How DeFi lending builds on-chain credit

Traditional credit scoring models do not apply to decentralized finance. In the crypto ecosystem, lenders do not rely on FICO scores or bureau data. Instead, they use on-chain history to assess risk. This system evaluates your wallet activity—specifically repayment consistency and collateral health—to determine your borrowing power.

Because crypto loans are typically collateral-based, the barriers to entry are different. You do not need a lengthy approval process or a verified income history. Instead, you must lock up assets to borrow against them. This removes traditional barriers such as credit checks, but it introduces new risks if your collateral value drops.

On-chain credit is more likely to start as wallet reputation. It will probably emerge, just not in the TradFi FICO form people imagine. The first systems to gain traction will likely focus on simple, verifiable data points: did you repay your loan on time? Did you maintain sufficient collateral? These actions build a public, immutable record of your reliability.

Lenders analyze this history to assign a risk profile. A wallet with a clean record of timely repayments and healthy collateral ratios will be viewed favorably. This reputation can lead to better loan terms, higher borrowing limits, or access to uncollateralized loans in the future. Your on-chain behavior is your new credit report.

Steps to establish your lending reputation

Establishing a DeFi lending reputation relies on proving you can manage debt in decentralized finance (DeFi). Unlike traditional credit, which looks at your employment history and income, a DeFi lending reputation is built entirely on your on-chain behavior. You must treat your crypto wallet like a bank account: deposit collateral, borrow responsibly, and repay on time to generate a positive history.

1. Choose a recognized DeFi lending protocol

Not all protocols contribute to credit scoring. To build a score that matters, you must use platforms that integrate with major credit bureaus or on-chain credit scoring models. For example, TransUnion has begun delivering credit scores for users on blockchain-based protocols, bridging the gap between traditional finance and crypto [src-serp-5].

Look for protocols that explicitly mention "credit building" or "on-chain credit scores" in their documentation. Common choices include established lending markets like Aave or specialized credit protocols like TrueFi or Maple Finance, depending on your risk tolerance. Ensure the protocol you choose reports to a bureau you trust or generates a score you can access.

2. Deposit collateral into the protocol

DeFi lending is over-collateralized, meaning you must lock up more crypto than you borrow. This collateral acts as security for the lender. Start by depositing a stablecoin like USDC or a major asset like ETH into your chosen protocol.

Be mindful of the loan-to-value (LTV) ratio. If you deposit $1,000 worth of ETH and the LTV is 70%, you can borrow up to $700. Keep your LTV low (below 50%) to avoid liquidation risks. A lower LTV also signals to credit models that you are conservative and less likely to default.

3. Borrow responsibly

Once your collateral is locked, you can take out a loan. This is the critical step that generates your credit history. Borrow a small amount relative to your collateral to keep your LTV safe.

Use the borrowed funds for their intended purpose, such as liquidity provision or yield farming, but ensure you have a clear repayment plan. Avoid borrowing against volatile assets if you can manage the risk. The goal is to show consistent, manageable debt usage, not to leverage up aggressively.

4. Repay on time to build positive history

Repayment is the most important factor in building your crypto credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date. Even a single late payment can severely damage your on-chain reputation.

As you repay, the protocol records your positive behavior on the blockchain. This history becomes part of your digital identity, making it easier to access larger loans or better terms in the future. Over time, this consistent repayment record forms the basis of your crypto credit score [src-serp-4].

5. Monitor your on-chain credit profile

Regularly check your credit score through the protocol or a third-party service that aggregates on-chain data. This helps you understand how your actions are being perceived by lenders.

If your score is low, look for ways to improve it. This might include diversifying your lending history across multiple protocols, increasing your collateral, or maintaining a longer track record of on-time payments. Consistency is key to building a strong reputation in the decentralized finance ecosystem.

Research and choose a DeFi lending platform that integrates with major credit bureaus like TransUnion or uses on-chain scoring models. This ensures your activity will be recorded and visible to future lenders.

Lock up crypto assets (like ETH or stablecoins) in the protocol. Keep your Loan-to-Value (LTV) ratio low (under 50%) to demonstrate financial prudence and reduce liquidation risk.

Borrow a small amount relative to your collateral. This creates your first debt obligation. Use the funds for a clear purpose and ensure you have the means to repay, avoiding over-leverage.

Repay your loan principal and interest before the due date. Set up automated payments to avoid missed deadlines. Consistent on-time repayment is the primary driver of a positive crypto credit score.

Track your on-chain credit profile. As your history grows, you can take on larger loans or diversify across protocols to strengthen your overall creditworthiness in the DeFi ecosystem.

Common mistakes that hurt your crypto credit score

Establishing a crypto credit score relies on proving reliability through DeFi lending history. Unlike traditional loans, these platforms use overcollateralization to manage risk. However, the margin for error is thin. A single misstep can trigger a liquidation, erase your on-chain reputation, and leave your assets seized.

Ignoring liquidation thresholds

Your loan-to-value (LTV) ratio is the most critical metric in your profile. If the value of your collateral drops, your position becomes undercollateralized. Protocols automatically liquidate these positions to protect lenders. This event is recorded on-chain and signals high risk to any future lender. Maintain a buffer by keeping your LTV well below the protocol’s liquidation threshold, typically under 70% for volatile assets.

Using unstable collateral

Not all crypto assets are equal when building credit. Lenders prefer stablecoins or blue-chip assets like Bitcoin because their values are predictable. Using highly volatile altcoins as collateral introduces unnecessary risk. Price swings can quickly push your LTV into danger zones. Choose collateral that aligns with the loan’s stability requirements to keep your credit profile healthy.

Missing repayment deadlines

While many DeFi loans are interest-only, missing payments or failing to repay the principal by maturity damages your score. Some platforms report late payments to credit bureaus, which can have long-term consequences. Set up automated reminders or use smart contract safeguards to ensure timely repayments. Consistency is the foundation of a strong credit history.

Verify your on-chain credit history

Before applying for larger loans or seeking better terms, you must confirm that your lending activity is accurately reflected in the credit scoring model. Third-party aggregators and protocol dashboards serve as the verification layer, translating raw blockchain transactions into readable reputation metrics.

Start by connecting your wallet to a reputable crypto credit rating provider. These platforms index your on-chain history, looking for consistent repayment behavior, active collateralization, and healthy debt-to-value ratios. Aggregators like Gio Ratings, which deliver daily updated counterparty risk scores powered by on-chain data, provide a clear snapshot of your standing [src-serp-1].

Check for completeness. Ensure that all relevant lending protocols are linked. If you have borrowed from multiple platforms, verify that each history line item appears in your report. Gaps in your lending history can lower your score, as the model interprets missing data as potential risk rather than neutrality.

Finally, review the specific metrics driving your score. Look for indicators like "repayment reliability" or "collateral health." If you spot errors, such as a missed transaction or an incorrectly attributed loan, use the provider’s dispute mechanism to correct the record before submitting your loan application.

Pre-flight verification checklist

-

Connect wallet to primary credit aggregator

-

Confirm all lending protocol histories are indexed

-

Review debt-to-value and repayment metrics

-

Dispute any missing or incorrect transaction data

Frequently asked questions about crypto credit

Establishing a crypto credit score in 2026 relies on on-chain activity, but the mechanics differ significantly from traditional banking. Here are the most common questions about privacy, portability, and how these scores actually work.

Is my lending history private on-chain?

No. Unlike a traditional bank where your credit report is sealed behind a login, every transaction on a public blockchain is visible to anyone. Your repayment history, loan size, and wallet address are permanently recorded. While your legal name isn't attached, your financial behavior is fully transparent. This transparency is why some users prefer centralized platforms that can keep data off-chain.

Can I use my DeFi score at a traditional bank?

Currently, no. Most DeFi lending history is not automatically reported to major credit bureaus like Equifax or TransUnion. However, this is changing. Some protocols are beginning to integrate with traditional credit agencies to report positive repayment history without exposing private data. For now, your DeFi score is mostly useful within the crypto ecosystem for better loan terms on other platforms.

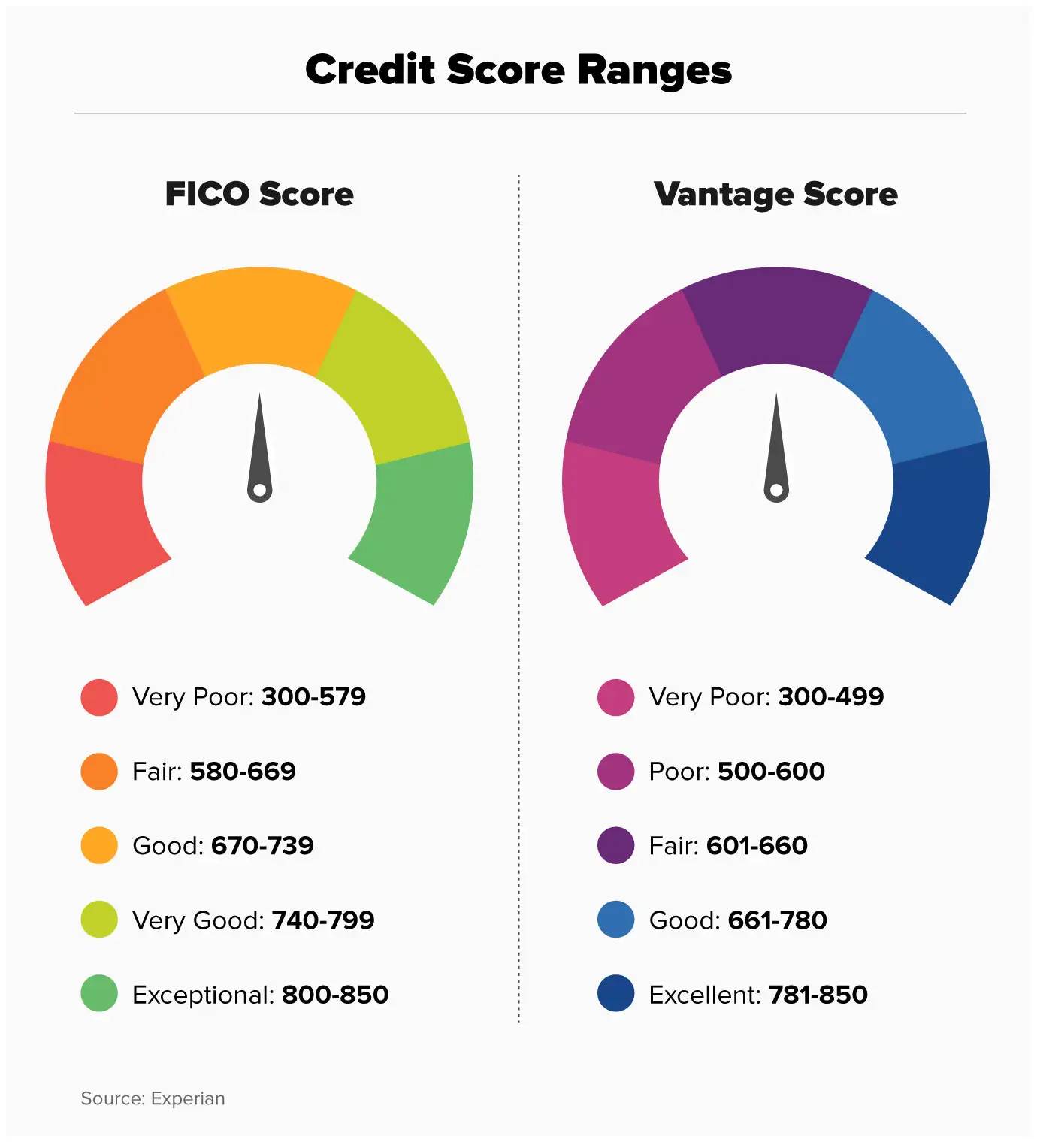

Is a crypto credit score the same as a FICO score?

Not exactly. A FICO score is a single number based on a mix of credit cards, mortgages, and loans. A DeFi credit score is often a reputation metric based solely on your on-chain behavior, such as how consistently you repay loans or how much collateral you hold. It is more like a wallet reputation system than a traditional credit score.

No comments yet. Be the first to share your thoughts!