In the bustling world of DeFi as of March 2026, on-chain DeFi scores like the ORBT DeFi Score are quietly reshaping how we think about trust and lending. Forget the days of locking up 150% collateral just to borrow a fraction of your assets. Platforms like ORBT are using three years of your wallet's on-chain history - transactions, protocol interactions, trading volume, even NFT flips - to craft a crypto credit profile that lenders can actually trust. This isn't hype; it's a practical shift toward under-collateralized Web3 lending credit, unlocking doors for users tired of overcollateralized headaches.

Launched in January 2026, ORBT Protocol's system lets anyone generate their DeFi Score by connecting their wallet. It's not just a number; it's a gateway to earning ORBs points through engagement. Higher scores mean more points, creating a flywheel of activity that boosts the entire ecosystem. As DeFi lending hits new highs, these blockchain credit scoring 2026 tools are essential for protocols wanting to lend smarter, not harder.

Why DeFi Still Leans on Collateral - And Why That's Crumbling

Traditional finance has FICO scores honed over decades, but DeFi? It's been a collateral cage. Borrow on Aave or Compound, and you're posting $150,000 in ETH to snag $100,000 USDC. Safe for lenders, sure, but it ties up capital and excludes normies without fat stacks. Sources like ChainAware. ai nail it: overcollateralization solves trust issues in a pseudonymous world, but it stifles growth. DeFi lending surged to $53.6B, outpacing DEXs, yet most of that is locked in inefficiency.

Enter on-chain credit scores. They scan your wallet's behavior - repayment history, liquidity provision, even risk-adjusted trading. Projects like Spectral, backed by General Catalyst and Samsung Next, prove investors see the potential in decentralizing this. ORBT takes it further with a points campaign rewarding historical activity, turning past deeds into future borrowing power. It's pragmatic evolution, not revolution.

Key ORBT DeFi Score Metrics

- Transaction Volume: Total value of on-chain transactions over three years, signaling user activity and liquidity engagement.

- Protocol Interactions: Number and diversity of DeFi protocols used, like lending platforms and liquidity pools, showing ecosystem involvement.

- Repayment History: Track record of loan repayments on platforms like Aave or Compound, building trust for under-collateralized lending.

- NFT Activity: Volume and frequency of NFT trades or holdings, reflecting broader Web3 asset management.

- Engagement Consistency: Steady participation depth over time, earning ORBs points for reliable behavior.

Unpacking the ORBT DeFi Score Mechanics

ORBT doesn't guess; it analyzes. Plug in your wallet, and it pulls three years of data across chains. Depth matters: frequent liquidity pool adds signal reliability over sporadic trades. Consistency is king - steady interactions beat one-off whales. Users earn ORBs based on score tiers, incentivizing deeper involvement. This on-chain DeFi score isn't static; it's dynamic, updating with your activity to reflect real-time creditworthiness.

"On-chain credit scoring bridges traditional lending with DeFi, creating a single, transparent financial ecosystem. " - Duredev on Medium

Compare to Spectral's infrastructure or arXiv's OCCR Score: all aim to quantify wallet risk for protocols. But ORBT's user-first points system makes it accessible. No KYC nonsense, just verifiable on-chain proof. For lenders, it's gold - lower defaults via data-driven decisions. I've crunched enough crypto analytics to say this beats black-box AI models; it's transparent and tamper-proof.

Crafting a Standout Crypto Credit Profile in Web3

Building your crypto credit profile starts with activity, but smart activity. Diversify interactions: lend on multiple protocols, provide liquidity without impermanent loss roulette, repay promptly. NFT holdings? They factor in for diversification signals. ORBT rewards consistency, so set-it-and-forget-it strategies like staking or automated yields shine. Avoid red flags like frequent liquidations or bridge exploits - those tank scores fast.

Check out how on-chain risk scores enable undercollateralized DeFi loans. In practice, a strong ORBT score could slash collateral needs to 110% or less, freeing capital for real yields. Huma Finance echoes this: track liquidity pools and lending to build history. By 2026, this is table stakes for Web3 lending credit; ignore it, and you're sidelined. Platforms experimenting with wallet behavior analysis, per Blockchain App Factory, confirm the trend.

Rebank's lessons from a $1.9B on-chain fund highlight challenges like oracle risks, but scores mitigate that with holistic views. Kava. io's AI twist adds prediction layers, yet ORBT keeps it pure on-chain for trust.

That blend of on-chain purity and behavioral insights positions ORBT as a frontrunner in blockchain credit scoring 2026. Lenders get a fuller picture, borrowers get fairer access. It's the kind of tool that turns DeFi from a speculator's playground into a viable financial system.

How ORBT Integrates with DeFi Lending Protocols

Protocols aren't waiting around. Imagine plugging your ORBT DeFi Score directly into Aave's risk engine or Morpho's matching markets. High scorers borrow at 110% collateral ratios, maybe even dipping under 100% for prime wallets. The Onchain Foundation predicts this unlocks trillions by enabling under-collateralized crypto lending as a real alternative to TradFi gatekeepers. Spectral's infrastructure already powers similar decisions, and ORBT's points campaign accelerates adoption by rewarding early users.

For developers, it's plug-and-play. ORBT exposes APIs for score queries, letting any dApp verify creditworthiness on-chain. No oracles needed beyond standard data feeds. This slashes default rates - think arXiv's OCCR Score applied at scale. I've seen enough risk models to know: when wallets prove reliability over years, lenders sleep better. DeFi's $53.6B lending surge shows demand, but efficiency gains from scores like these will push it higher.

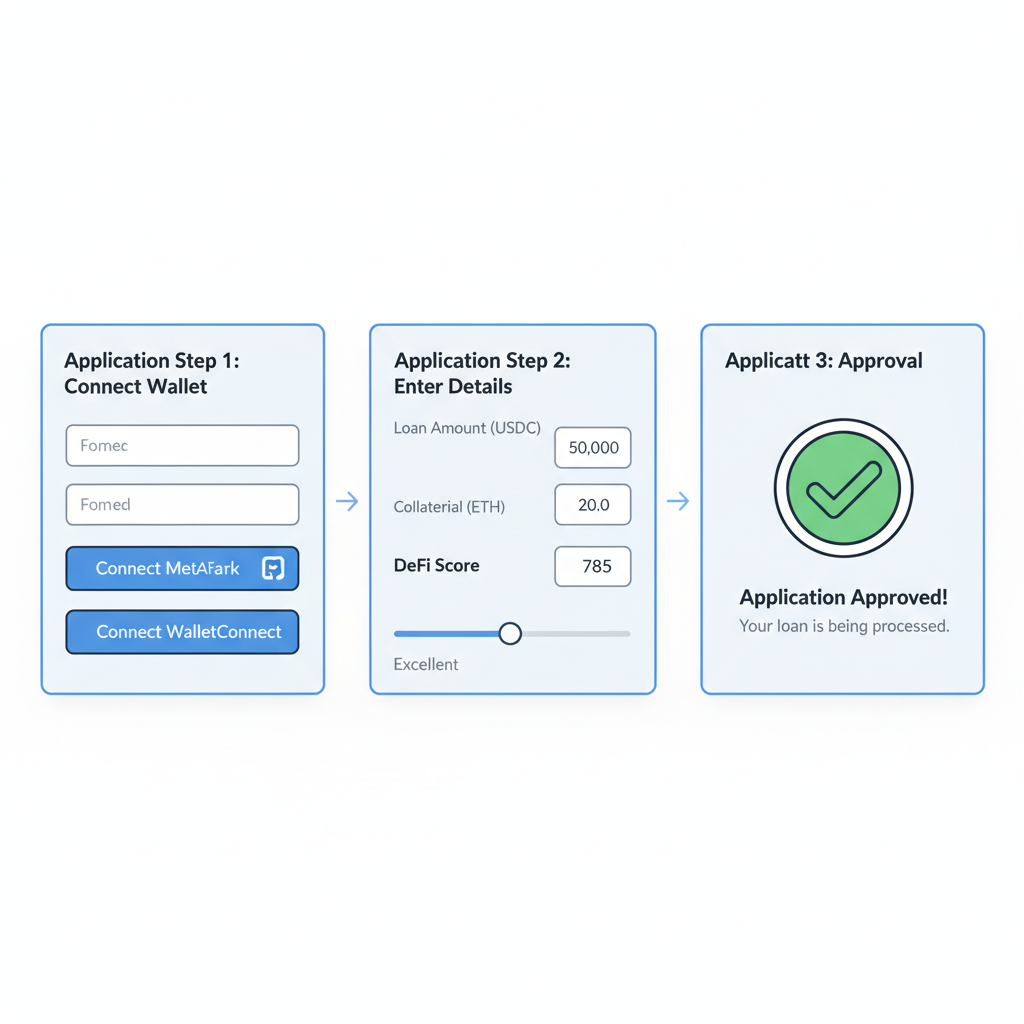

Unlock Your ORBT DeFi Score: Connect, Generate, Earn & Borrow in Web3

Risks and Realities: What Could Go Wrong?

No system's perfect. Sybil attacks? ORBT's three-year history requirement weeds out fresh multis. Gaming the score via wash trading? Consistency checks and volume normalization catch that. Privacy hawks worry about data exposure, but zero-knowledge proofs let you prove scores without revealing full history. Huma Finance's guide stresses this balance: analyze without doxxing.

Lessons from rebank. cc's $1.9B fund ring true here - on-chain credit demands robust oracles and stress-tested models. Yet ORBT sidesteps much of that by sticking to verifiable blockchain events. Kava. io's AI layer tempts, but pure on-chain wins for immutability. My take: start simple, iterate. Overcomplicate, and you lose the Web3 edge.

Users building strong crypto credit profiles today position themselves for tomorrow's opportunities. Stake steadily, lend responsibly, trade with discipline. Your wallet's story matters more than ever. As ChainAware. ai outlines, this beats FICO for DeFi because it's earned through action, not paperwork.

General Catalyst's bet on Spectral signals institutional buy-in, and Samsung Next agrees. Medium voices like Duredev see a unified ecosystem emerging. ORBT's user engagement loop - score to points to perks - makes it sticky. Dive in, generate yours, and watch Web3 lending credit evolve from niche to norm.

By mid-2026, expect ORBT integrations across major protocols, slashing collateral barriers and drawing in sidelined capital. This isn't just scoring; it's scaffolding for a trustless economy where your on-chain deeds open real doors. Platforms tracking liquidity pools and repayments, as Blockchain App Factory notes, confirm the momentum. Get ahead: build that profile now.

No comments yet. Be the first to share your thoughts!