi lending.

No comments yet. Be the first to share your thoughts!