Why on-chain credit matters now

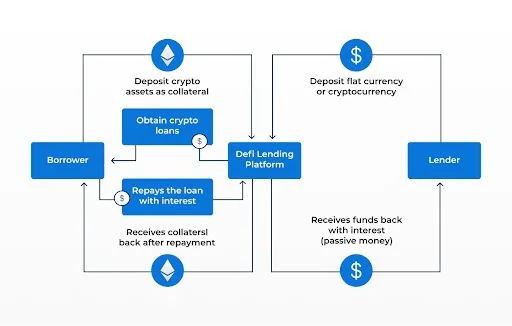

The crypto lending landscape in 2026 is undergoing a structural shift from purely collateralized systems to reputation-based models. This transition is driven by institutional adoption and increasing regulatory clarity, which demand more sophisticated risk assessment than simple over-collateralization can provide. Traditional DeFi lending, which relies heavily on locking up assets to secure loans, is being supplemented by on-chain credit scores that evaluate borrower behavior across multiple protocols.

Institutional players require infrastructure that mirrors traditional finance without the friction of centralized intermediaries. Galaxy’s recent market analysis highlights the rise of on-chain prime infrastructure, which enables sophisticated credit strategies for large-scale participants. These systems analyze on-chain activity—such as repayment history, asset diversity, and transaction frequency—to generate a creditworthiness score. This allows borrowers to access liquidity without tying up all their capital in collateral, improving capital efficiency for both individuals and institutions.

Regulatory frameworks are also pushing the industry toward greater transparency and accountability. By establishing clear standards for on-chain credit reporting, regulators are creating a more stable environment for credit products. This reduces the risk of systemic failures caused by opaque lending practices and encourages broader adoption of crypto credit as a legitimate financial tool. The result is a market where credit is no longer just about what you hold, but how you manage it.

How wallet reputation replaces FICO

Traditional credit scoring relies on a centralized, siloed dataset: bank statements, loan repayment history, and utility bills. The "crypto-native credit score" operates on a fundamentally different architecture. It aggregates on-chain activity—transaction history, collateralization ratios, and repayment behavior—into a wallet reputation profile. This model shifts the burden of proof from a central authority to the blockchain itself, where every action is immutable and publicly verifiable.

The mechanism begins with data collection. Unlike FICO, which requires explicit permission to access off-chain financial records, on-chain data is transparent by default. Lending protocols analyze a wallet’s historical interactions with decentralized finance (DeFi) platforms. Did the user consistently maintain healthy collateralization ratios? Did they repay loans on time across multiple protocols? These patterns form the basis of the reputation score. For example, a wallet that has successfully navigated volatile market conditions without liquidation demonstrates a higher risk tolerance and financial discipline than one that relies on static income verification.

This distinction is critical for understanding the structural shift in credit assessment. Traditional models penalize thin-file users—those with little to no credit history—because the absence of data is interpreted as high risk. On-chain reputation models treat activity as signal. A wallet with six months of consistent, low-value transactions may be deemed more reliable than a wallet with a decade of dormant activity. The score is not a single number but a dynamic profile that updates in real time as the wallet interacts with the blockchain.

| Dimension | Traditional FICO | On-Chain Reputation |

|---|---|---|

| Data Source | Centralized banks, credit bureaus | Public blockchain ledgers |

| Privacy | Requires explicit consent, opaque | Transparent by default, pseudonymous |

| Accessibility | Limited to formal financial history | Open to any wallet with activity |

| Update Frequency | Monthly or quarterly | Real-time |

The result is a more inclusive, yet technically complex, underwriting process. By leveraging on-chain behavior, lenders can offer under-collateralized loans to users who would otherwise be excluded from traditional finance. This does not eliminate risk; it redefines it. The risk is no longer based on past income stability but on current on-chain conduct. As the market matures, these reputation scores will likely become the standard for DeFi lending, replacing the outdated FICO model for a significant portion of the global population.

DeFi protocols enabling uncollateralized loans

The integration of on-chain reputation into DeFi lending protocols marks a structural shift from asset-backed security to behavioral underwriting. Traditionally, decentralized finance required borrowers to lock up more collateral than the loan value, often exceeding 150%, to mitigate the risk of smart contract failure or market volatility. This model prioritized capital preservation over capital efficiency. By analyzing historical on-chain behavior—such as consistent staking participation, governance voting, and prior loan repayment records—protocols can now assign a credit score that reflects a user’s reliability rather than their current asset holdings.

This shift enables under-collateralized lending, where the required collateral ratio is determined by the borrower’s score rather than a fixed protocol standard. For instance, a borrower with a high on-chain credit score may secure a loan with only 110% collateralization, significantly reducing the capital lock-up compared to the standard 150-200% required by legacy platforms. This mechanism mirrors traditional credit lines, allowing users to access liquidity without selling their underlying crypto assets, thereby preserving their long-term investment positions and avoiding taxable events associated with liquidation.

The practical application of these scores relies on transparent, immutable data points. Protocols analyze transaction history, duration of asset holding, and interaction frequency with other DeFi services to build a comprehensive reputation profile. This data-driven approach reduces the reliance on subjective metrics or external credit bureaus, which are often inaccessible to crypto-native users. As a result, borrowers with strong on-chain histories can negotiate better terms, including lower interest rates and higher borrowing limits, creating a more efficient capital market within the decentralized ecosystem.

While the potential for increased capital efficiency is significant, the implementation of on-chain credit scores introduces new complexities in risk assessment. Protocols must ensure that their scoring algorithms accurately reflect long-term reliability and are not easily manipulated by short-term gaming of the system. As these models mature, they are likely to become a standard feature of DeFi lending platforms, further blurring the lines between traditional finance and decentralized credit markets.

Regulatory hurdles and data privacy

The architecture of on-chain reputation faces a fundamental conflict: blockchains are designed for permanence and transparency, while modern privacy laws like the GDPR and CCPA mandate the right to be forgotten. This tension creates a significant barrier for crypto-native credit scoring, as storing immutable financial history on a public ledger can violate data protection regulations. Unlike traditional credit bureaus that operate within closed, compliant databases, decentralized protocols expose transaction histories to anyone, raising serious concerns about user consent and data erasure.

To navigate this legal landscape, established financial institutions are developing hybrid models that bridge off-chain compliance with on-chain utility. TransUnion, a major credit reporting agency, has begun integrating traditional credit scores into blockchain-based lending protocols. This approach allows lenders to assess risk using established, privacy-compliant data without exposing raw transactional history on the public ledger. By keeping sensitive personal data off-chain while utilizing blockchain for verification and execution, these systems attempt to satisfy both regulatory requirements and the transparency needs of decentralized finance.

The shift toward hybrid models signals a maturation of the market. Rather than forcing users to choose between privacy and access to capital, these frameworks allow financial institutions to verify identity and creditworthiness without compromising the core principles of blockchain security. As regulations tighten, the ability to separate identity verification from transactional visibility will likely determine which platforms can operate at scale.

What to expect from Web3 financial identity

On-chain credit is evolving from experimental wallet reputation into structured financial infrastructure. As Galaxy’s market analysis indicates, institutional adoption is shifting toward prime lending frameworks that treat on-chain behavior as verifiable collateral rather than abstract trust signals. This transition moves credit scoring away from the traditional FICO model toward dynamic, activity-based assessment.

The integration of these scores with broader Web3 identity systems will likely prioritize cross-chain interoperability. Instead of isolated silos, reputation data will flow across protocols, allowing users to leverage their transaction history and asset holdings across different networks. This structural change reduces friction for DeFi users who previously had to build separate credit profiles for each platform.

Traditional finance integration will follow a similar path, focusing on regulatory compliance and risk management. We expect to see more hybrid models where on-chain reputation supplements off-chain credit checks, particularly for underbanked populations. The result is not a replacement of traditional credit but a parallel system that rewards consistent on-chain behavior with tangible financial access.

No comments yet. Be the first to share your thoughts!