In the fast-paced world of decentralized finance, traditional borrowing hurdles like sky-high collateral demands are giving way to smarter alternatives. Enter Veera's Financial Identity Score (FIS), an innovative on-chain credit score that turns your blockchain activity into a powerful key for unlocking lower-collateral DeFi loans. Unlike legacy credit systems tied to opaque banks, Veera FIS is fully transparent, dynamic, and under your control, analyzing everything from transaction histories to repayment patterns across chains. This isn't just a score; it's a living profile that rewards responsible DeFi participation with real financial perks, such as reduced collateral ratios and competitive borrowing rates.

Veera, positioning itself as an on-chain neobank, has already garnered massive traction with over 2 million app downloads and 30,000 sign-ups for its Veera Card waitlist. Backed by a recent $10 million funding round from CMCC Titan Fund and Sigma Capital, the platform is expanding globally, especially into emerging markets where financial inclusion remains a challenge. By integrating with protocols like Aave, users can earn yields on stablecoins such as USDC and USDT while building their FIS through non-custodial activities. The result? A seamless bridge between everyday blockchain use and sophisticated lending opportunities.

How Veera FIS Builds Your On-Chain Financial Profile

At its core, Veera FIS functions as a DeFi credit scoring mechanism, drawing from verified on-chain data without relying on centralized KYC overreach. Privacy-focused yet comprehensive, it aggregates your interactions: trades, stakes, loans repaid on time, and even cross-chain movements. Imagine every swap on Uniswap or stake in a liquidity pool contributing positively to your score, creating a blockchain credit bureau entry that's immutable and verifiable by anyone.

This dynamic scoring evolves in real time. A user with consistent, low-risk behavior might see their FIS climb, signaling to lenders a profile worthy of trust. Sources like IQ. wiki highlight how Veera plans this as a cornerstone of its ecosystem, while on-chain research from arXiv underscores the systematic analysis of transaction histories for creditworthiness. It's not static like FICO; it's a reflection of your actual financial behavior in Web3, empowering protocols to offer tailored terms. For instance, higher FIS scores correlate with dynamic interest rates and slashed collateral needs, paving the way for under-collateralized lending.

Veera's approach stands out because it's 100% on-chain, as emphasized on their site. You control it through your actions - no middlemen dictating terms based on outdated data. This transparency fosters trust, crucial in DeFi where billions are at stake daily.

The Shift from Over-Collateralization to Smarter DeFi Lending

DeFi lending today often demands 150-200% collateral to mitigate risks, locking up capital inefficiently. Veera FIS disrupts this by quantifying on-chain reputation, allowing platforms to dial back requirements for proven users. Think of it as earning and quot;crypto loan collateral and quot; credits through activity, not just dumping more assets.

Recent integrations and community buzz, like posts praising Veera's wallet setup and FIS for better investing insights, show real momentum. A higher score doesn't just lower borrowing rates; it unlocks higher loan limits and more rewards, creating a virtuous cycle. As noted in analyses from Block3 Finance, this enables dynamic rates and eventual unsecured loans, potentially injecting trillions into DeFi per Onchain Foundation estimates.

Stafi (FIS) Price Prediction 2027-2032

Forecasts based on Veera's on-chain credit score adoption, DeFi growth, and market cycles from $0.0179 baseline in 2026

| Year | Minimum Price | Average Price | Maximum Price | YoY % Change (Avg from Prev) |

|---|---|---|---|---|

| 2027 | $0.0120 | $0.0280 | $0.0550 | +55.6% |

| 2028 | $0.0180 | $0.0450 | $0.0900 | +60.7% |

| 2029 | $0.0250 | $0.0720 | $0.1450 | +60.0% |

| 2030 | $0.0380 | $0.1150 | $0.2300 | +59.7% |

| 2031 | $0.0550 | $0.1750 | $0.3500 | +52.2% |

| 2032 | $0.0750 | $0.2450 | $0.4900 | +40.0% |

Price Prediction Summary

Stafi (FIS) shows strong long-term potential due to Veera's innovative Financial Identity Score (FIS) enabling lower-collateral DeFi loans. Predictions assume progressive adoption, with average prices rising from $0.028 in 2027 to $0.245 by 2032 (13x from 2026 baseline), factoring in bull cycles in 2028-29 and 2031-32, tempered by potential bear markets.

Key Factors Affecting Stafi Price

- Veera FIS on-chain credit adoption driving DeFi lending volume

- $10M funding and 2M+ app downloads boosting ecosystem growth

- Integrations with Aave and stablecoin yields enhancing utility

- Market cycles: Bull runs in 2028-29 and 2031+ amid Bitcoin halving effects

- Regulatory clarity on DeFi credit scores enabling institutional inflows

- Competition from other credit protocols and overall crypto market cap expansion

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis. Actual prices may vary significantly due to market volatility, regulatory changes, and other factors. Always do your own research before making investment decisions.

I've seen market cycles where overcollateralization stifles growth; Veera's model aligns incentives differently. Responsible users thrive, while risky ones face appropriate hurdles, reducing systemic risks without custodians. Early adopters collateralizing BTC or ETH for instant stablecoin loans via smart contracts are already tasting these benefits, bypassing traditional credit checks entirely.

Key Factors That Boost Your Veera FIS Score

Diving deeper, what specific behaviors elevate your Veera FIS? Repayment history weighs heavily - timely loan settlements signal reliability. Frequency and diversity of interactions matter too; active participation across DeFi protocols demonstrates savvy risk management. Low liquidation events and stable wallet balances further polish your profile.

Veera combines this with platform activity and optional KYC for enhanced accuracy, all while prioritizing privacy. As Metaverse Post reports, it's a cross-chain financial service advancing rapidly. For long-term investors like myself, this builds resilient portfolios by tying credit access to proven on-chain wisdom. Learn more about similar innovations in how on-chain credit scores like Veera FIS unlock undercollateralized DeFi loans.

Long-term holders benefit most here. By maintaining diversified positions and avoiding high-leverage plays, your FIS reflects maturity, much like a seasoned trader navigating cycles without distress sales. I've analyzed countless wallets over 18 years; those with steady inflows and purposeful outflows consistently outperform. Veera quantifies this on-chain, turning data into actionable credit.

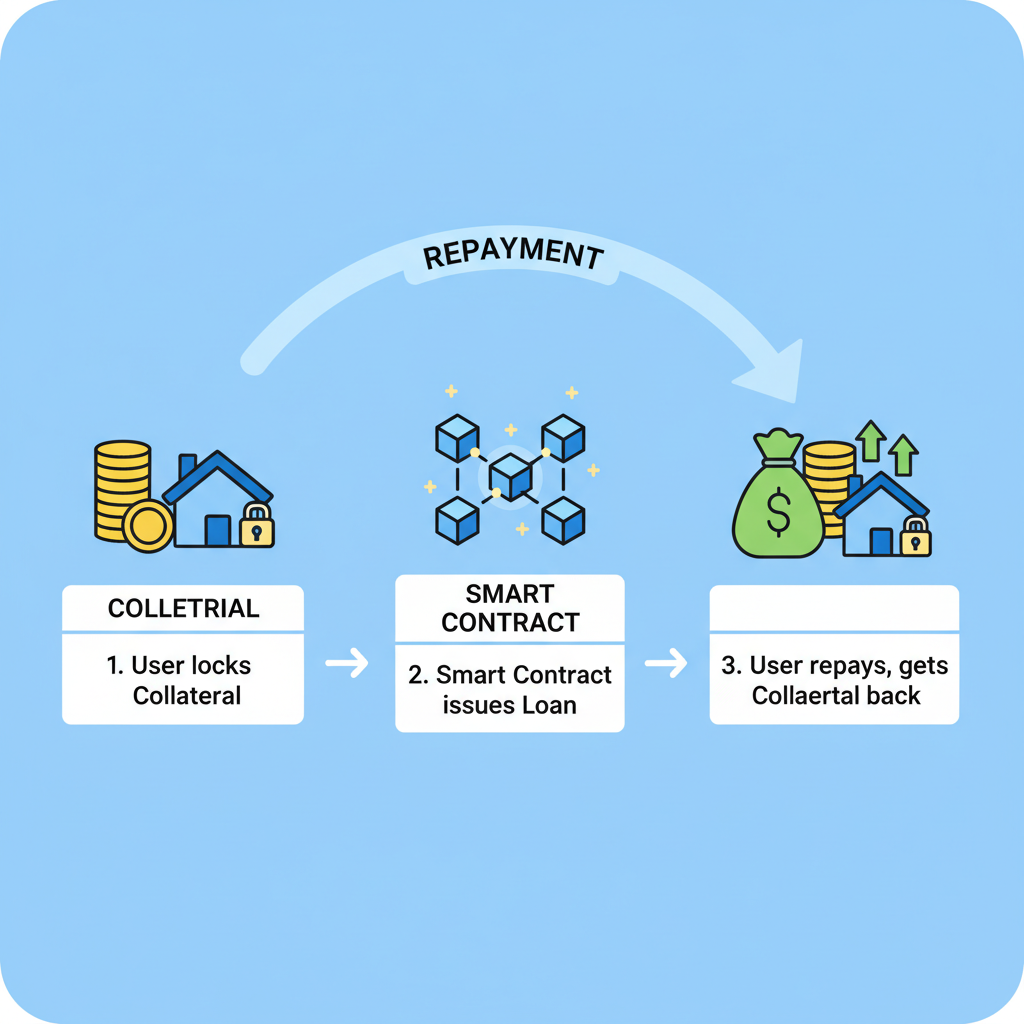

Build Your Veera FIS Score: Unlock Lower Collateral DeFi Loans Step-by-Step

Applying Your FIS: Securing Loans with Minimal Collateral

Once your financial identity score solidifies, the magic happens in borrowing. Platforms integrated with Veera review your FIS alongside collateral. A top-tier score might drop requirements from 150% to 110%, freeing capital for yields elsewhere. For example, collateralize Bitcoin or Ethereum for USDC loans via smart contracts, now with rates adjusted dynamically to your profile. No more overcollateralization locking funds idly; instead, efficient leverage based on proven behavior.

This model scales across chains, thanks to Veera's wallet supporting any network in under 60 seconds. Users report instant stablecoin access, fueling trades or liquidity provision. As DeFi matures, protocols like Aave leverage such scores for non-custodial vaults, where earning on USDT or EURC directly boosts your FIS through responsible participation. It's a feedback loop: better score, better rates, more activity, higher score.

From my vantage, this addresses DeFi's core friction. Traditional finance rations credit via black-box models; Veera FIS democratizes it with verifiable blockchain truth. Emerging markets stand to gain immensely, where billions lack banking but hold crypto. Veera's global push, post its $10 million raise, targets exactly this, blending financial inclusion with Web3 rigor.

Challenges, Risks, and the Path Forward for On-Chain Credit

No system is flawless. On-chain scores hinge on data oracles and chain interoperability, where delays or exploits could skew assessments. Privacy remains paramount; Veera emphasizes zero-knowledge proofs to share scores without exposing full histories. Adoption lags too - most DeFi users stick to collateral-heavy loans from habit. Yet, with 2 million downloads, momentum builds.

Looking ahead, FIS-like innovations could usher undercollateralized lending at scale, as explored in how on-chain credit scores like Veera FIS unlock lower DeFi borrow rates. Trillions await, per forward thinkers, as scores enable unsecured loans for the trustworthy. Stafi's FIS token, trading at $0.0179 with a slight 24-hour dip, underscores ecosystem value even in choppy markets.

For investors building resilient portfolios, engage early. Stake, lend responsibly, watch your score rise. It mirrors macroeconomic prudence: steady accumulation over speculation. Veera FIS isn't hype; it's infrastructure rewarding wisdom in a decentralized world. Platforms evolving with it will define DeFi's next era, where your chain speaks louder than any bank statement.

No comments yet. Be the first to share your thoughts!