Decentralized finance (DeFi) is at a pivotal crossroads. While overcollateralized lending has powered the sector's growth to date, this model inherently restricts access for users lacking significant crypto holdings. As DeFi matures, the emergence of on-chain credit scores is fundamentally changing the landscape, enabling undercollateralized loans that promise broader financial inclusion and greater capital efficiency. The question is no longer if, but how fast this transformation will reshape crypto lending.

The Capital Efficiency Dilemma in DeFi Lending

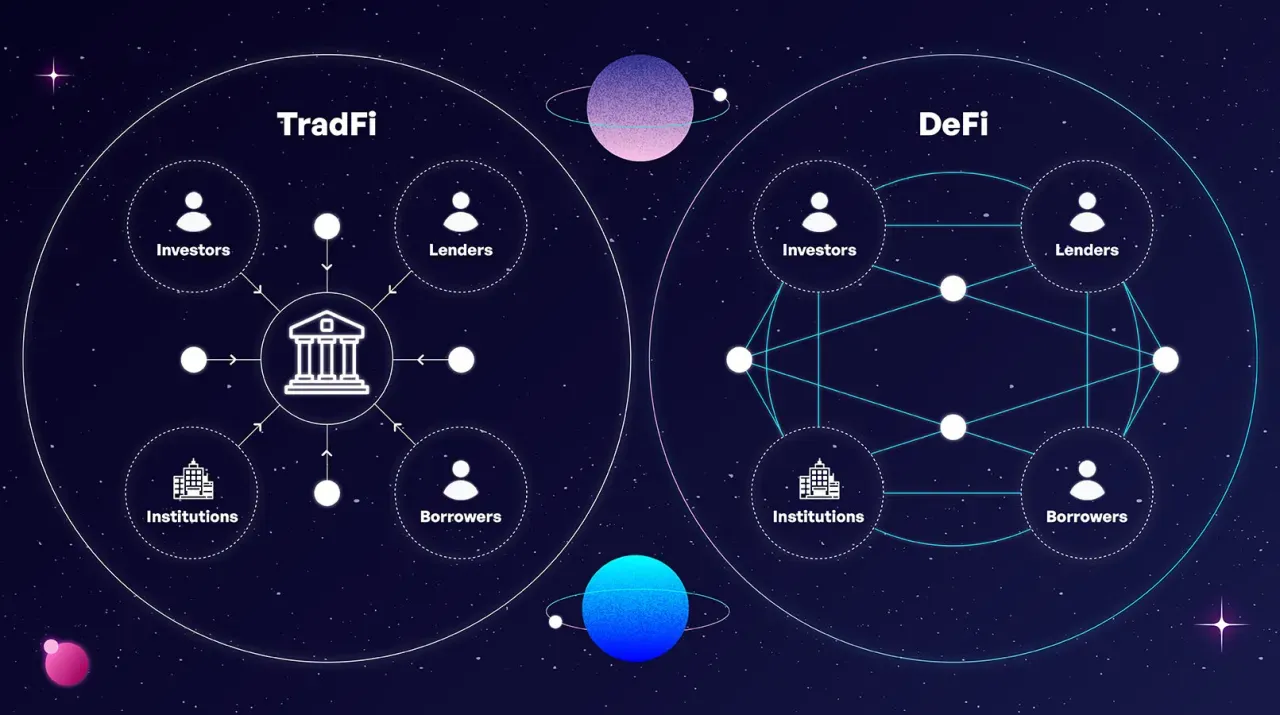

Traditional DeFi lending protocols require borrowers to lock up assets worth more than their loan amount. This approach, while effective at minimizing default risk, results in poor capital utilization and leaves out millions who cannot afford hefty collateral requirements. According to recent industry analysis, over 90% of all DeFi loans remain overcollateralized, a figure that underscores both the security and inefficiency of current systems.

For many potential participants, especially those in emerging markets or new to crypto, these barriers are insurmountable. The need for more inclusive solutions has never been clearer. Enter on-chain credit assessment: a data-driven alternative that leverages blockchain transparency to quantify borrower risk without demanding excessive collateral.

How On-Chain Credit Scores Work

An on-chain credit score DeFi system analyzes a user's blockchain history, wallet activity, repayment patterns, protocol interactions, to generate a probabilistic measure of creditworthiness. Unlike legacy credit bureaus, these scores are transparent and privacy-preserving by design. Protocols such as Cred Protocol and Spectral Finance have pioneered decentralized models: Cred quantifies on-chain risk for underserved communities, while Spectral’s Multi-Asset Credit Risk Oracle (MACRO) provides FICO-like scores based on transaction data.

This shift toward algorithmic reputation is not merely theoretical; it’s already powering real-world use cases. Platforms like RociFi employ machine learning on Polygon to enable zero- and undercollateralized loans by dynamically calculating loan risk from borrowers’ blockchain footprints, a major leap forward for blockchain reputation lending.

Pioneers of Undercollateralized Crypto Loans

The integration of decentralized credit scoring has catalyzed the rise of undercollateralized lending platforms targeting both crypto-native entities and real-world borrowers:

Leading Platforms for Undercollateralized DeFi Loans

- Goldfinch — Goldfinch enables undercollateralized loans to real-world businesses, especially in emerging markets, by combining off-chain credit assessments with on-chain lending. Its approach expands access to capital for borrowers lacking substantial crypto collateral.

- Maple Finance — Maple uses a pool-delegate model where decentralized credit underwriters vet and approve undercollateralized loans to crypto-native companies. Lending decisions are supported by off-chain due diligence and executed via smart contracts.

- RociFi — Built on Polygon, RociFi leverages on-chain data and machine learning to assign credit scores, enabling both zero and undercollateralized loans. The protocol uses borrower history and risk analytics to inform lending decisions.

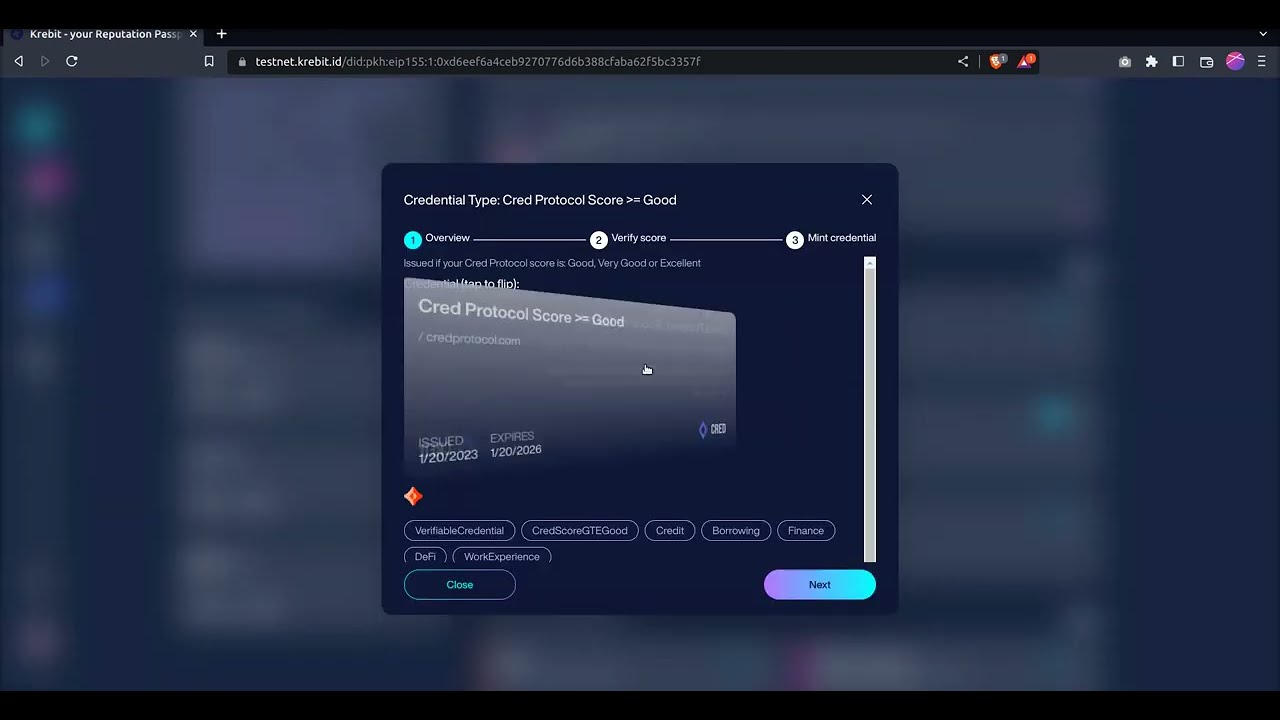

- Cred Protocol — Cred Protocol focuses on decentralized on-chain credit scoring to assess borrower risk, aiming to make undercollateralized lending accessible to underserved communities. Its credit scores are used by lenders to evaluate risk transparently.

- Spectral Finance — Spectral introduces the Multi-Asset Credit Risk Oracle (MACRO) score, which quantifies creditworthiness using on-chain transaction data. This enables lenders to offer undercollateralized loans based on a borrower's blockchain history.

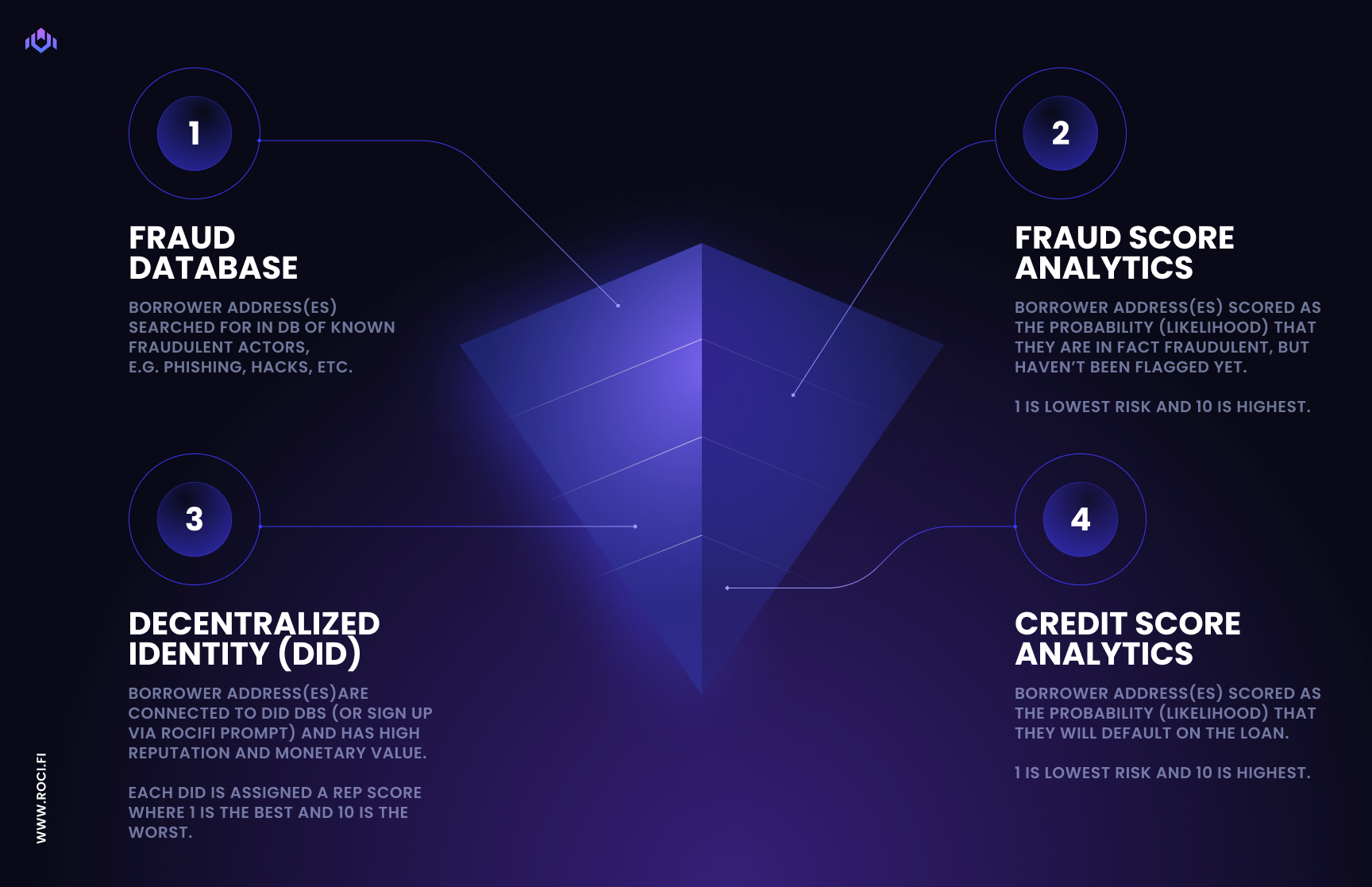

- Chainlink DECO — Chainlink's DECO protocol provides privacy-preserving credit attestation using zero-knowledge proofs, allowing borrowers to prove off-chain creditworthiness for undercollateralized loans without revealing sensitive data on-chain.

- Goldfinch: Focuses on real-world borrowers in emerging markets using off-chain assessments combined with on-chain execution.

- Maple Finance: Utilizes pool delegates, decentralized groups performing due diligence, to approve loans for vetted organizations.

- RociFi: Leverages machine learning models on Polygon to dynamically price loan risk based on user activity across multiple protocols.

This new breed of lending protocol does not simply replicate TradFi’s unsecured lending; it innovates by using transparent data trails and programmable logic to automate trust and risk management at scale. As highlighted by recent research (see here), these advances are rapidly compounding into a credible asset class with growing product-market fit.

The Technology Behind Modern DeFi Credit Assessment

The technical backbone enabling undercollateralized crypto loans is multifaceted:

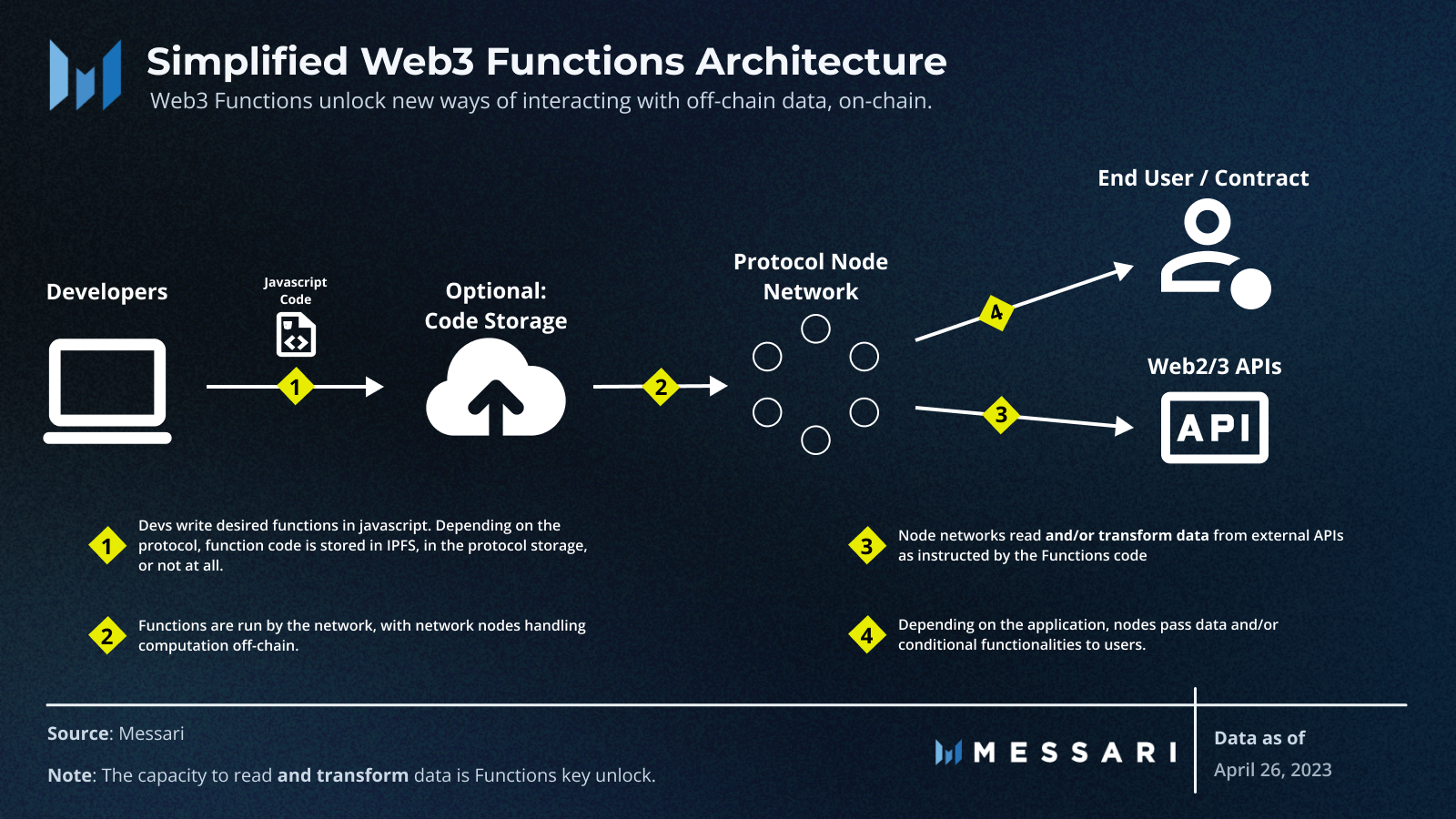

- Zero-Knowledge Proofs (ZKPs): Solutions like Chainlink’s DECO allow verification of off-chain credentials without exposing sensitive information publicly.

- Soulbound Tokens (SBTs): These non-transferable tokens can represent immutable reputation or identity markers tied directly to a wallet address, an emerging trust primitive in Web3 lending ecosystems.

Together, these innovations create robust mechanisms for assessing borrower reliability while preserving privacy, a critical factor for mainstream adoption. For an in-depth technical review, see our coverage on emerging trends in under-collateralized lending using blockchain data.

As these technologies mature, the convergence of on-chain data analytics, privacy-preserving cryptography, and programmable smart contracts is setting new standards for DeFi credit assessment. The result: a dynamic risk pricing environment where borrowers are incentivized to build positive blockchain reputations, and lenders can more confidently allocate capital without rigid collateral constraints.

Managing Risk and Governance in Undercollateralized Lending

With opportunity comes risk. Unlike overcollateralized models, undercollateralized crypto loans expose lenders to greater default potential. This puts the spotlight squarely on the accuracy and robustness of on-chain credit scores. Protocols are increasingly integrating real-time monitoring tools, automated liquidation mechanisms, and decentralized governance frameworks to mitigate these risks.

For example, platforms may employ continuous health factor checks, a metric derived from borrower activity and protocol-specific risk parameters, to trigger protective actions if a position deteriorates. Decentralized autonomous organizations (DAOs) also play a pivotal role by collectively overseeing risk models, updating scoring algorithms, and enforcing transparent dispute resolution processes. Such governance innovations are essential for scaling trust in blockchain reputation lending.

Top Risk Management Strategies in DeFi Undercollateralized Lending

- On-Chain Credit Scoring Systems: Protocols such as Cred Protocol and Spectral Finance use blockchain transaction histories to generate decentralized credit scores, enabling precise borrower risk assessment before issuing undercollateralized loans.

- Decentralized Credit Underwriting Pools: Platforms like Maple Finance utilize pool delegates—decentralized groups of credit underwriters—to conduct rigorous due diligence and ongoing monitoring of borrowers, mitigating default risk.

- Off-Chain Data Integration via Oracles: Chainlink's DECO protocol leverages zero-knowledge proofs and oracles to securely incorporate off-chain credit data, allowing lenders to verify borrower information without compromising privacy.

- Real-World Credit Assessment Partnerships: Goldfinch partners with trusted off-chain entities to perform borrower credit checks and due diligence, combining real-world insights with on-chain lending for enhanced risk management.

- Non-Transferable Identity Tokens (Soulbound Tokens): Emerging DeFi protocols are exploring Soulbound Tokens (SBTs) to represent verifiable, non-transferable on-chain identities, strengthening borrower reputation and reducing the risk of fraud.

The Road Ahead: Real-World Impact and Market Expansion

The shift toward undercollateralized lending is already unlocking capital for previously excluded segments, small businesses in emerging economies, first-time crypto users, and innovative startups. By lowering entry barriers through reliable credit scoring mechanisms, DeFi can drive true financial inclusion at global scale.

Yet challenges persist: cross-chain identity fragmentation complicates holistic credit assessment; evolving attack vectors require continuous protocol hardening; and regulatory clarity remains elusive in many jurisdictions. Addressing these hurdles will demand ongoing collaboration between developers, auditors, data scientists, and policymakers.

Still, the trajectory is clear. As more protocols adopt advanced on-chain credit assessment tools and integrate off-chain data sources securely via ZKPs oracles like DECO, the market for undercollateralized crypto loans is poised for exponential growth. Industry estimates suggest that as on-chain reputation matures into a credible alternative to traditional FICO-style ratings, and as interoperability improves, trillions of dollars could flow into DeFi credit markets over the next decade.

Key Takeaways for Users and Builders

- Borowers: Building an on-chain reputation is now an asset, consistent positive activity can unlock access to cheaper capital with lower collateral requirements.

- Lenders: Leveraging decentralized credit scores enables smarter risk-adjusted returns while expanding your addressable market beyond whales with deep pockets.

- Developers: Integrating transparent scoring systems and robust governance models is critical for sustainable protocol growth in this new paradigm.

The transformation underway is not just technical, it’s cultural. By replacing opaque gatekeeping with transparent algorithmic trust, DeFi is redefining what it means to assess risk in global finance. For deeper insights into how on-chain scores are powering this revolution, and practical guidance on integrating these tools, see our detailed analysis at Crypto Credit Scores.

No comments yet. Be the first to share your thoughts!