What crypto credit scores mean in 2026

In 2026, the term "crypto credit scores" no longer refers to a single, universal metric like a traditional FICO score. Instead, it describes a spectrum of reputation systems that bridge two distinct financial worlds: the on-chain ecosystem of decentralized finance (DeFi) and the off-chain infrastructure of traditional finance (TradFi). Understanding this duality is essential for navigating lending and borrowing opportunities in the current market.

On-Chain Reputation: The DeFi Foundation

Within DeFi, creditworthiness is derived entirely from on-chain activity. This system evaluates a wallet's history through transaction volume, repayment consistency, and asset diversity. Unlike traditional credit reports, which rely on static data points like income and employment, these on-chain metrics are dynamic and transparent. Lending platforms use this data to offer under-collateralized loans, allowing users to borrow against their reputation rather than locking up 150% of their assets in collateral.

This reputation is not a single number but a composite of behavioral signals. A wallet that consistently repays loans on time and maintains a healthy debt-to-value ratio builds a higher standing. This standing is portable across various DeFi protocols, creating a fluid credit identity that exists solely within the blockchain ecosystem.

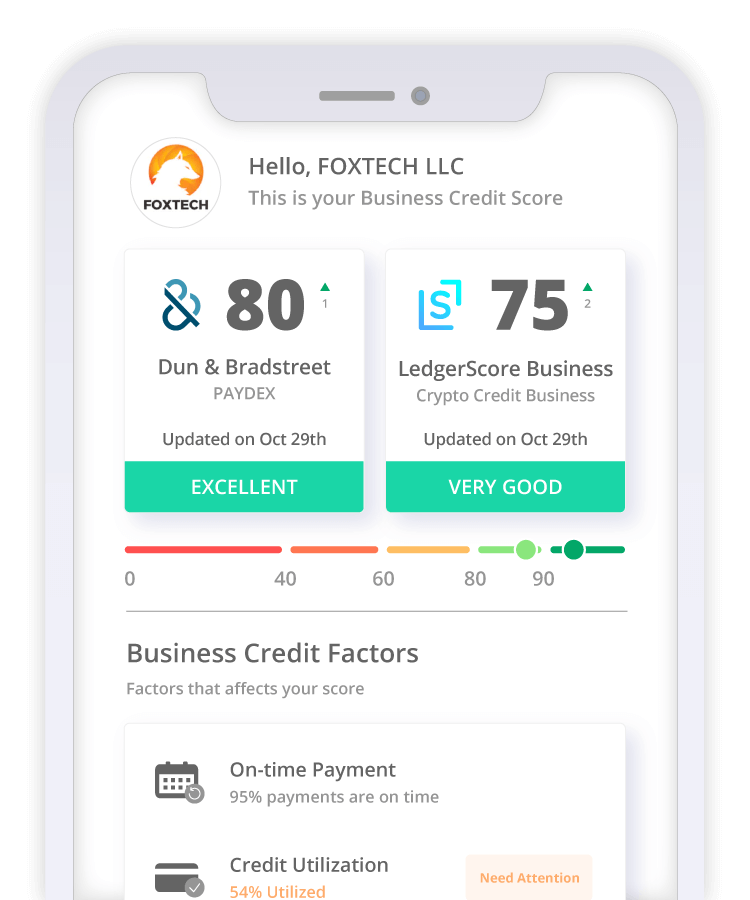

Off-Chain Integration: The TradFi Bridge

The second dimension involves integrating off-chain financial data with on-chain identity. This approach aims to bring traditional credit metrics into the crypto space, allowing users to leverage their established credit history from banks and credit bureaus. This integration is critical for mainstream adoption, as it provides a familiar framework for risk assessment that bridges the gap between legacy finance and decentralized protocols.

Projects working on this integration often partner with traditional credit reporting agencies or use identity verification services to pull in off-chain data. This creates a hybrid model where a user's credit score is influenced by both their on-chain behavior and their off-chain financial responsibility. This dual-layer approach is becoming increasingly common as the lines between DeFi and TradFi continue to blur.

Why the Distinction Matters

The separation between on-chain and off-chain credit scores is not just technical; it impacts accessibility and risk. On-chain scores are accessible to anyone with a wallet, regardless of their location or traditional credit history. However, they may not be recognized by traditional lenders. Conversely, off-chain integrated scores offer broader recognition but require personal data sharing and identity verification, which some users may prefer to avoid.

As the market evolves, the ability to move seamlessly between these two systems will become a key differentiator for users. Those who can leverage both on-chain reputation and off-chain credit history will have access to a wider range of financial products, from DeFi lending pools to traditional mortgage approvals. This dual capability represents the future of credit in a hybrid financial landscape.

How on-chain reputation lowers DeFi borrowing costs

Traditional decentralized finance relies on over-collateralization: you must lock up more crypto than you borrow to protect lenders from volatility. On-chain credit scores change this dynamic by allowing protocols to assess your repayment history directly from your wallet activity. This verified history enables under-collateralized lending, where trusted users can borrow against their reputation rather than their entire portfolio.

When a protocol recognizes a strong on-chain credit score, it reduces the required collateral ratio. This means you keep more of your assets liquid and available for other investments. The effective borrowing cost also drops because the lender faces less risk. This model mirrors traditional credit systems, where a high FICO score leads to better loan terms, but it operates entirely in the open without identity verification.

The market is shifting toward these tranched credit models. According to Galaxy Research, the crypto-collateralized lending market reached $53 billion by mid-2025, with DeFi protocols capturing roughly two-thirds of this volume. As protocols like Aave and Compound integrate more sophisticated risk engines, the gap between traditional mortgage approval and DeFi lending is narrowing.

| Feature | Standard DeFi Loan | Reputation-Based Loan |

|---|---|---|

| Collateral Requirement | 120-150%+ | 50-80% |

| Approval Speed | Instant (automated) | Minutes (verification) |

| Interest Rates | Market-based | Discounted for high scores |

| Risk to Lender | Low (over-collateralized) | Medium (on-chain history) |

This shift requires users to maintain a clean transaction history. Avoiding defaults, repaying loans on time, and engaging consistently with reputable protocols builds the data points needed for these scores. Without this history, you remain in the standard over-collateralized tier, paying higher rates to mitigate the lender's uncertainty.

Traditional lenders integrate blockchain data

The boundary between traditional finance and decentralized assets is thinning. Major credit bureaus and lenders are beginning to incorporate crypto transaction history into mortgage and loan approvals, moving beyond the binary view of crypto as purely speculative collateral. This integration aims to bridge the gap between Web2 credit profiles and Web3 financial activity, allowing borrowers to demonstrate financial responsibility on-chain.

TransUnion has emerged as a primary connector in this space. The credit reporting giant now delivers traditional off-chain credit scores to individuals applying for loans on blockchain-based protocols. This service allows users to prove their creditworthiness without compromising their privacy or exposing their entire on-chain history to the lender. By translating on-chain behavior into recognized credit metrics, TransUnion enables a more nuanced assessment of risk for crypto-native borrowers.

This shift is critical for those seeking to leverage crypto assets for traditional financing. Unlike crypto-backed loans, which are strictly collateral-based and ignore credit scores, traditional mortgage approvals require a holistic view of financial health. Integrating blockchain data allows lenders to see a fuller picture of a borrower's liquidity and transaction history, potentially opening doors for those with thin credit files but strong on-chain activity.

The market is scaling, but scoring lags behind

The convergence of traditional private credit and decentralized finance is creating a massive new liquidity pool, but it is exposing a critical infrastructure gap. Institutional giants like BlackRock and Morgan Stanley estimate the private credit market will exceed $2.3 trillion by 2026, driven by demand for yield in a high-rate environment [[src-serp-6]]. Simultaneously, the crypto-collateralized lending market reached $53 billion by mid-2025, with DeFi protocols capturing roughly two-thirds of that volume according to Galaxy Research [[src-serp-8]].

This capital influx is not just about volume; it is about sophistication. Traditional banks are entering the space to offer crypto-backed loans to high-net-worth clients, while DeFi protocols are moving beyond simple overcollateralization to offer unsecured or semi-secured lending products. However, these institutions lack a unified method to assess borrower risk. Without standardized credit scoring, lenders cannot accurately price risk or determine loan-to-value ratios for complex, multi-chain collateral.

The result is a market where capital is abundant but allocation is inefficient. Institutional lenders require granular, on-chain credit data to underwrite loans at scale, yet most DeFi protocols still rely on binary collateral checks. This mismatch creates a bottleneck. As the market moves toward $2.3 trillion in private credit, the ability to generate accurate, verifiable credit scores will determine which platforms can capture institutional flow.

To understand the volatility context that makes credit scoring so difficult, consider the price action of the primary collateral asset in this space.

Risks and regulatory considerations

Adopting crypto credit scores introduces distinct vulnerabilities that traditional lending models largely avoid. The primary concern is data privacy. Unlike a FICO score, which aggregates anonymized data from banks, on-chain scoring often relies on transparent wallet histories. This means your financial behavior is permanently visible to anyone who can read the blockchain, creating a tension between credit transparency and personal privacy.

Regulatory uncertainty further complicates adoption. While the White House has examined how digital assets affect traditional banking, specific frameworks for on-chain credit scoring remain undefined. This lack of clarity means lenders and borrowers operate in a gray area where consumer protections may not yet apply.

Algorithmic bias is another critical risk. Scoring models trained on historical DeFi data may penalize users based on their wallet age or transaction patterns rather than actual repayment ability. This can create a feedback loop where early adopters benefit disproportionately while newer participants face higher barriers to entry.

Checklist for evaluating crypto credit options

Before committing capital or personal data, verify how a platform calculates its crypto credit scores. Unlike traditional FICO models, onchain credit often relies on wallet reputation, transaction history, and collateralization ratios rather than just off-chain debt records.

- Collateral requirements: Determine if the loan is overcollateralized (requiring more crypto as security) or undercollateralized (using onchain credit scores). Overcollateralized loans are standard in DeFi, while undercollateralized options are emerging but riskier.

- Data privacy: Check if the platform uses traditional credit bureaus like TransUnion or relies solely on onchain data. Privacy-focused platforms may not access off-chain identity, keeping your traditional credit score untouched.

- Interest rate structure: Compare fixed vs. variable rates. Crypto lending rates fluctuate with market liquidity, so understand how rate adjustments are triggered.

- Liquidation thresholds: Review the health factor and liquidation price. A lower threshold means you have more room for price volatility before losing collateral.

- Platform reputation: Verify the protocol’s audit history and total value locked (TVL). Established platforms with transparent governance reduce smart contract risk.

Confirm if the loan requires overcollateralization. Most DeFi platforms require you to lock more crypto than you borrow to mitigate volatility risk.

Determine if the platform uses onchain wallet history or traditional credit bureau data like TransUnion. This impacts your privacy and approval speed.

Understand the health factor and liquidation price. A lower threshold gives you more buffer against market swings before your collateral is seized.

No comments yet. Be the first to share your thoughts!