Why DeFi credit scores matter now

The decentralized finance landscape is undergoing a structural shift. For years, the dominant model for crypto lending relied on over-collateralization, requiring borrowers to lock up more assets than they intended to borrow. This safety mechanism, while effective at preventing insolvency, severely limited capital efficiency and excluded users with significant on-chain activity but insufficient liquid collateral.

On-chain credit history is changing this dynamic by enabling under-collateralized lending. By analyzing transaction patterns, repayment history, and wallet behavior, protocols can now assess borrower risk without requiring excessive collateral locks. This transition mirrors the evolution from traditional FICO-based lending to alternative credit scoring models, but operates entirely within the transparent, immutable environment of blockchain networks.

The implications for market liquidity are substantial. When borrowers can access capital without tying up their entire portfolio, capital efficiency increases across the ecosystem. This allows for more sophisticated financial strategies and broader participation in DeFi markets. As protocols integrate these credit scores, the barrier to entry for credit-worthy users lowers, potentially driving significant volume shifts in lending markets.

To understand the broader market context in which these credit mechanisms operate, it is useful to observe the asset classes most commonly involved in these lending protocols. The volatility and performance of underlying assets directly impact risk models and lending rates.

This shift from collateral-heavy to behavior-based risk assessment represents a maturation of DeFi infrastructure. As these systems become more robust, they bridge the gap between traditional financial trust models and decentralized innovation, creating a more inclusive and efficient lending environment.

How on-chain credit history works

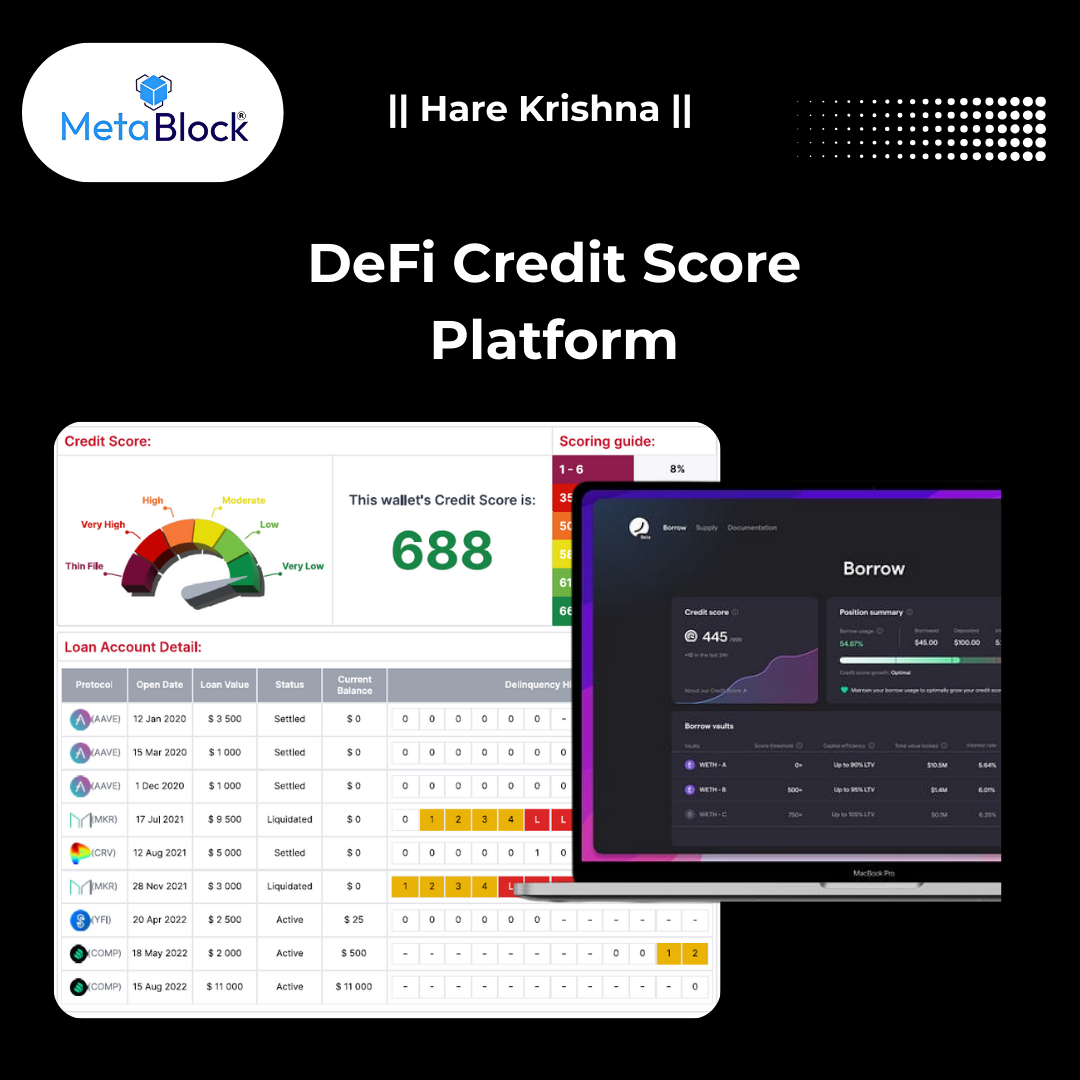

A DeFi credit score is an algorithmic representation of a wallet’s financial behavior and reliability. Unlike traditional FICO models that rely on private bureau data, these scores evaluate public ledger activity. The system quantifies credit risk by analyzing lending history, repayment consistency, and the stability of collateral positions across decentralized protocols.

The calculation typically rests on three core pillars: payment history, regularity, and collateral proximity. Length of payment history measures how long a wallet has maintained active positions. Regularity assesses the consistency of repayments, flagging irregular patterns that suggest liquidity stress. Collateral proximity evaluates the ratio of borrowed assets to deposited value, providing a real-time snapshot of solvency.

Recent academic frameworks, such as the On-Chain Credit Risk Score (OCCR), treat these metrics as a probabilistic measure. By treating on-chain identity as a trust signal, protocols can adjust interest rates and borrowing limits dynamically. This shift moves lending from static, one-size-fits-all terms to personalized risk pricing based on actual financial conduct.

Leading DeFi Credit Score Platforms

The DeFi credit scoring market has fragmented into specialized protocols, each attempting to solve the same problem: assessing borrower risk without traditional credit bureaus. Unlike FICO, which relies on a narrow slice of consumer debt history, on-chain scores aggregate wallet activity, transaction patterns, and collateral behavior across multiple blockchains. This shift enables under-collateralized lending, a significant departure from the over-collateralized norms that have defined DeFi since its inception.

Three platforms currently dominate the landscape by offering robust integration with major lending markets. ChainAware, Cred, and TrueFi each employ distinct methodologies to calculate trustworthiness, targeting different segments of the crypto economy. Understanding their specific metrics is essential for lenders seeking to mitigate risk and for borrowers aiming to access better terms.

The following comparison highlights the core differences in scoring factors, supported chains, and lending partnerships for the leading providers.

| Platform | Primary Scoring Factors | Supported Chains | Key Lending Partners |

|---|---|---|---|

| ChainAware | Wallet age, transaction volume, DeFi engagement | Ethereum, Polygon, Arbitrum | Various DeFi protocols |

| Cred | On-chain history, debt repayment behavior | Multi-chain | Integrated lending markets |

| TrueFi | Credit score, collateral quality | Ethereum | TrueFi pool |

Improving your crypto loan eligibility

Building a strong on-chain identity requires consistent, verifiable activity. Lenders evaluate your creditworthiness by analyzing the length of your payment history, the regularity of your repayments, and the consistency of your interactions with lending protocols.

Start by borrowing small amounts and repaying them on time. A short but consistent track record is more valuable than a long history of missed payments. Lenders prioritize regularity and consistency when calculating your score.

Avoid relying on a single protocol. Interacting with multiple lending platforms demonstrates a broader financial footprint. This diversity helps lenders assess your risk profile more accurately and reduces the impact of any single platform’s instability.

Keep your collateralization ratios well above the liquidation threshold. Lenders view borrowers who maintain healthy margins as lower risk. This behavior signals financial discipline and reduces the likelihood of forced liquidations.

Many platforms now offer decentralized identity (DID) verification. Completing these steps adds a layer of trust to your profile. It helps lenders distinguish between anonymous actors and verified participants, potentially unlocking better loan terms.

By focusing on these core behaviors, you build a reputation that translates directly into better borrowing conditions. The goal is to create a transparent, reliable history that lenders can trust without relying on traditional FICO metrics.

Risks and regulatory considerations

Decentralized credit scores promise to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive. However, this shift from traditional FICO models introduces significant legal and security complexities. The primary concern is data privacy; unlike centralized bureaus, on-chain history is immutable and public. Borrowers must carefully manage which wallet addresses and transaction histories are linked to their identity, as exposing this data can lead to permanent reputational damage or targeted attacks.

Smart contract vulnerabilities present another critical risk. Credit scoring algorithms often rely on automated logic to determine loan-to-value ratios and liquidation thresholds. If these contracts contain bugs or are exploited, the resulting financial losses are typically irreversible. The transparency that makes DeFi attractive also makes it a prime target for sophisticated actors looking to manipulate credit metrics or drain liquidity pools.

Regulatory frameworks are still catching up to these innovations. The Global Association of Risk Professionals (GARP) notes that while credit scores can minimize counterparty risk, the lack of standardized oversight creates uncertainty. Lenders and borrowers alike must navigate a patchwork of jurisdictional rules regarding data ownership and financial compliance. Until clearer guidelines emerge, participants in decentralized credit systems must exercise heightened due diligence and assume a higher degree of personal responsibility for security.

No comments yet. Be the first to share your thoughts!