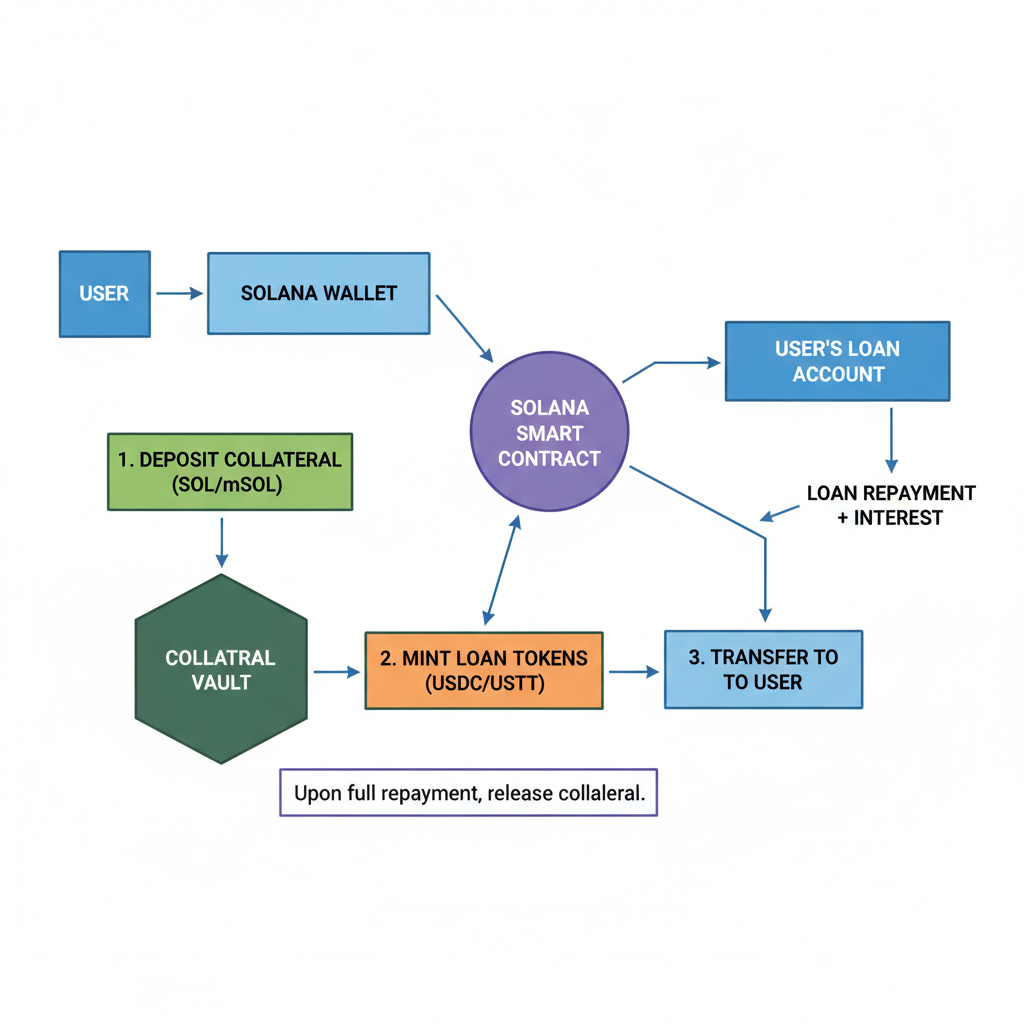

In the high-speed ecosystem of Solana, where transactions zip by at thousands per second, DeFi lending has long grappled with the limitations of overcollateralization. Borrowers must lock up assets far exceeding loan values, stifling access for those without hefty holdings. Enter on-chain credit scores like FairScore, a game-changer for DeFi lending eligibility. Developed by FairScale, FairScore crafts a dynamic crypto reputation score from on-chain activity, social signals, and off-chain data, all privacy-shielded via zero-knowledge proofs. This isn't just scoring; it's a precise gauge of trustworthiness, enabling undercollateralized loans that could unlock trillions in dormant capital.

Solana's fee efficiency, generating around $1 million in chain fees and $12.1 million in app fees recently, makes it ideal for real-time credit evaluation. Protocols can query scores instantly without the drag of Ethereum's gas wars. FairScore exemplifies Web3 credit scoring, quantifying behaviors like consistent repayments, wallet age, and interaction diversity across Solana wallets.

Decoding FairScore's Data Aggregation Engine

FairScore doesn't rely on centralized oracles prone to manipulation. Instead, it pulls from decentralized sources: Solana's transparent ledger for transaction history, social graphs for community standing, and verified off-chain attestations. The result? A probabilistic score reflecting real-time behavior, much like the On-Chain Credit Risk Score (OCCR Score) outlined in recent arXiv and RePEc papers, but tailored for Solana's velocity.

Zero-knowledge proofs are the secret sauce. Users prove score thresholds without revealing underlying data, letting lenders verify eligibility, say, a minimum 750/1000 for prime rates, while keeping wallets pseudonymous. This sidesteps DeFi's cold start problem: no KYC needed, yet creditworthiness shines through on-chain footprints.

FairScore Key Components

- AI-Powered Wallet Analysis: Uses AI to analyze Solana wallet on-chain activity for creditworthiness assessment.

- ZK Privacy Proofs: Employs zero-knowledge proofs to verify reputation scores without exposing sensitive data.

- Real-Time Social/On-Chain Fusion: Aggregates on-chain, social, and off-chain data for dynamic, real-time user scoring.

- Sybil Resistance Metrics: Incorporates metrics to detect and mitigate Sybil attacks in DeFi ecosystems.

- Solana-Native Integration: Designed for seamless integration within the Solana blockchain for DeFi lending protocols.

Solana Wallet Activity Under the Microscope

Consider a typical Solana wallet credit profile. FairScore scans transaction velocity, token diversity, and repayment patterns. Frequent, low-value swaps signal speculation; steady lending/borrowing histories build reliability. AI models, akin to Superteam's DeFi Credit Score build, weigh factors like:

- Wallet vintage and activity consistency

- Interaction with reputable protocols (e. g. , Kamino, Marginfi)

- Cross-chain bridges usage without exploits

- Social proof from Farcaster or X endorsements

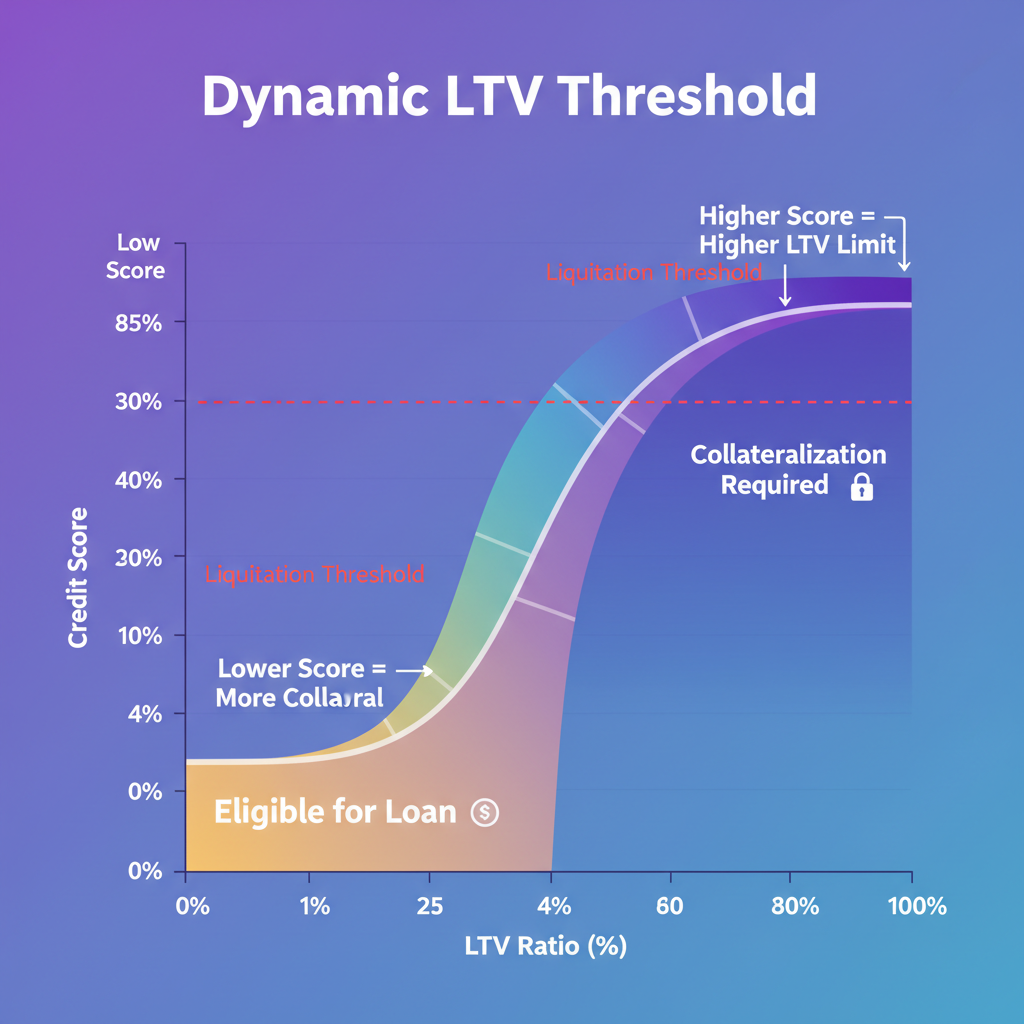

This granular analysis empowers lenders. A wallet with a 850 and FairScore might access loans at 2% APR with 50% collateral, versus 500-score users capped at overcollateralized terms. As Matt Pfeifer notes on Medium, such scores reward responsibility, transforming Solana DeFi from collateral cages to merit-based markets.

Real-Time Eligibility Gates in Action

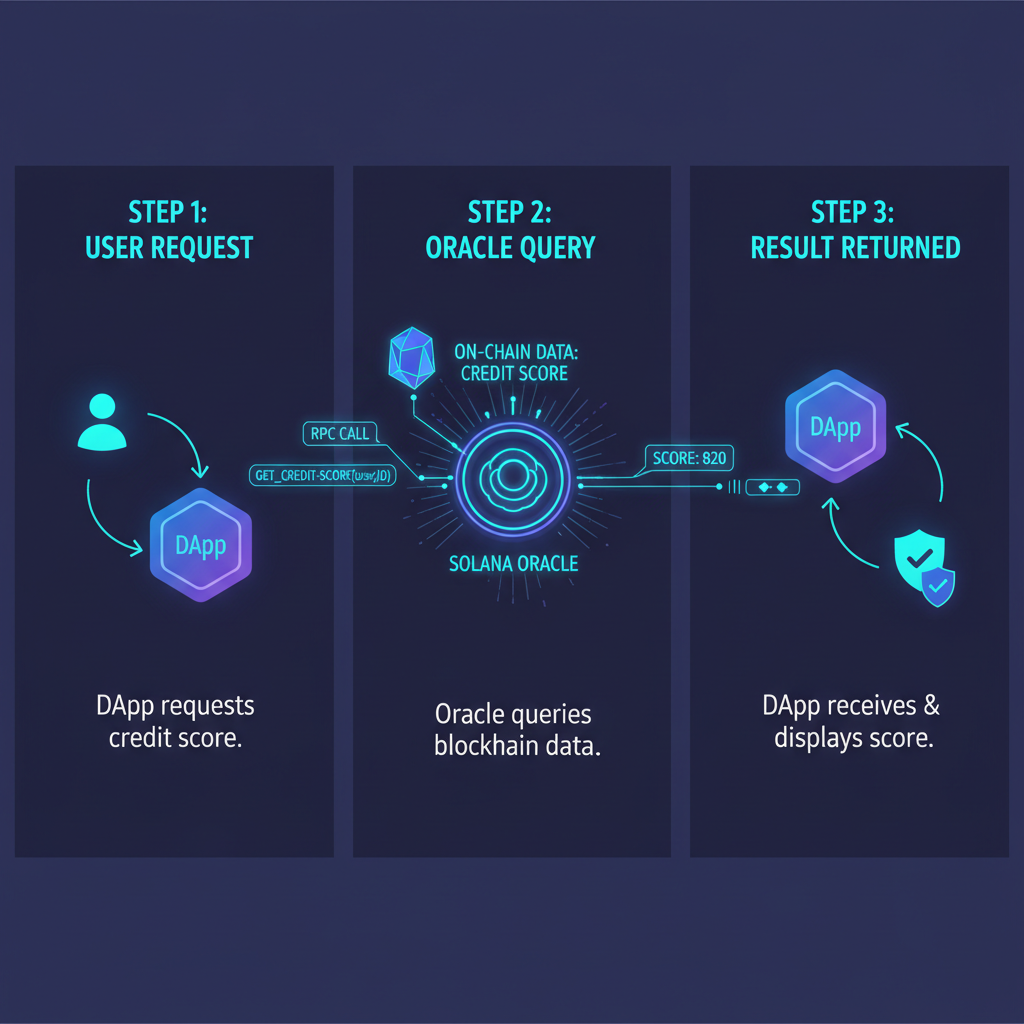

FairScore integrates seamlessly via APIs or oracles into Solana lending dApps. Upon loan request, smart contracts query the score: above threshold? Proceed with adjusted LTV ratios. Below? Prompt collateral top-up or denial. This dynamic gating mitigates Sybil attacks and MEV exploitation, as seen in ICOs and airdrops where low-score wallets get filtered.

Huma Finance's guide to on-chain credit underscores this shift: from rigid collateral to fluid reputation. On Solana, where apps rake in $12.1 million fees, FairScore could slash defaults by 30-50%, per emerging models. Lenders gain risk clarity; borrowers, opportunity without liquidation fears. Yet challenges persist, data silos and oracle reliability demand vigilant auditing.

Integrating FairScore demands robust smart contract logic attuned to Solana's parallel execution. Protocols like those rebuilding credit models on Solana can embed score verifiers, adjusting loan-to-value ratios dynamically. A borrower with a FairScore Solana above 800 unlocks 80% LTV on stablecoin loans, while sub-600 scores trigger full collateral. This precision stems from FairScore's fusion of AI-driven pattern recognition and ZK-verified data feeds, outpacing static models in volatile markets.

Undercollateralized Lending: From Vision to Protocol Reality

The promise of on-chain credit scores lies in undercollateralized DeFi lending, a shift echoed by the Onchain Foundation's projection of trillions in new capital. On Solana, where fee productivity hits $12.1 million across apps, FairScore enables protocols to offer loans at 0-20% collateral based on crypto reputation score. Lenders query scores via oracles, slashing default risks through behavioral predictive analytics. Unlike EigenLayer's zScore or OCCR models, FairScore's Solana-native design leverages high-throughput for sub-second verifications, ideal for flash loans or perpetuals.

Integrate FairScore: Enhance Solana DeFi Lending with On-Chain Credit Scores

Superteam's DeFi Credit Score prototype hints at this future, analyzing wallet heuristics for creditworthiness. Yet FairScore advances further, incorporating social vectors to detect genuine actors amid Sybil noise. Protocols gain a tamper-proof eligibility layer, rewarding wallets with proven track records across Kamino liquidity pools or Marginfi borrows.

Metrics That Matter: FairScore's Scoring Framework

Diving deeper, FairScore assigns weights methodically: 40% on-chain repayment history, 25% interaction diversity, 20% social attestations, 15% risk signals like exploit proximity. This Web3 credit scoring matrix yields a 0-1000 score, with tiers dictating DeFi lending eligibility. High scorers access premium yields; low ones build via micro-actions, fostering upward mobility without KYC barriers.

| Score Tier | LTV Max | Collateral Req. | APR Range |

|---|---|---|---|

| 900-1000 (Elite) | 90% | 10% | 1-3% |

| 700-899 (Prime) | 75% | 25% | 3-6% |

| 500-699 (Standard) | 50% | 50% | 6-12% |

| and lt;500 (High Risk) | 20% | 80% | and gt;12% |

Such tiered access, drawn from emerging Solana lender practices, balances inclusivity with prudence. As AInvest reports, this paradigm expands access, drawing undercollateralized borrowers previously sidelined by overcollateralization.

Risks linger, though. Oracle delays or adversarial data poisoning could skew scores, necessitating multi-oracle ensembles and on-chain audits. FairScale counters with decentralized aggregators, but protocols must stress-test integrations. Reddit discussions on zScore-like systems highlight portability needs; FairScore's ZK portability across chains positions it well.

Looking ahead, as Solana lenders refine these models, Solana wallet credit profiles will dictate DeFi's meritocracy. FairScore isn't merely a score; it's infrastructure for trustless capital flows, propelling Solana toward a collateral-light future where reputation reigns supreme. Protocols adopting it early will capture the trillions in unlocked value, per Onchain Foundation insights, cementing Solana's edge in programmable finance.

No comments yet. Be the first to share your thoughts!