What MiCA 2026 means for credit data

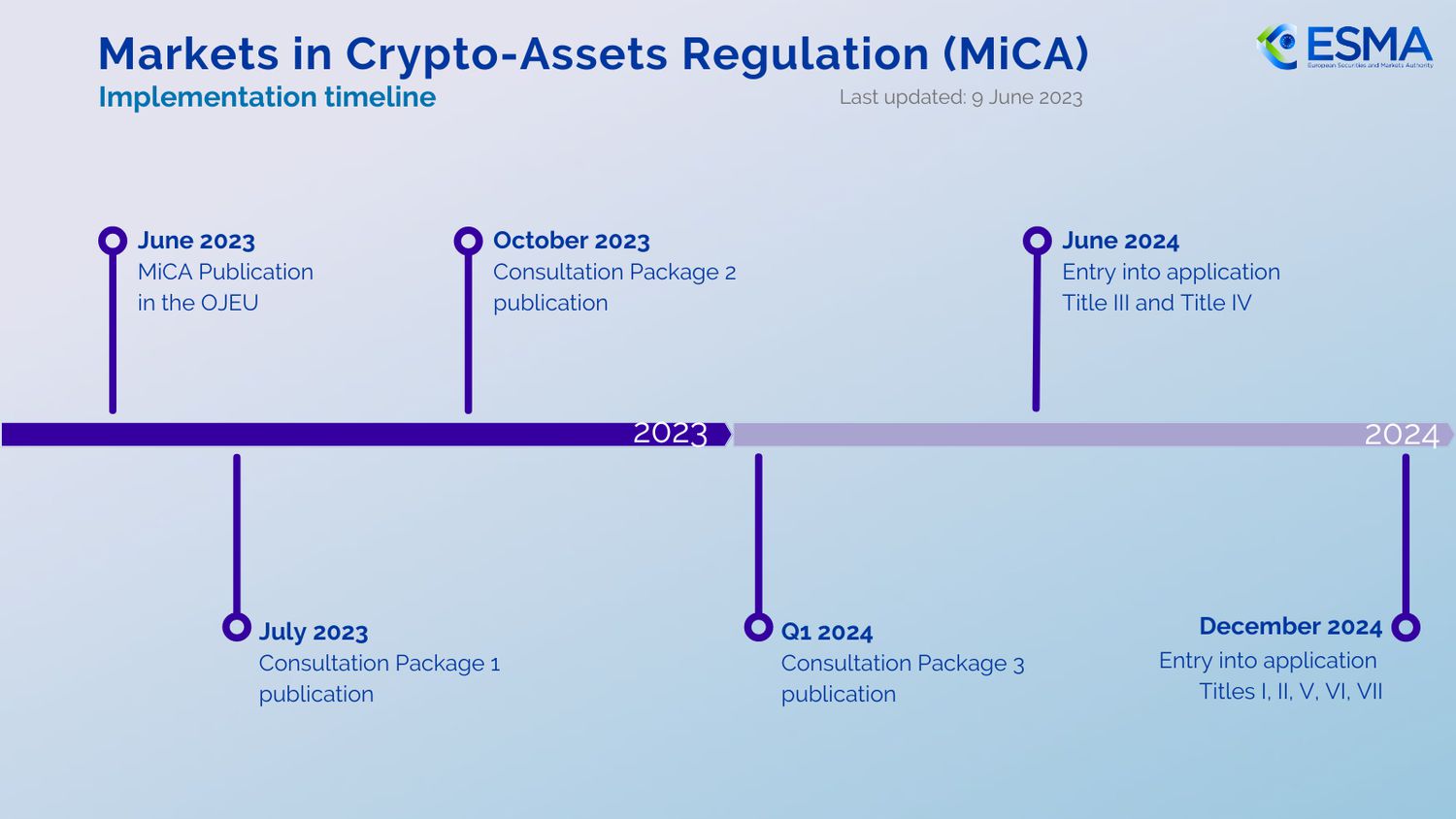

The Markets in Crypto-Assets Regulation (MiCA) establishes the legal foundation for treating digital assets as verifiable collateral rather than speculative instruments. By April 2026, the European Union’s consolidated market will enforce uniform standards for Credit-Associated Service Providers (CASPs), Asset-Referenced Tokens (ARTs), and Electronic Money Tokens (EMTs). This regulatory shift directly impacts credit scoring by mandating the transparency and reserve requirements necessary for accurate risk assessment.

For credit data infrastructure, this means that the historical volatility and opacity that previously disqualified crypto assets from traditional lending models are being replaced by auditable, real-time reserve proofs. Lenders can now integrate verified on-chain data into credit algorithms, allowing for the inclusion of digital asset holdings in creditworthiness calculations. This transforms crypto from a high-risk liability into a quantifiable asset class within the European financial system.

The enforcement of these rules requires CASPs to maintain rigorous record-keeping and reporting standards. This data availability enables credit bureaus to incorporate verified crypto transaction histories into consumer credit profiles. Consequently, individuals and businesses with significant crypto holdings may see their credit scores reflect their true financial capacity, provided the underlying assets comply with MiCA’s reserve and issuance requirements.

Stablecoin collateral classification under MiCA

The Markets in Crypto-Assets Regulation (MiCA) establishes a binary classification for stablecoins, fundamentally altering their eligibility as credit collateral. Lenders must distinguish between Asset-Referenced Tokens (ARTs) and Electronic Money Tokens (EMTs) to determine risk weighting and reserve adequacy. This distinction dictates whether a crypto-asset can secure a loan and at what discount rate.

ARTs represent claims on a basket of assets or fiat currencies and are subject to strict issuance limits and reserve requirements. Because their value is derived from a diversified portfolio, regulators view them as having higher complexity and potential liquidity risk. EMTs, by contrast, are pegged to a single fiat currency and function similarly to traditional electronic money. They benefit from streamlined reserve requirements and clearer redemption rights, making them more predictable for credit underwriting.

The following comparison outlines the regulatory differences that directly impact collateral valuation.

| Feature | Electronic Money Tokens (EMTs) | Asset-Referenced Tokens (ARTs) |

|---|---|---|

| Reserve Requirement | 100% high-quality liquid assets | Diversified asset basket with strict limits |

| Issuer Liability | Strict capital and governance rules | Comprehensive prospectus and audit requirements |

| Credit Suitability | High; lower volatility risk | Moderate; higher complexity and redemption risk |

| Regulatory Scope | EU-wide passporting | EU-wide passporting with enhanced oversight |

For credit score calculations, EMTs are generally favored as collateral due to their stable peg and transparent reserve backing. ARTs may be accepted but often require higher haircuts to account for the complexity of the underlying asset basket. Lenders must verify that the token issuer holds a valid authorization from a national competent authority before accepting any stablecoin as security.

Verification requirements for borrowers

Under the Markets in Crypto-Assets (MiCA) regulation, the path to establishing a verifiable credit history is strictly gated by compliance. Borrowers seeking to have their crypto activity recorded for credit scoring purposes must first satisfy the rigorous identity verification standards imposed on Crypto-Asset Service Providers (CASPs). This is not a mere formality; it is the foundational layer of financial integrity that allows regulatory bodies and credit agencies to link digital asset transactions to a specific, verified individual.

1. Complete Identity Verification (KYC)

Before any credit-relevant data can be aggregated, borrowers must undergo full Know Your Customer (KYC) procedures. CASPs are required to collect and verify official identification documents, such as passports or national ID cards, and confirm the borrower’s residential address. This step ensures that the entity behind the wallet is a real, identifiable person. Without this verified identity, transactions remain anonymous in the eyes of the law, rendering them invisible to credit reporting systems.

2. AML Compliance and Source of Funds

Anti-Money Laundering (AML) checks are mandatory for all credit-related crypto activities. Borrowers must demonstrate the legitimacy of their assets. CASPs must screen transactions against sanctions lists and monitor for suspicious patterns. If a borrower’s funds originate from high-risk jurisdictions or exhibit characteristics of money laundering, the credit activity will be flagged or rejected. This scrutiny ensures that the credit score reflects only lawful financial behavior, protecting the integrity of the lending ecosystem.

3. Travel Rule Adherence

The Travel Rule requires CASPs to share specific information about the originator and beneficiary of crypto transfers. For borrowers, this means that when moving assets to or from a platform that offers credit services, their identity data must accompany the transaction. This creates an immutable, auditable trail that credit bureaus can use to verify the authenticity and context of the borrower’s financial movements. Failure to comply with the Travel Rule can result in blocked transactions and a lack of recorded credit history.

4. Ongoing Monitoring and Record Keeping

Verification is not a one-time event. MiCA mandates continuous monitoring of customer transactions. Borrowers must be aware that their financial activity is under constant scrutiny. Any changes in risk profile or unusual transaction patterns can trigger additional verification steps. This ongoing oversight ensures that the credit data remains accurate and up-to-date, reflecting the current financial standing and compliance status of the borrower.

Provide a valid passport or national ID to the CASP. The platform will verify the document’s authenticity and match it against official databases to confirm your identity.

Submit proof of residence, such as a utility bill or bank statement dated within the last three months. This establishes your legal jurisdiction and risk profile for AML purposes.

Declare the origin of your crypto assets. You may need to provide transaction hashes or wallet addresses to prove that your funds are not derived from illicit activities.

Authorize your CASP to share your identity data with counterparties during transfers. This ensures that your credit activity is traceable and compliant with EU regulations.

Keep your personal information up to date. Notify your CASP of any changes to your identity or address to avoid disruptions in your credit reporting.

Provider licensing and market access

The Markets in Crypto-Assets (MiCA) regulation establishes a unified licensing regime for Crypto-Asset Service Providers (CASPs), Asset-Referenced Tokens (ARTs), and E-money Tokens (EMTs). For entities offering crypto credit products, obtaining authorization under MiCA is no longer optional; it is the mandatory gateway to operating within the European Union. This framework replaces fragmented national rules with a single passport, allowing a firm authorized in one member state to provide services across the entire EU without obtaining separate licenses in each jurisdiction.

Authorization requires meeting strict capital, governance, and operational standards. CASPs must demonstrate robust internal controls, including clear segregation of client assets and rigorous anti-money laundering (AML) procedures. The licensing process is rigorous, with national competent authorities verifying that applicants have adequate policies for risk management, cybersecurity, and consumer protection. For credit-related services, this means that the data handling practices used to assess creditworthiness must align with both MiCA’s operational resilience requirements and the EU’s broader data protection laws.

The single passport mechanism significantly lowers barriers to entry for compliant firms, fostering a more integrated European crypto market. However, it also centralizes regulatory scrutiny. A firm facing enforcement action in its home member state may find its passport rights suspended, effectively halting its operations across the EU. This creates a high-stakes environment where regulatory compliance is not just a legal formality but a core component of market access.

As the July 2026 deadline approaches, the distinction between compliant and non-compliant providers will sharpen. Firms that fail to secure MiCA authorization will lose access to the EU market, while those that succeed will benefit from a harmonized regulatory environment that enhances consumer trust and facilitates cross-border expansion.

2026 Compliance Checklist

As the MiCA implementation phase concludes, Credit Activity Service Providers (CASPs) must verify that their internal controls align with the final regulatory text. The transition from transitional regimes to full authorization requires a rigorous audit of data handling, consumer protection, and cross-border passporting rights. Failure to meet these standards by the end of 2026 will result in the revocation of licenses and the cessation of regulated activities within the EU.

The following checklist outlines the mandatory actions for entities managing crypto-asset credit data.

- Verify CASP Authorization Status: Confirm that your entity holds a valid MiCA authorization from the relevant National Competent Authority. Ensure that your passporting rights are active for all target member states.

- Audit ART and EMT Data Governance: For Asset-Referenced Tokens (ARTs) and Electronic Money Tokens (EMTs), validate that reserve assets are held in segregated accounts and that redemption rights are clearly defined in the white paper.

- Implement Travel Rule Protocols: Update AML systems to capture and transmit originator and beneficiary information for all crypto-asset transfers exceeding the prescribed threshold, ensuring interoperability with other VASP systems.

- Review Credit Data Reporting Standards: Align internal credit scoring models with MiCA’s transparency requirements. Ensure that consumers are provided with clear, standardized information regarding the risks associated with crypto-backed lending.

- Finalize Consumer Complaint Mechanisms: Establish a robust, accessible, and timely complaint handling procedure. Document all interactions to demonstrate compliance with the MiCA’s consumer protection directives.

For entities operating in jurisdictions outside the EU, these MiCA requirements serve as a baseline for global compliance. The standardization of EU crypto markets is expected to influence regulatory frameworks in the US and Asia, making early adoption of these practices a strategic advantage. Stay informed by monitoring updates from the European Banking Authority (EBA) and the European Securities and Markets Authority (ESMA).

No comments yet. Be the first to share your thoughts!