In the wild ride of decentralized finance, your on-chain credit score acts like a volatile altcoin - surging on good trades, plunging amid market mayhem. Platforms like Crypto Credit Scores track wallet behaviors across blockchains, turning transactions into trustworthiness metrics. Yet, these scores swing wildly, mirroring crypto credit score fluctuations that leave lenders wary and borrowers scrambling. Understanding this turbulence is key to navigating DeFi's promise of financial inclusion without the pitfalls of traditional credit bureaus.

The Anatomy of On-Chain Credit Score Volatility

On-chain credit scores, such as the OCCR Score proposed in recent arXiv research, quantify wallet risk through blockchain footprints - from repayment history to asset holdings. But unlike FICO's stable snapshots, these scores pulse with real-time data. The pseudonymous blockchain amplifies this: no names, just addresses exposed to crypto's frenzy. Volatility stems from assets like ETH or BTC, whose prices whip around due to supply-demand whims rather than economic anchors, as Bruegel notes in critiquing DeFi's foundations.

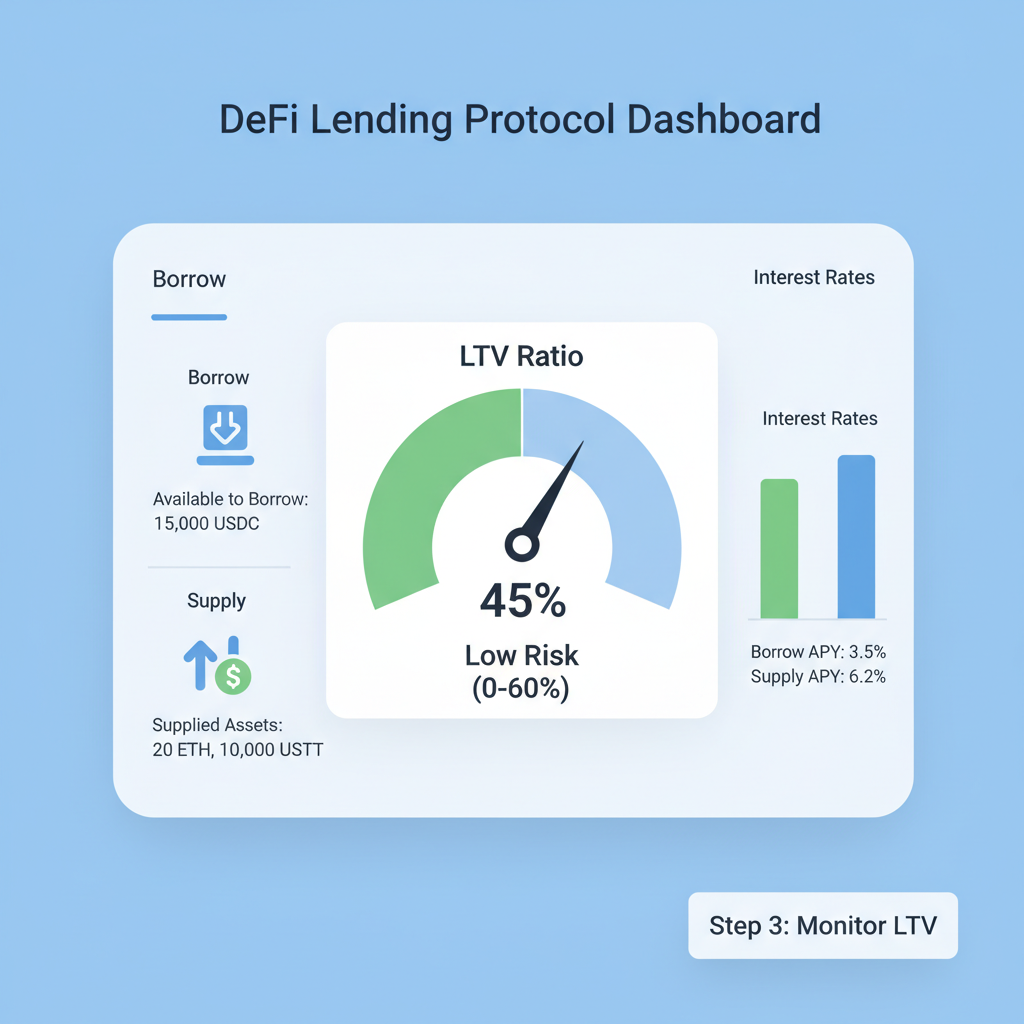

Consider a wallet collateralizing a loan with ETH. A 10% price drop overnight spikes the loan-to-value ratio, dinging the score. Galaxy Research highlights how staking drains liquid collateral from lending pools, tightening markets and pressuring scores further. This isn't mere noise; it's systemic, tying personal credit to market caprice.

Key Causes of On-Chain Credit Volatility

- 1. Market Price Swings: Rapid changes in crypto asset values, like ETH and BTC, alter collateral loan-to-value ratios, directly impacting OCCR scores.Impacted by fiat-referenced volatility (BIS, Visa reports)

- 2. Liquidity Crunches: Sudden drops in DeFi protocol liquidity affect borrowing availability, causing score fluctuations amid volatile on-chain conditions.Exacerbated by stablecoin lending rates (Visa, Galaxy)

- 3. Protocol Changes: Updates or vulnerabilities in DeFi protocols erode user trust and participation, leading to erratic credit assessments.Highlighted in risk management analyses (GARP, arXiv)

- 4. Staking Competition: High staking yields draw liquid collateral away from lending markets, starving DeFi of high-quality assets.Tension between staking and credit (Galaxy Research)

- 5. Hidden Wallet Risks: Pseudonymous wallets obscure identities, complicating risk assessment and asset recovery in on-chain debt.Pseudonymity challenges (Yeshiva U., GARP)

Market Volatility: The Primary Culprit in Score Swings

Crypto's hallmark - on-chain credit score volatility - roots deeply in collateral flux. Visa's analysis of stablecoin lending shows rates fluctuating as ETH and BTC collateral values yo-yo, forcing score recalibrations. A borrower with solid history sees their profile tank if BTC dips sharply, even without missed payments. BIS warns that this fiat-referenced volatility incentivizes over-collateralization, yet scores still falter under sudden shifts.

PYMNTS. com underscores the danger: borrowers face liquidation cascades from these swings, eroding repayment capacity and score integrity. In my 18 years analyzing markets, I've seen commodities steady under fundamentals; crypto lacks that ballast, making scores hypersensitive barometers of sentiment over substance.

Ethereum Technical Analysis Chart

Analysis by Brian Colby | Symbol: BINANCE:ETHUSDT | Interval: 1W | Drawings: 6

Technical Analysis Summary

As Brian Colby, with my conservative fundamental lens overlaid on this technical chart of ETHUSDT through mid-2026, I recommend drawing a primary downtrend line connecting the late 2025 peak around $4,800 (approx. 2025-11-15) to the recent low near $1,720 (2026-02-10), using 'trend_line' tool in red dashed style to highlight the bearish channel post-bull cycle exhaustion. Add horizontal support at $1,700 (strong multi-touch base), resistance at $2,500 (prior swing high), and a rectangle for the ongoing consolidation zone from $1,700-$2,200 spanning Jan-Feb 2026. Use fib retracement from 2025 peak to 2026 low (0.618 at ~$2,900 as key resistance). Mark volume divergence with callout on declining bars during price drop, and MACD bearish crossover with arrow_mark_down. Vertical line at 2026-02-18 for current analysis point. Text notes: 'Macro caution: DeFi volatility weighs on ETH'. This setup educates on waiting for cycle confirmation before long positions.

Risk Assessment: medium

Analysis: Elevated volatility from DeFi credit score fluctuations and collateral risks, but support holding suggests limited downside; conservative stance favors patience

Brian Colby's Recommendation: Hold cash or stables; enter longs only on $1,700 hold with confirmation. Diversify, think long-term cycles.

Key Support & Resistance Levels

📈 Support Levels:

- $1,700 - Strong multi-month base with volume cluster; aligns with 0.786 fib retracement strong

- $1,500 - Psychological and cycle low extension moderate

📉 Resistance Levels:

- $2,500 - Recent swing high and channel top moderate

- $2,900 - 0.618 fib retracement of prior decline weak

Trading Zones (low risk tolerance)

🎯 Entry Zones:

- $1,750 - Bounce from strong support with volume confirmation; conservative long for cycle bottom low risk

- $2,200 - Break above consolidation high for trend shift medium risk

🚪 Exit Zones:

- $2,500 - Initial profit target at resistance 💰 profit target

- $1,600 - Tight stop below key support 🛡️ stop loss

Technical Indicators Analysis

📊 Volume Analysis:

Pattern: declining on downside, potential divergence

Volume fades on recent lows, hinting at selling exhaustion amid DeFi risk aversion

📈 MACD Analysis:

Signal: bearish crossover persisting

MACD below zero line, but histogram contracting—watch for bullish divergence

Applied TradingView Drawing Utilities

This chart analysis utilizes the following professional drawing tools:

Disclaimer: This technical analysis by Brian Colby is for educational purposes only and should not be considered as financial advice. Trading involves risk, and you should always do your own research before making investment decisions. Past performance does not guarantee future results. The analysis reflects the author's personal methodology and risk tolerance (low).

Real-time scoring tools like SolCred attempt adjustments via machine learning, but base volatility persists. GARP points out hidden identities compound this, as risk models grapple with unverified behaviors.

Liquidity Droughts and Protocol Perils Amplify Instability

Beyond prices, liquidity ebbs and flows reshape scores. Staking booms, as Galaxy details, siphon high-quality assets from lending, hiking borrow rates and squeezing marginal wallets. DeFi protocols' upgrades or exploits - think oracle failures or flash loan attacks - jolt participation, rippling through score algorithms.

Medium's Duredev celebrates on-chain data's verifiability, yet volatility undermines it: a liquid market today starves tomorrow, tanking scores for active users. ScienceDirect's DeFi token studies link returns to sentiment, not stability, perpetuating blockchain credit scoring volatility. Reputation DAO's decentralized bureaus aim to parse this, but current systems lag.

Untangled Finance's Moody's integration blends off-chain stability, hinting at hybrid paths. Still, pure on-chain scores demand reckoning with these forces before stabilization takes hold. As we peel back these layers, strategies emerge to tame the swings.

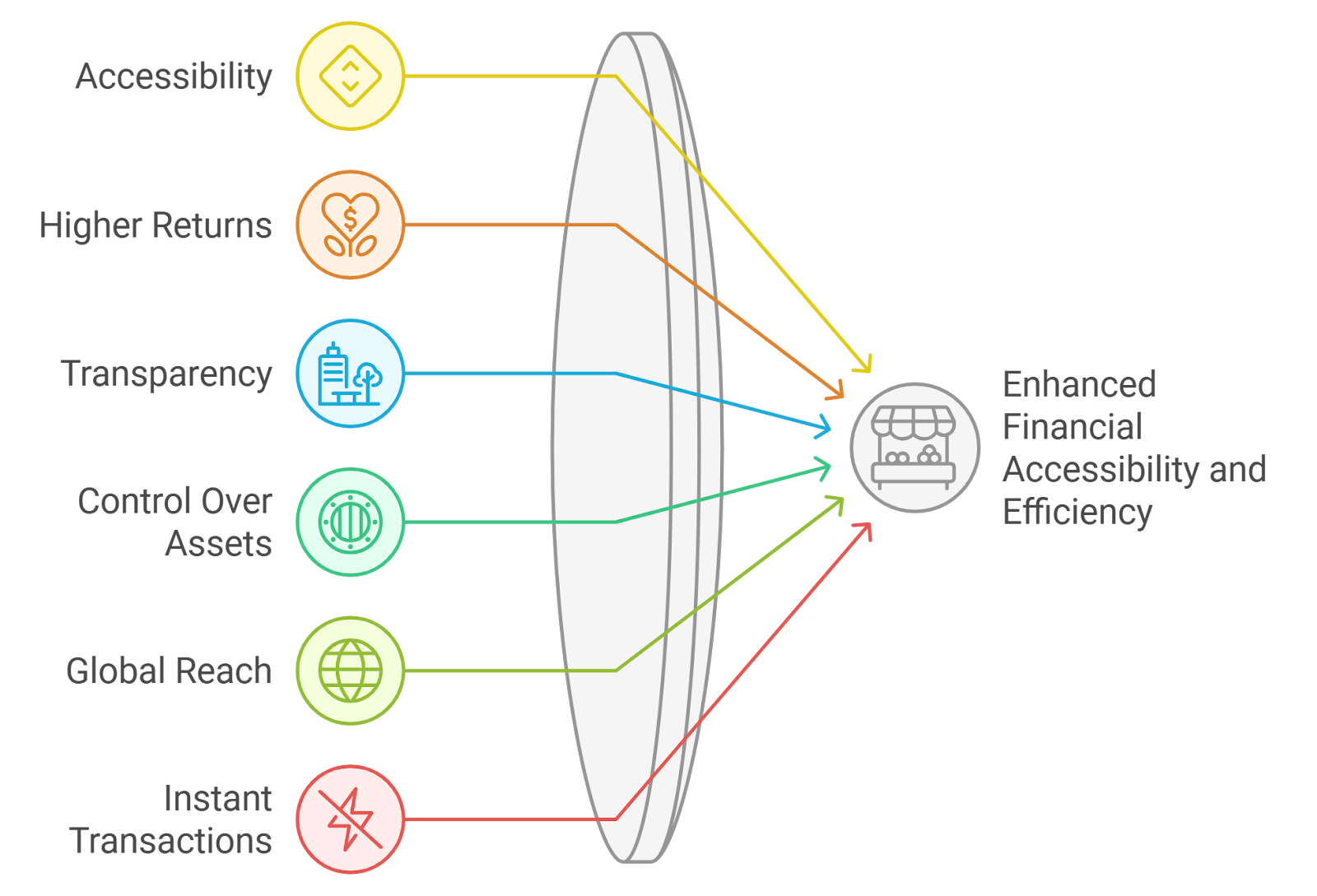

Explore how scores evolveStabilizing these onchain score swings requires blending blockchain's transparency with safeguards against crypto's chaos. Platforms like Crypto Credit Scores pioneer this by aggregating multi-chain data into resilient profiles, factoring in not just snapshots but behavioral trends over cycles. Yet, true steadiness demands deliberate tactics from users and protocols alike.

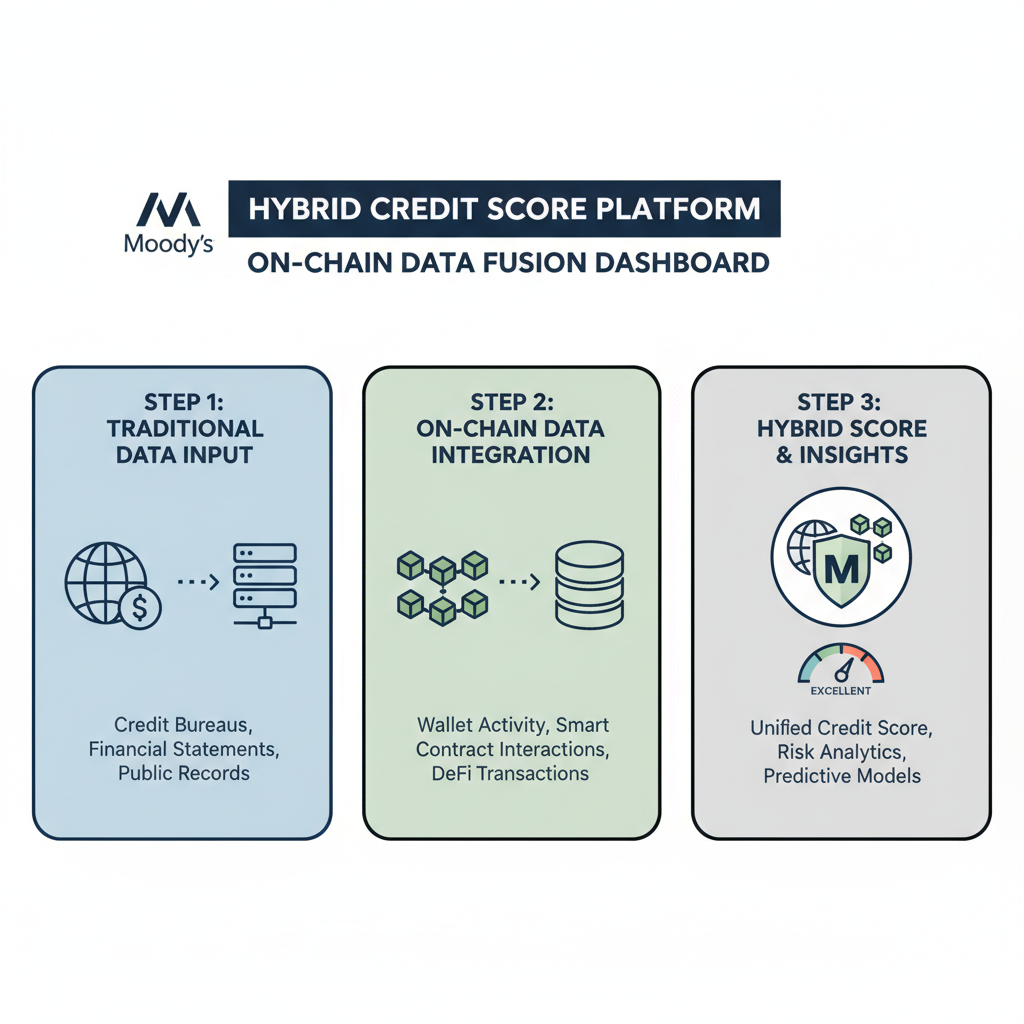

Hybrid Data Fusion: Bridging On-Chain and Off-Chain Stability

One potent approach fuses traditional credit insights with blockchain verifiability. Untangled Finance's partnership with Moody's overlays established ratings onto wallet addresses, diluting pure crypto volatility. This hybrid tempers scores against isolated market dips, as a borrower's off-chain history anchors on-chain whims. In my view, this isn't dilution; it's evolution, echoing how commodities traders layer fundamentals atop price charts for clearer signals.

DeXposure-FM models, detailed in arXiv papers, forecast inter-protocol exposures, preempting cascade risks that amplify fluctuations. By simulating liquidity crunches or staking outflows, these tools smooth score trajectories, much like stress tests in TradFi. Galaxy's staking analysis underscores the need: as LSTs lock assets, predictive modeling ensures scores reflect future availability, not just present holdings.

Reputation DAO's decentralized credit bureaus take this further, crowdsourcing verifiable data audits across chains. No central gatekeeper means tamper-proof scores, resistant to protocol-specific jolts. SolCred's real-time ML scoring adjusts dynamically, weighting recent repayments heavier during volatility spikes, per their whitepaper. These innovations counter GARP's anonymity woes, turning pseudonyms into proven track records.

User-Level Tactics: Building Resilient Wallet Profiles

Individuals aren't passive; proactive habits forge stable scores amid crypto credit score fluctuations. Diversify collateral beyond ETH/BTC - stablecoins or yield-bearing tokens buffer price shocks. Maintain low loan-to-value ratios, avoiding liquidation triggers that scar histories. Regular, small repayments signal reliability, outpacing one-off heroics in algorithms.

Visa notes stablecoin rates steady when non-stable collateral dominates volatility; mirror this by laddering positions across maturities. Avoid high-stake pools during yield famines, preserving liquidity for repayments. Over cycles I've analyzed, patience trumps speculation: wallets with steady DeFi engagement weather storms better than flash traders.

Stabilize Your DeFi Credit Score: 5 Proven Steps Amid Crypto Volatility

Protocols amplify this via dynamic oracles and insurance layers, but users lead. See how these practices lower lending risks.

Protocol Innovations: Architecting Anti-Fragile Scoring Systems

DeFi builders must embed stability at the core. Time-weighted average prices mitigate flash crashes' score impacts. Cross-chain aggregators, like those powering Crypto Credit Scores, average volatility across ecosystems, revealing true risk over noise. BIS critiques decentralization's illusion; counter it with composable risk oracles sharing exposure data network-wide.

Bruegel laments crypto's fundamental voids; fill them with behavioral multipliers - longevity bonuses for veteran wallets, penalizing rugs early. Yeshiva's inclusion vision realizes here: stable scores unlock undercollateralized loans, spreading wealth sans TradFi gatekeepers. PYMNTS warns of dangers, but matured scoring flips volatility from foe to feature, rewarding adaptive actors.

Medium's Duredev nails it: verifiable behavior demystifies borrowers. As DeXposure-FM and SolCred scale, expect scores to dampen like hedged portfolios, fostering trust. ScienceDirect ties DeFi returns to sentiment; advanced models decouple this, grounding scores in actions.

Crypto Credit Scores exemplifies this shift, delivering privacy-preserving assessments that endure market tempests. Wallets scoring consistently high access better rates, closing inclusion loops. In Web3's marathon, stability isn't rigidity; it's agility honed against chaos, empowering all to thrive.

Learn more on risk improvements

No comments yet. Be the first to share your thoughts!