In the fast-evolving world of decentralized finance (DeFi), access to credit is being reimagined for a new era. Traditionally, lending in DeFi has required borrowers to lock up more collateral than the amount they wish to borrow, which restricts capital efficiency and excludes those without significant crypto holdings. The root of this overcollateralization lies in the challenge of assessing creditworthiness in a pseudonymous ecosystem. However, the rise of on-chain credit scores is rapidly changing that landscape, paving the way for undercollateralized lending that could unlock trillions of dollars in value.

Why Overcollateralization Dominates DeFi Lending

Unlike traditional finance, where credit bureaus evaluate a borrower’s history and financial behavior, DeFi protocols operate in an environment where users are identified by wallet addresses, not personal identities. This anonymity has made it difficult for protocols to gauge risk, so they require loans to be overcollateralized, often by 150% or more, to protect lenders from default. While this approach minimizes risk for lenders, it creates barriers for borrowers and limits DeFi’s potential as a truly inclusive financial system.

Yet, the demand for capital-efficient lending is surging. The current market reflects this momentum: as of today, Aave (AAVE) trades at $231.92, up $11.94 ( and 0.0543%) in the last 24 hours, a testament to growing activity and confidence in DeFi lending platforms. Still, for DeFi to rival traditional credit markets, it must move beyond collateral-heavy models.

What Are On-Chain Credit Scores?

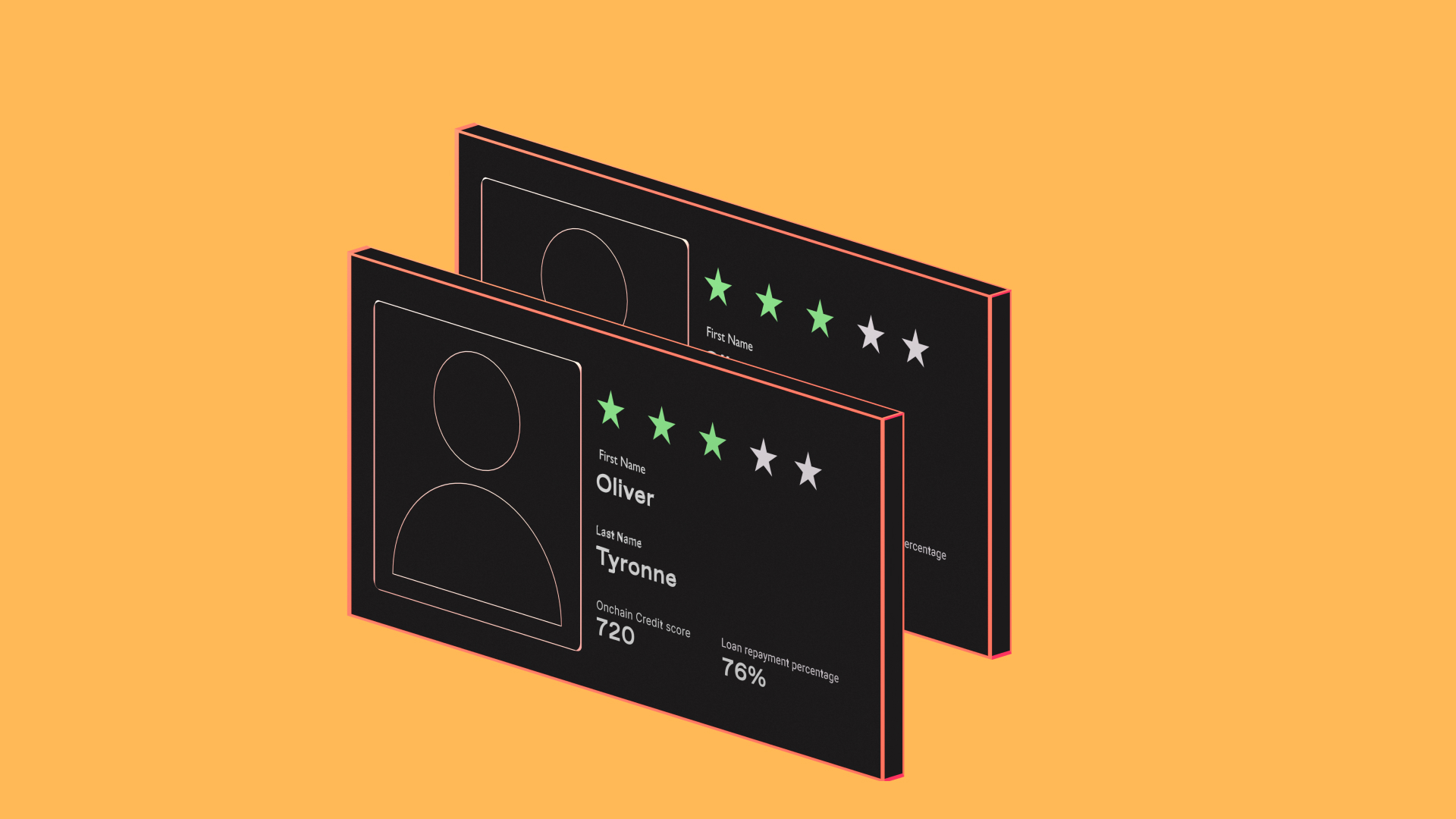

On-chain credit scores are blockchain-native risk assessments that analyze a user’s on-chain behavior, such as loan repayments, transaction history, and interactions with smart contracts, to generate a quantifiable credit reputation. Unlike traditional credit scores, which are tied to personal identities and centralized databases, on-chain scores are linked to wallet addresses, preserving user privacy while enabling transparent risk evaluation.

These scores use advanced analytics and machine learning to process vast amounts of decentralized data, offering real-time insights into a borrower’s reliability. By leveraging this technology, DeFi platforms can confidently offer undercollateralized loans to users with strong on-chain reputations, a breakthrough that stands to democratize access to credit across the globe.

Leading Platforms Driving Undercollateralized Lending

Several innovative protocols are at the forefront of integrating on-chain credit scores into their lending models:

- Cred Protocol: Builds decentralized credit scores by analyzing on-chain lending behaviors, facilitating undercollateralized loans through robust risk quantification.

- Spectral: Introduces the MACRO score, ranging from 300 to 850 and encapsulated in unique Non-Fungible Credits (NFCs): to bring FICO-like scoring to Web3.

- Credora and More Protocol: Provides on-chain credit assessments on Flow Blockchain, enabling users to borrow up to 200% of their collateral while enhancing transparency.

- Teller Finance: Collaborates with Chainlink for privacy-preserving oracle technology that allows borrowers to prove their creditworthiness without exposing sensitive data.

These platforms exemplify how blockchain-based risk assessment is reshaping the DeFi landscape. For a deeper dive into the mechanics and real-world impact of these solutions, visit this comprehensive guide on how on-chain credit scores enable undercollateralized lending in DeFi.

How On-Chain Credit Scores Work: The Building Blocks

The process of generating an on-chain credit score involves several key steps:

- Data Collection: Aggregating wallet activities across DeFi protocols, such as repayment history, liquidity provision, and smart contract interactions.

- Credit Scoring Models: Employing algorithms and machine learning to synthesize raw data into actionable risk metrics.

- Privacy-Preserving Techniques: Leveraging cryptographic proofs (like zero-knowledge proofs) so borrowers can prove their eligibility without revealing personal information.

- Lending Integration: Feeding these scores directly into smart contract lending platforms to dynamically adjust terms based on borrower profiles.

This approach not only improves DeFi risk assessment, but also fosters a more open and competitive financial marketplace where users are rewarded for responsible blockchain behavior instead of gatekept by rigid collateral requirements.

As the infrastructure for on-chain credit scores matures, the benefits for both borrowers and lenders are becoming increasingly clear. Borrowers gain access to capital with less upfront collateral, which is especially impactful for users without significant crypto holdings or those in emerging markets. Lenders, meanwhile, can rely on transparent, data-driven risk assessments that reduce the likelihood of default and enable finer control over loan terms. This shift is already visible in the DeFi landscape as protocols experiment with new risk models and real-time reputation scoring.

Unlocking Capital Efficiency and Financial Inclusion

Undercollateralized lending powered by blockchain credit reputation fundamentally changes the game for capital efficiency. Instead of locking up assets well beyond the value of a loan, users with strong on-chain reputations can borrow closer to or even above their posted collateral, sometimes up to 200% as seen with Credora’s integration on Flow Blockchain. For regular users, this means more flexible access to liquidity; for institutions, it opens doors to scalable credit lines and novel financial products.

Perhaps most importantly, this innovation fosters financial inclusion. By eliminating the need for traditional credit histories or bank accounts, on-chain scores provide a pathway for underserved populations to participate in global finance. The result is a more level playing field where trust is algorithmically earned and transparently verified.

Challenges and Considerations Ahead

While the promise of undercollateralized lending in DeFi is immense, several hurdles must be overcome. Accuracy and security of credit scoring models are paramount; any flaws could expose protocols to increased default risk or manipulation. Privacy must also remain central, protocols like Teller Finance are pioneering privacy-preserving technologies to ensure sensitive details stay protected while still enabling robust risk evaluation.

Another challenge lies in cross-protocol interoperability: as users interact across multiple blockchains and platforms, aggregating a holistic view of their behavior becomes complex. Standards for decentralized identity and attestations are evolving rapidly but will require broad adoption before seamless multi-chain credit scoring becomes reality.

The Road Ahead: Trillions at Stake

The market potential is staggering. Industry leaders estimate that effective decentralized credit bureaus could unlock trillions of dollars in untapped value within DeFi by bringing uncollateralized lending mainstream. As protocols refine their approaches and expand integrations, expect competition, and innovation, to accelerate.

If you’re interested in how these systems are being implemented today (and what’s next), check out our deep dive into the rise of undercollateralized loans in DeFi.

Practical Steps: Building Your On-Chain Credit Reputation

If you want to benefit from emerging undercollateralized lending opportunities, start by building a positive blockchain footprint:

This might include repaying loans promptly, providing liquidity responsibly, and interacting with reputable protocols, all activity that can be tracked by decentralized scoring engines.

The Future Is Transparent, and User-Centric

The evolution from overcollateralization toward data-driven undercollateralized lending marks a turning point for DeFi’s maturity. With platforms like Aave trading at $231.92, momentum is clearly building around smart contract lending and risk-based pricing models. As more users embrace this shift, and as privacy technology keeps pace, the vision of an open, inclusive financial system powered by blockchain analytics moves closer to reality.