Decentralized finance (DeFi) has always promised a more open, accessible, and efficient alternative to traditional financial systems. Yet, until recently, the lack of reliable credit assessment tools meant most DeFi lending relied on heavy over-collateralization. This limited not just who could borrow, but also how much capital could flow into the ecosystem. Today, on-chain credit scoring is rewriting these rules, fueling a new era of trust and capital efficiency across DeFi protocols.

Why Traditional DeFi Lending Needed an Upgrade

Historically, DeFi lending platforms required users to lock up more collateral than the value of their loan - sometimes by 150% or more. This approach made sense in an environment where no one knew who they were lending to; anonymity is both a strength and a challenge in crypto. But it also meant that vast amounts of capital sat idle and that those without significant crypto holdings were effectively excluded from borrowing.

Enter on-chain credit scores: dynamic, transparent measures of user reliability based on blockchain activity rather than opaque off-chain data. These scores are shifting the paradigm from trustless transactions to trust-minimized ones - where reputation and risk can be quantified without sacrificing privacy or decentralization.

The Mechanics of On-Chain Credit Scoring

An on-chain credit score evaluates a user's crypto wallet behavior: transaction history, repayment patterns, protocol interactions, and even DAO participation. The result? A decentralized reputation that any lending protocol can reference in real time. This empowers lenders to assess risk with unprecedented nuance and enables borrowers with strong on-chain histories to unlock under-collateralized or even unsecured loans.

Top 5 Benefits of On-Chain Credit Scoring in DeFi

- Enhanced Financial Inclusion: On-chain credit scoring allows users worldwide to build a financial reputation through their crypto activity, enabling access to DeFi lending without traditional banking relationships or formal credit histories. This opens lending opportunities to the unbanked and underbanked populations.

- Transparent and Verifiable Credit Assessment: Unlike traditional credit bureaus, on-chain credit scores are calculated using transparent, publicly auditable criteria. Users can see how their actions impact their score, and blockchain immutability ensures calculations are tamper-proof.

- Improved Capital Efficiency: By leveraging on-chain credit scores, DeFi protocols can offer under-collateralized or even zero-collateral loans to trustworthy borrowers. This reduces the need for excessive collateral, allowing users to access more capital with less locked value.

- Faster and Automated Lending Decisions: Smart contracts can instantly analyze on-chain credit data, enabling rapid, programmatic loan approvals and disbursements. This streamlines the lending process and reduces manual intervention.

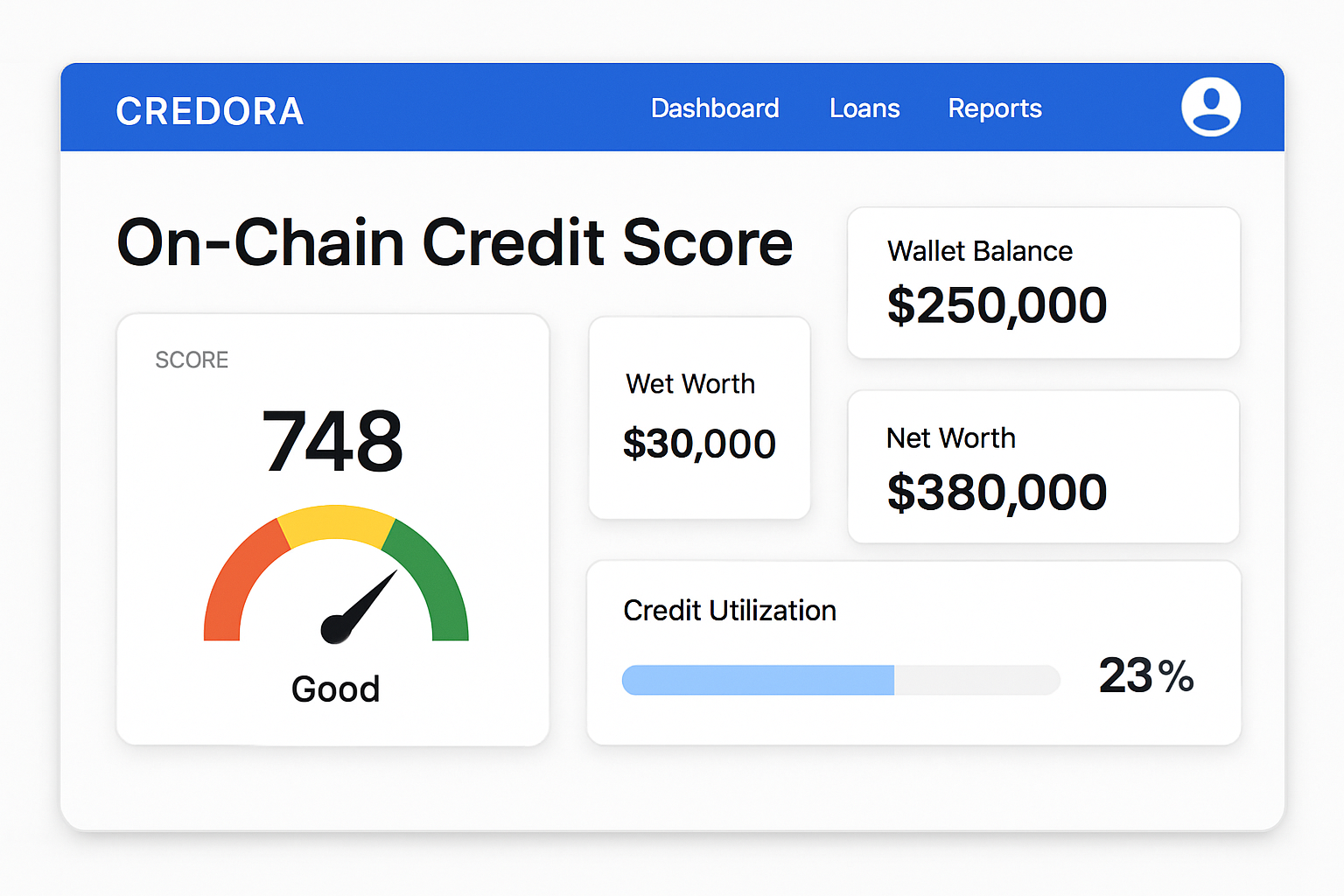

- Greater Trust and Risk Management: Platforms like Credora, CreDA, and RociFi enable lenders to assess borrower risk more accurately using verifiable on-chain histories. This fosters trust between anonymous parties and supports the growth of scalable, secure DeFi credit markets.

This shift isn't just theoretical. Platforms like Credora, CreDA, Untangled Finance (with Moody's), Reputation DAO, and RociFi are already proving that blockchain-based reputation works at scale:

- Credora: Introduced real-time on-chain scores in July 2024 for partners like Clearpool and Obligate, letting investors evaluate risk-adjusted returns transparently.

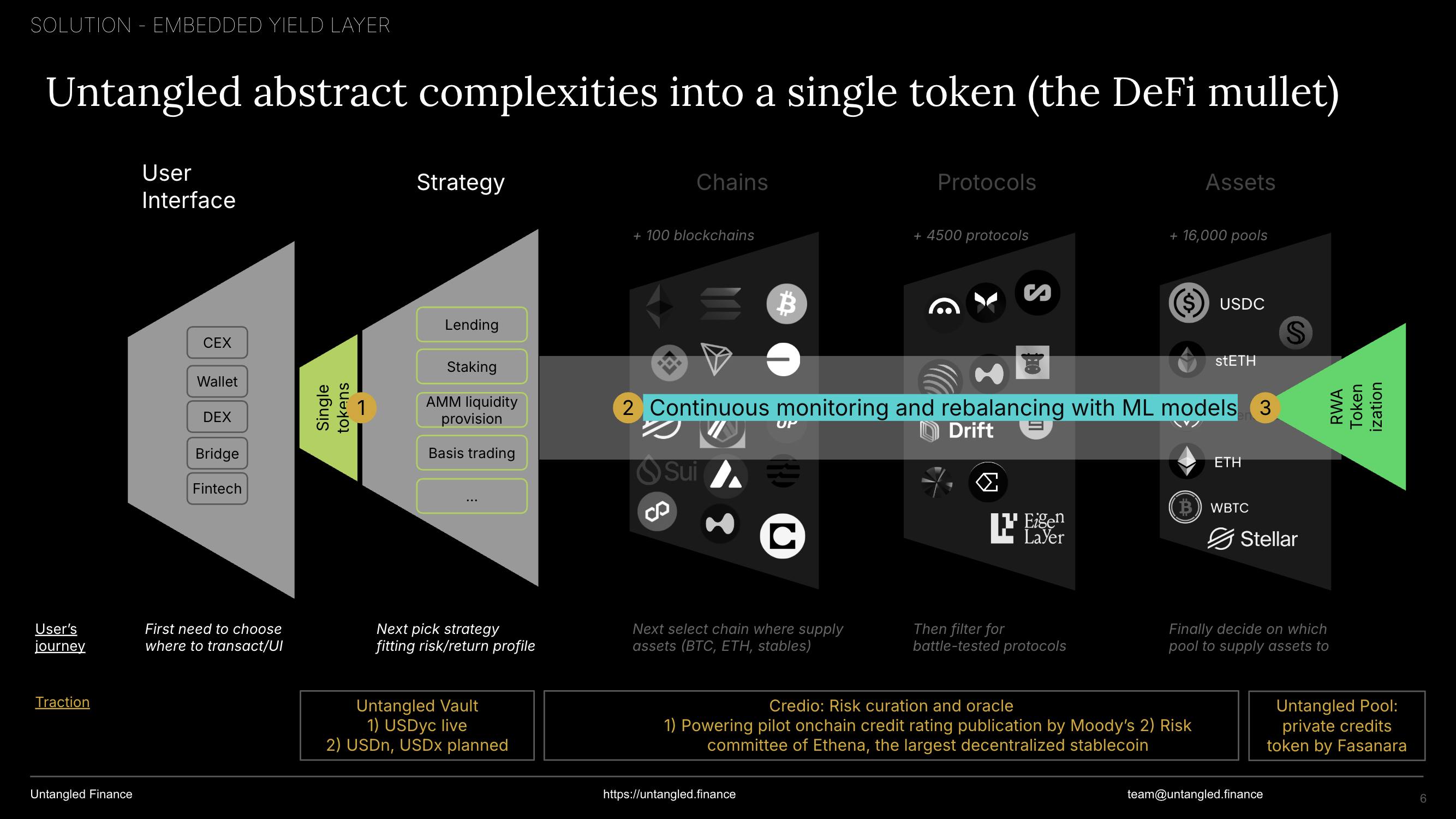

- Untangled Finance and Moody's: Brought traditional ratings on-chain using zero-knowledge proofs in March 2025 - blending institutional credibility with decentralized access.

- CreDA: Pioneered Credit NFTs (cNFTs) tied to users' DeFi activity for leveraged borrowing since early 2022.

- Reputation DAO and RociFi: Enable highly granular scoring using wallet analytics across multiple chains, powering under-collateralized loans based on actual crypto behavior.

The Ripple Effects: Trust, Inclusion and Capital Efficiency

The implications go far beyond mere convenience. By making reputation programmable and portable across protocols:

- Lenders gain transparency: They no longer have to rely solely on collateral as a proxy for trust; they can see exactly how borrowers behave across the entire DeFi landscape.

- Borrowers gain agency: Anyone can build their own decentralized reputation simply by interacting responsibly with smart contracts - no bank account or paperwork required.

- The ecosystem gains efficiency: Capital previously locked up as excess collateral is freed for productive use; high-quality borrowers get better terms; lenders access new markets safely.

This transformation isn't hypothetical - it's already attracting attention from both crypto natives and TradFi giants looking for new ways to measure risk without compromising privacy or control. As highlighted by recent collaborations between Untangled Finance and Moody's Ratings, the convergence of traditional expertise with Web3 innovation is accelerating mainstream adoption of decentralized reputation systems.

Tackling Challenges: Privacy Meets Transparency

No system is perfect yet. While blockchain's transparency makes it easy to verify how scores are calculated (learn more here), it also raises concerns about user privacy and data sovereignty. Leading platforms are addressing this through advanced cryptography such as zero-knowledge proofs - allowing users to prove their creditworthiness without exposing every detail of their financial history.

Another challenge is ensuring the accuracy and fairness of DeFi trust scores. Since on-chain credit scoring relies on wallet activity, questions remain about how to account for Sybil attacks (where users split activity across multiple wallets) or to prevent manipulation. Protocols are experimenting with multi-factor scoring, cross-chain analytics, and partnerships with identity verification services to make scores more robust and resistant to gaming.

Still, the benefits are hard to ignore. By making blockchain credit assessment accessible and programmable, DeFi platforms can finally offer a spectrum of loan products tailored to real user behavior, not just raw collateral value. This opens the door for new financial instruments, permissionless micro-loans, and even borderless credit markets where anyone with a smartphone can participate.

Real-World Impact: From Collateral Constraints to Global Opportunity

The impact of decentralized reputation is already being felt in emerging markets and among unbanked populations. In regions where access to traditional credit is limited or non-existent, individuals can now build a decentralized reputation by simply using DeFi protocols responsibly. Over time, this on-chain history becomes their passport to better rates and larger loans, without ever needing a conventional bank account.

For institutional players, these innovations mean new ways to manage risk transparently while tapping into previously unreachable borrower segments. As more real-world assets are tokenized and brought on-chain, expect borderless lending powered by on-chain scores to become the norm rather than the exception.

Real-World Examples of On-Chain Credit Scores Enabling Under-Collateralized Loans

- Credora partnered with Clearpool and Obligate in July 2024 to bring on-chain credit scores to DeFi lending. This allows investors to assess risk-adjusted returns and enables under-collateralized loans by providing transparent, real-time credit assessments for institutional borrowers.

- Untangled Finance integrated Moody's Ratings on-chain in March 2025, using zero-knowledge proofs to bring traditional credit data to DeFi. This innovation allows DeFi protocols to offer under-collateralized loans based on verified creditworthiness, bridging the gap between traditional finance and decentralized lending.

- CreDA (Credit DeFi Alliance) enables users to mint Crypto Credit Scores as Credit NFTs (cNFTs) based on their on-chain activity. Through partnerships with platforms like FilDA, these scores unlock access to leveraged and low or no-collateral loans for users worldwide.

- Reputation DAO provides decentralized, verifiable credit scores by analyzing both on-chain accounts and real-world financial data. This system allows users to access under-collateralized loans in DeFi by leveraging their blockchain reputation and traditional identity.

- RociFi offers Non-Fungible Credit Scores (NFCS) that classify users' on-chain behavior on a scale from 1 to 10. These scores are used by DeFi lenders to offer under-collateralized loans, improving capital efficiency and expanding access to credit based on blockchain transaction history.

The numbers speak for themselves: market analysts predict that as on-chain credit infrastructure matures, trillions of dollars in untapped capital could flow into DeFi lending markets. This isn’t just about efficiency, it’s about creating a fundamentally fairer system where opportunity is unlocked by merit and transparency rather than gatekeeping or geography.

What’s Next? The Road Ahead for On-Chain Credit Scoring

The next phase will see even deeper integration between DeFi trust scores and mainstream finance. Expect further collaboration between blockchain projects and established rating agencies, along with advances in privacy-preserving analytics that let users control their data footprint while still proving their reliability.

If you’re interested in diving deeper into how decentralized reputation systems work under the hood, or want actionable steps for building your own crypto credit profile, explore our guides like How On-Chain Credit Scores Are Transforming DeFi Lending: Risks, Benefits and Use Cases.

The future of DeFi lending isn’t just more open, it’s smarter, safer, and more inclusive thanks to transparent on-chain reputation systems. As these tools evolve alongside advances in privacy tech and cross-protocol interoperability, expect your crypto wallet’s history, not just your holdings, to unlock new worlds of financial possibility.

No comments yet. Be the first to share your thoughts!