The 2026 shift from collateral to behavior

The landscape of crypto lending is undergoing a fundamental structural change in 2026. For years, the dominant model relied on over-collateralization: you lock up $10,000 of Bitcoin to borrow $5,000 in stablecoins. While this minimized risk for lenders, it trapped capital and excluded anyone without significant upfront assets. The new paradigm, often referred to as crypto credit scores 2026, replaces this brute-force security with behavioral scoring.

This shift moves the industry from simple asset-backed loans to credit-based lending powered by on-chain history. Instead of asking how much collateral you can lock away, lenders now analyze your transaction patterns, repayment consistency, and wallet activity. This approach mirrors traditional finance but uses blockchain data as the primary source of truth, removing the need for lengthy approval processes or centralized credit bureaus.

The impact is immediate. Borrowers can access liquidity without freezing their core holdings, and lenders gain access to a broader, more diverse pool of borrowers. As noted by industry research, this transition is reshaping global credit by removing traditional barriers while introducing more nuanced risk assessments. The result is a market where your on-chain reputation matters as much as your wallet balance.

To understand the scale of this shift, it helps to look at the broader market environment where these products are emerging. The volatility and growth of the underlying assets directly influence lending rates and risk models.

How on-chain credit scoring works

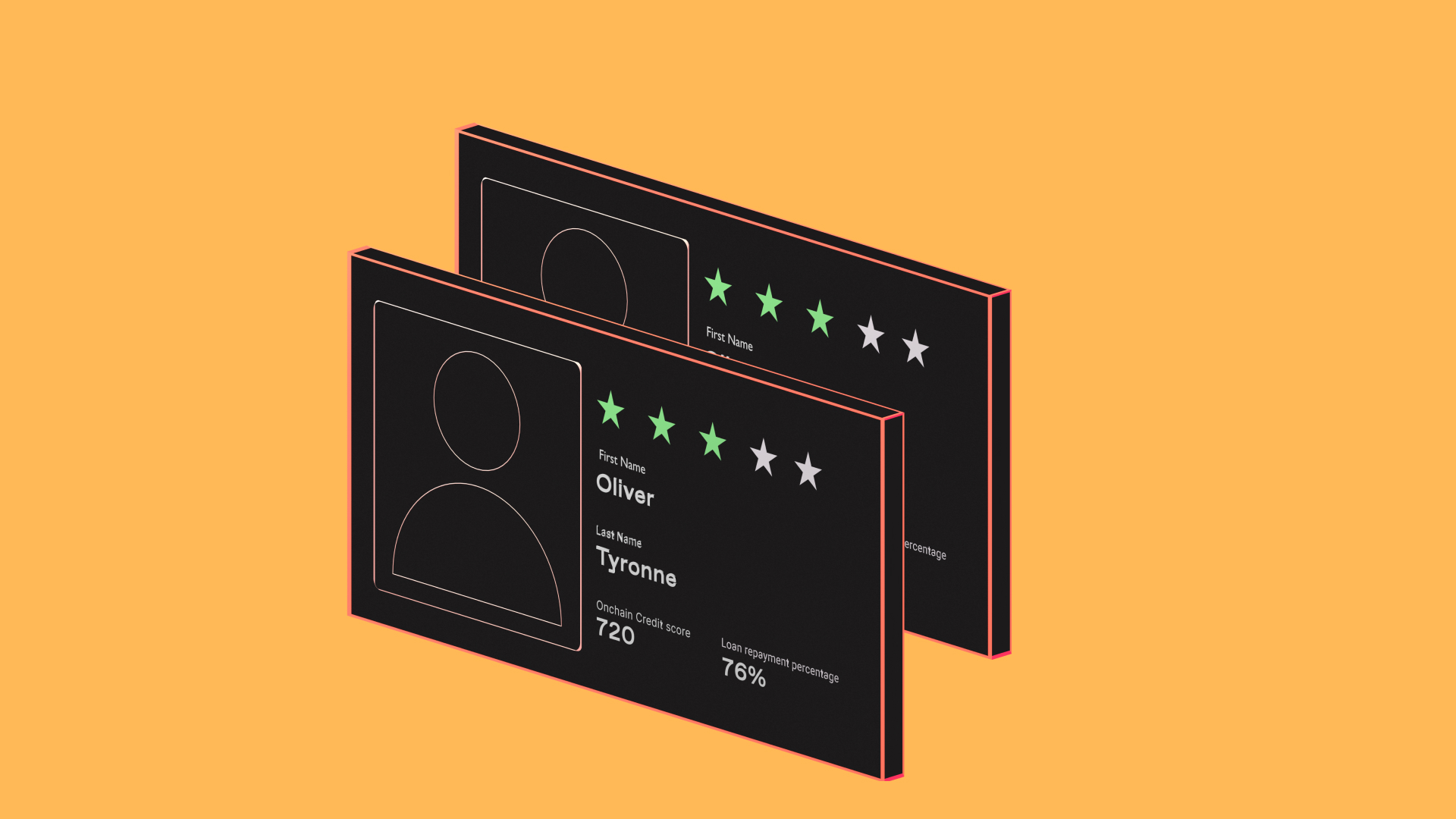

Traditional credit bureaus rely on a narrow set of financial relationships: credit cards, mortgages, and utility payments. In 2026, crypto credit scores replace this limited data with the full breadth of on-chain activity. A numerical assessment of a wallet's creditworthiness is now derived from behavioral data—transaction history, wallet age, and repayment behavior—rather than third-party bureau reports.

This shift transforms how risk is evaluated in decentralized finance. Protocols no longer need to trust a centralized entity's judgment; they verify it through the blockchain itself. The first wave of this technology emerged not as a direct FICO equivalent, but as a wallet reputation system. Over time, these reputation signals have matured into sophisticated scoring models that predict default risk with surprising accuracy.

The mechanics are straightforward. Smart contracts analyze specific on-chain metrics to generate a score. Key factors include the consistency of DeFi repayments, the age of the wallet, and the diversity of assets held. A wallet that consistently repays loans on time across multiple protocols demonstrates reliability that a single credit card statement cannot match.

By focusing on actual transactional behavior, crypto credit scores reduce the friction of underwriting. Lenders can offer terms based on verified history rather than static income statements. This approach is particularly valuable for users with thin credit files, as their on-chain activity provides a rich, verifiable data set that traditional systems often ignore.

Leading tools for building wallet reputation

The landscape for crypto credit scores 2026 has shifted from experimental prototypes to structured data pipelines. Lenders no longer need to guess a wallet's reliability; they can now access standardized risk profiles generated by specialized Web3 infrastructure. These platforms aggregate on-chain history—transaction volume, loan repayment rates, and DeFi interaction patterns—to create a verifiable reputation layer.

Three primary models currently dominate the market, each serving a different segment of the financial ecosystem. Retail-focused tools prioritize user-friendly dashboards that allow individuals to monitor their own scores. Institutional platforms, conversely, offer granular risk ratings for high-volume entities and protocol-level due diligence. Meanwhile, infrastructure providers build the underlying APIs that allow traditional fintech apps to read blockchain data as if it were a traditional credit bureau.

The following comparison highlights the distinct approaches of leading tools in this space. Understanding these differences helps users and lenders select the right infrastructure for their specific needs.

| Platform | Primary Focus | Data Sources | Target Audience |

|---|---|---|---|

| ZestChain | Retail Credit Building | Multi-chain transaction history, DeFi loans | Individuals, Fintech Apps |

| Chainalysis | Institutional Risk | Exchange flows, sanction lists, on-chain patterns | Banks, Regulators, Enterprises |

| DeFi Llama | Protocol Analytics | TVL, yield rates, smart contract interactions | DeFi Users, Researchers |

| Nansen | Smart Money Tracking | Wallet behavior, token flows, insider activity | Traders, VCs, Analysts |

Institutional adoption and market impact

The shift toward crypto credit scores in 2026 is no longer driven by retail speculation but by institutional demand for structured risk management. At Consensus 2026 in Miami, executives from major lenders like Two Prime, Ledn, and Lygos Finance noted that institutional borrowers now prioritize custody solutions and transparent risk ratings above all else. This change marks a departure from the opaque lending practices of previous cycles, replacing them with on-chain history that institutions can audit and trust.

Institutions are integrating crypto credit into broader finance by treating on-chain data as a primary source of truth. Rather than relying on traditional FICO scores, which often fail to capture the financial behavior of crypto-native entities, lenders are using real-time wallet activity to assess creditworthiness. This approach allows for more accurate risk pricing and reduces the reliance on centralized intermediaries that have historically been points of failure in the crypto lending space.

The market impact is visible in the growing liquidity of Bitcoin-backed lending markets. As regulatory clarity improves, traditional finance players are entering the space with tools designed to integrate seamlessly with existing risk frameworks. This institutional adoption is driving the maturation of crypto credit scores, making them a viable alternative to traditional credit systems for both individuals and businesses.

Steps to build a strong DeFi credit profile

Building a strong DeFi credit profile requires treating your wallet like a traditional financial institution would treat a borrower. In 2026, the difference between a wallet that qualifies for low-interest lending and one that gets rejected often comes down to consistent, verifiable behavior rather than the sheer size of your assets. You are not just storing value; you are generating a data trail that algorithms read to assess risk.

Algorithms penalize silence. A wallet that sits dormant for months looks risky because there is no recent data to evaluate. Regular, small transactions—whether they are swaps, swaps to stablecoins, or small payments—signal an active user. This consistency helps establish a baseline of reliability. Treat your wallet like a checking account that needs to show activity, not a savings account buried in a vault.

The single most important factor in your crypto credit score is your repayment history. If you borrow against your crypto holdings, paying back the principal and interest before the due date is non-negotiable. Late payments or, worse, liquidations, are recorded permanently on-chain. These events act as red flags that can drop your score significantly and make future borrowing expensive or impossible. Always monitor your health factors and set up alerts to prevent forced liquidations.

Relying on a single protocol or a single type of token can limit your credit profile. Lending platforms look for a diverse history of interactions across different dApps, stablecoins, and major assets like Bitcoin or Ethereum. This diversity shows that you understand different parts of the DeFi ecosystem and can manage various types of financial instruments. It reduces the perception that your creditworthiness is tied to the volatility of one specific asset.

Just as traditional credit bureaus look at your utilization ratio, DeFi protocols assess how much of your total on-chain wealth is tied up in active debt. A high debt-to-asset ratio suggests you are stretched thin and vulnerable to market downturns. By keeping your leverage low and maintaining a healthy buffer of unencumbered assets, you demonstrate financial stability. This makes you a safer bet for lenders looking for long-term, low-risk borrowers.

While crypto credit scores are primarily on-chain, many protocols in 2026 offer bonus points for identity verification. Using decentralized identity solutions or completing KYC (Know Your Customer) checks on major lending platforms can boost your trust score. This step bridges the gap between anonymous on-chain data and real-world accountability, making your profile more attractive to institutional lenders who require compliance data.

Common questions about on-chain credit

Crypto credit scores 2026 are built on wallet history rather than personal identity. This shift removes traditional barriers like lengthy approval processes, allowing borrowers to access capital based on on-chain behavior. As noted by the Bitcoin Foundation, this trend is reshaping global credit by making borrowing more accessible and transparent.

How do crypto credit scores differ from FICO?

Traditional FICO scores rely on bank data and personal identifiers, whereas crypto credit scores analyze transaction history and wallet reputation. This means your on-chain activity, such as consistent repayments or asset holding, directly influences your creditworthiness without exposing sensitive personal information to centralized institutions.

Will my crypto credit score be portable across chains?

Portability is an emerging challenge. Currently, most scoring models are ecosystem-specific. However, as the industry matures, interoperable standards are being developed to allow wallet reputation to travel across different blockchains, ensuring your credit history isn't locked to a single network.

Is on-chain credit secure and private?

On-chain credit offers enhanced privacy by design. Since scores are derived from public blockchain data rather than personal documents, users maintain greater control over their financial identity. This approach reduces the risk of identity theft associated with traditional credit reporting agencies.

No comments yet. Be the first to share your thoughts!