In the rapidly evolving world of decentralized finance (DeFi), one of the most persistent challenges has been enabling uncollateralized loans. Traditional lending relies on comprehensive credit checks and tangible collateral, but blockchain’s pseudonymous nature complicates trust and risk assessment. Enter on-chain reputation scores: a breakthrough solution that leverages blockchain credit scoring and transparent analytics to unlock new DeFi borrowing opportunities for users worldwide.

What Are On-Chain Reputation Scores?

On-chain reputation scores distill a user’s blockchain activity into a quantifiable metric, much like a traditional credit score but rooted entirely in Web3 interactions. These scores analyze wallet behavior, such as transaction frequency, loan repayment history, participation in liquidity pools, and engagement with various DeFi protocols. The result is a DeFi credit reputation that is transparent, tamper-resistant, and portable across ecosystems.

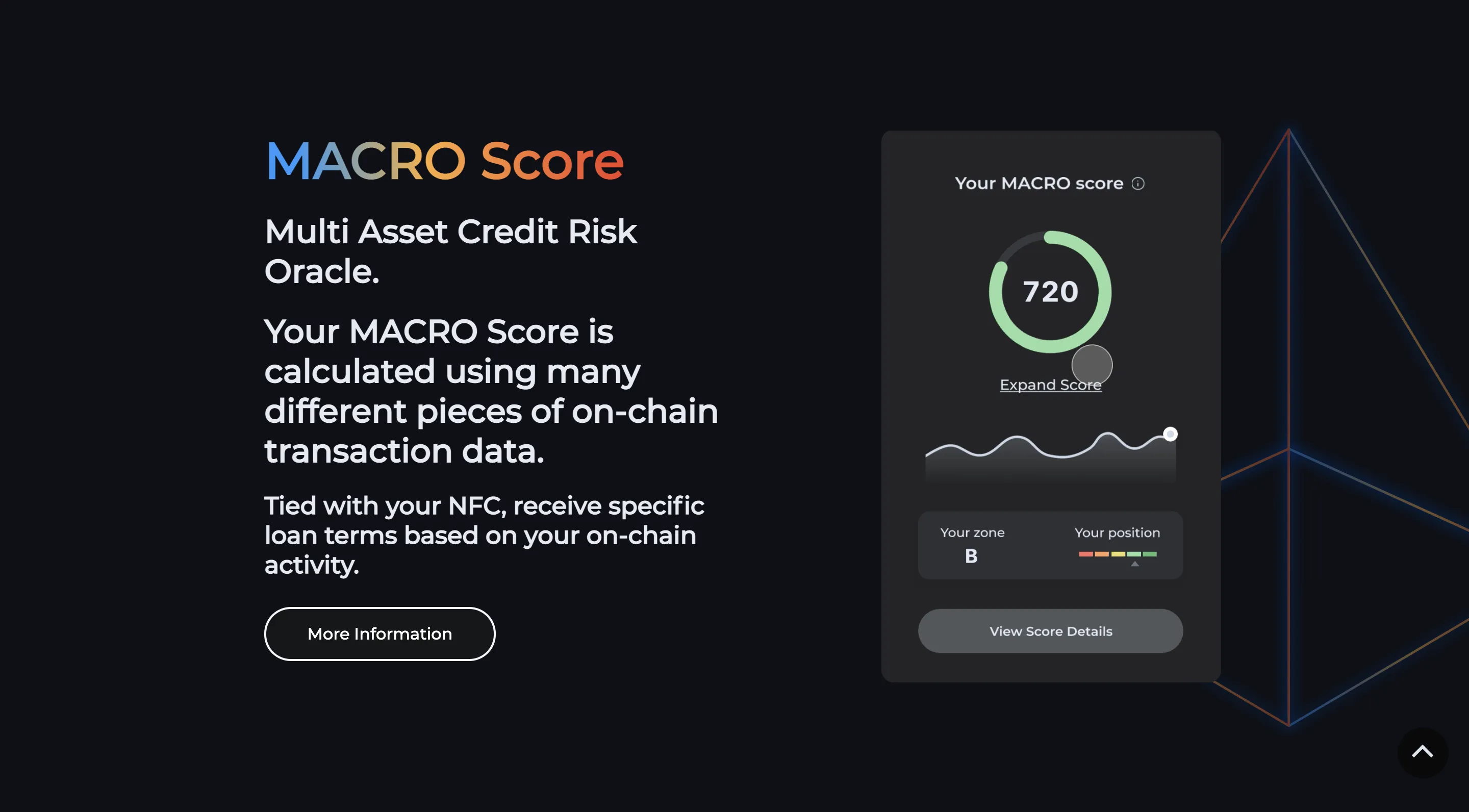

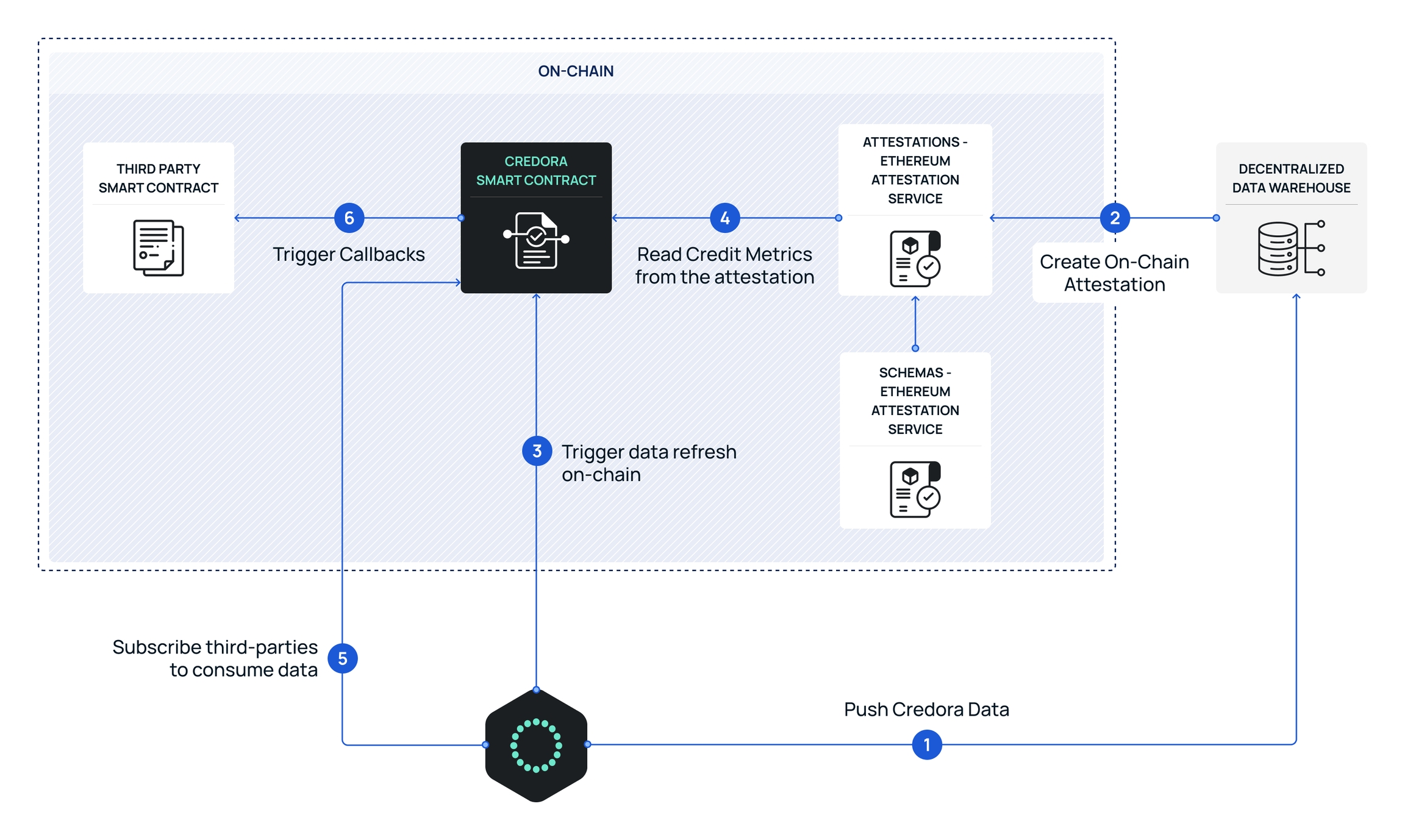

This innovation is more than theoretical. Protocols like Spectral Finance’s Multi-Asset Credit Risk Oracle (MACRO) and Credora are already providing risk-adjusted assessments for DeFi lending markets. Their approaches signal the industry’s move toward decentralized credit bureaus, systems designed to objectively evaluate borrower reliability while preserving privacy.

How On-Chain Reputation Unlocks Uncollateralized DeFi Loans

The promise of uncollateralized loans in crypto is enormous. By removing the requirement for borrowers to over-collateralize, often by 150% or more, DeFi can become far more inclusive and capital-efficient. But how does it actually work?

Core Mechanisms Behind Uncollateralized DeFi Loans

- On-Chain Credit Assessment Protocols: Platforms like Cred Protocol and Spectral Finance analyze users’ blockchain activity—such as transaction history and loan repayments—to generate decentralized credit scores, enabling risk-based lending without collateral.

- Integration of Off-Chain Financial Data: Protocols such as 3Jane Protocol utilize zero-knowledge proofs to securely combine traditional financial data with on-chain activity, enhancing borrower evaluation while preserving privacy.

- Reputation-Based Lending Networks: Union Protocol allows users to build credit lines through social vouching, where others stake assets to back a borrower, creating a web of trust that signals creditworthiness to lenders.

- Privacy-Preserving Verification: Technologies like zero-knowledge proofs (used by platforms such as 3Jane Protocol) enable verification of sensitive financial data without exposing it on-chain, addressing privacy concerns in credit assessments.

- Standardization of Credit Metrics: Efforts are underway to develop universally accepted on-chain reputation standards, such as the Multi-Asset Credit Risk Oracle (MACRO) score by Spectral Finance, fostering interoperability and adoption across DeFi platforms.

Credit assessment protocols like Cred Protocol assign risk profiles based on historical wallet behavior, enabling lenders to offer loans with little or no collateral when justified by strong on-chain reputations. Some platforms are even integrating off-chain data using privacy-preserving techniques such as zero-knowledge proofs, 3Jane Protocol is one recent example, bridging Web2 financial records with Web3 transparency.

Learn more about how on-chain reputation scores are unlocking under-collateralized crypto loans here.

The Role of Community Trust and Vouching Systems

Beyond algorithms, community-driven trust signals are gaining traction in Web3 lending. Union Protocol allows users to vouch for each other by staking assets, creating social collateral that boosts an address’s perceived creditworthiness. This approach leverages network effects: as more users participate and vouch for reliable borrowers, the system becomes increasingly robust against bad actors.

The interplay between algorithmic scoring and peer-based endorsement is shaping the next generation of uncollateralized DeFi lending solutions, offering both transparency and flexibility previously unseen in traditional finance.

Despite the progress, several open questions remain. Standardization is a major hurdle: with each protocol developing its own scoring methodology, interoperability and universal acceptance are still aspirational. The DeFi space is actively debating what constitutes a fair and predictive blockchain credit score. Should it be based on repayment history alone, or should it include factors like DAO participation and cross-chain activity? As more protocols experiment with these variables, the race is on to establish a set of benchmarks that can be trusted across the ecosystem.

Data privacy is another crucial concern. While on-chain credit data is inherently transparent, users demand solutions that protect their identity and sensitive financial details. Zero-knowledge proofs (ZKPs) are emerging as a leading technology here, enabling verification of creditworthiness without revealing private information. This balance between transparency for lenders and privacy for borrowers will likely define the next phase of Web3 lending innovation.

Opportunities and Risks for Lenders and Borrowers

The upside for both borrowers and lenders is substantial. Borrowers with strong DeFi credit reputations gain access to capital without tying up assets as collateral, unlocking liquidity for everything from trading to real-world business growth. Lenders, meanwhile, benefit from broader diversification opportunities and risk-adjusted returns powered by algorithmic scoring tools like Spectral’s MACRO or Credora.

However, risks remain. The possibility of default looms larger in uncollateralized lending than in traditional over-collateralized models. Protocols are responding by refining their risk models, incorporating more granular data points, and even introducing dynamic interest rates that adjust in real time based on updated reputation scores.

Top Protocols Pioneering Uncollateralized DeFi Loans

- Spectral Finance: Known for its Multi-Asset Credit Risk Oracle (MACRO) score, Spectral Finance analyzes on-chain transaction data to generate decentralized credit scores, enabling risk-assessed uncollateralized lending.

- Cred Protocol: This platform offers a decentralized credit scoring system that quantifies on-chain lending risks, expanding access to undercollateralized and uncollateralized loans by evaluating users' blockchain activity.

- Union Protocol: Union introduces reputation-based lending where users can build credit lines through a vouching system, leveraging community trust to unlock uncollateralized borrowing opportunities.

- 3Jane Protocol: By integrating zero-knowledge proofs, 3Jane connects on-chain and off-chain credit data, enabling precise and private credit assessments for uncollateralized loans.

- Credora: Specializing in on-chain credit scoring, Credora provides risk-adjusted credit scores for DeFi markets, helping lenders assess borrower reliability without traditional collateral.

The market impact could be transformative. Analysts project that as trust in crypto credit scoring matures, trillions of dollars could flow into DeFi lending markets, capital that has historically been locked out due to lack of collateral or opaque risk assessment processes.

What’s Next for On-Chain Reputation Scores?

The next wave of innovation will likely focus on cross-protocol portability and composability, allowing users to carry their reputation seamlessly across DeFi platforms, much like a passport for Web3 finance. Interoperable standards could empower users to unlock new borrowing opportunities wherever they go while giving lenders richer datasets to inform their decisions.

This shift also opens doors for new types of financial products: undercollateralized lines of credit tied to stablecoins, real-world asset financing via tokenization, and even decentralized identity solutions that merge off-chain credentials with blockchain-native behavior.

The path forward isn’t without obstacles, regulation, user education, and technical refinement all play pivotal roles, but the trajectory is clear. By embedding trust directly into code and community networks rather than centralized gatekeepers, on-chain reputation scores are redefining what’s possible in digital lending.

If you’re interested in diving deeper into this rapidly evolving field or want practical guidance on building your own DeFi credit profile, explore our comprehensive resource: How On-Chain Risk Scores Enable Under-Collateralized Lending in DeFi.

No comments yet. Be the first to share your thoughts!