Decentralized finance (DeFi) has already reimagined how we borrow and lend, removing the banks and opening up a world where anyone can be a lender or a borrower. But there’s been one persistent catch: trust. How do you know if an anonymous wallet address is reliable? Traditionally, DeFi lending protocols have solved this using overcollateralization, which means borrowers must lock up more crypto than they wish to borrow. While this keeps lenders safe, it restricts capital efficiency and excludes many would-be borrowers from participating.

Why Trustless Lending Needs Decentralized Credit Scores

The next evolution in DeFi is all about trustless lending without excessive collateral. Enter decentralized credit scoring: a new breed of on-chain reputation systems that analyze blockchain activity to assess borrower risk. Instead of relying on paperwork or centralized bureaus, these systems use transparent, immutable data from users’ wallet histories and protocol interactions.

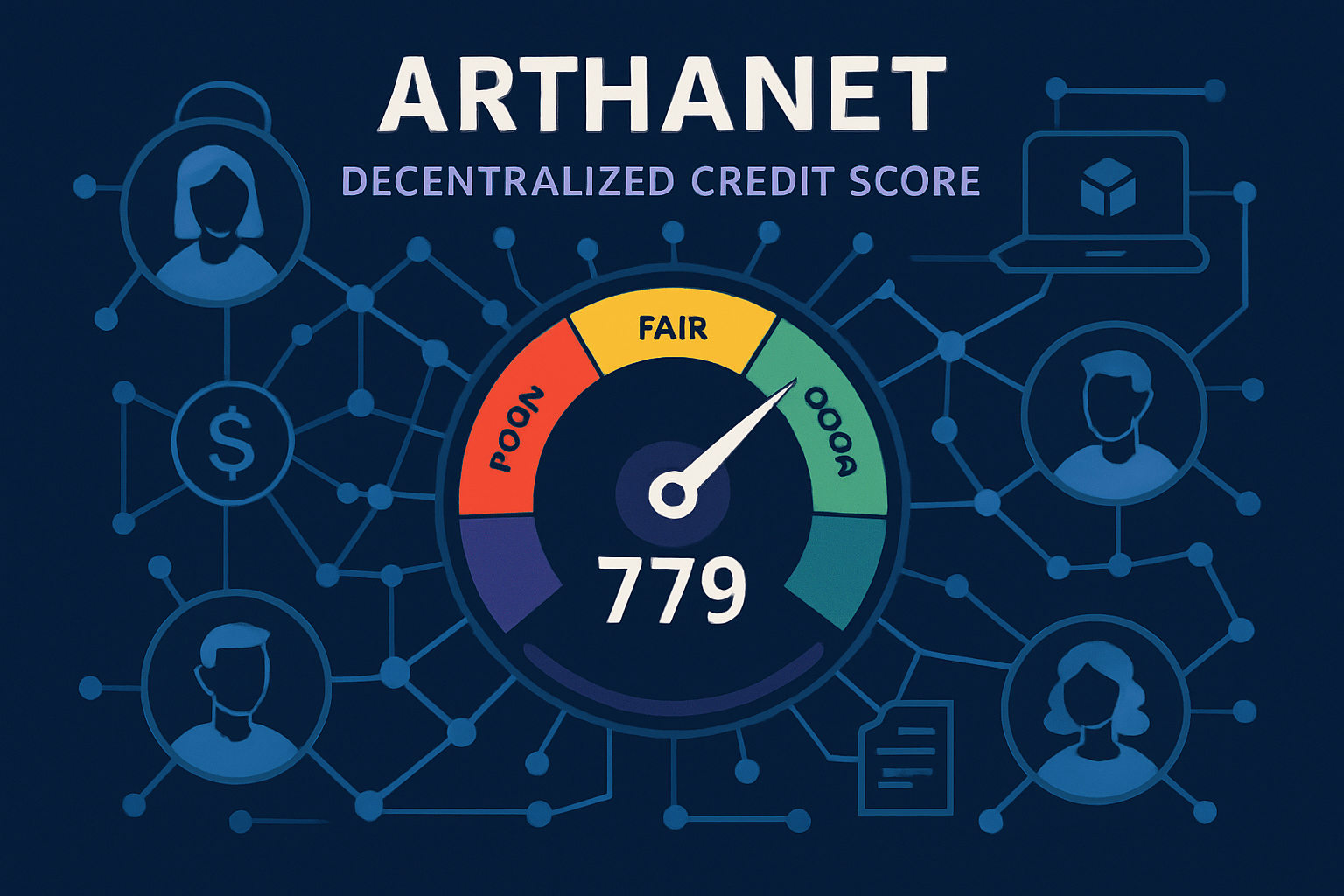

This shift is not just theoretical. Platforms like ArthaNet are using machine learning to generate real-time credit scores from users’ on-chain behavior, making it possible for protocols to offer personalized loan terms. AJEndless AI takes it further by blending artificial intelligence with blockchain transparency, evaluating everything from token swaps to staking patterns for a nuanced view of borrower reliability.

How On-Chain Credit Scores Work

At their core, decentralized credit scores tap into the open nature of blockchains. They analyze:

- Lending and borrowing history: Have you repaid previous loans?

- Wallet age and transaction consistency: Are you an established user or new address?

- Diversity of protocol interactions: Do you use multiple platforms responsibly?

- Network reputation signals: Are there endorsements or negative flags tied to your address?

The result is a dynamic score that can travel with your wallet across protocols, no paperwork required. For example, Cred Protocol aggregates data from over 30 lending platforms across eight blockchains, giving lenders a panoramic view of user trustworthiness.

This innovation paves the way for under-collateralized loans in crypto, where your borrowing power is determined by your digital reputation rather than just your wallet balance.

The Power of Integration: Real-Time Risk Assessment in Action

The real magic happens when these decentralized credit scores plug directly into DeFi apps. Take Gora’s collaboration with RociFi: by incorporating RociFi’s Web3 credit data into Gora’s oracle services, lending protocols can instantly assess a borrower’s risk profile before issuing a loan. This means smarter capital allocation for lenders and better rates for trustworthy borrowers, all without sacrificing privacy or decentralization.

TrueFi goes even further by blending on-chain analytics with select off-chain data points (think business records or social signals), enabling fully uncollateralized lending based purely on reputation. As more protocols embrace these models, the days of locking away excess crypto just to access liquidity could soon be behind us.

This paradigm shift is already having ripple effects across the DeFi landscape. By unlocking under-collateralized and even uncollateralized lending, decentralized credit scoring mechanisms are making capital more accessible and efficient. Lenders can confidently offer loans to a broader pool of users, while borrowers with strong on-chain reputations are rewarded with better rates and higher borrowing limits.

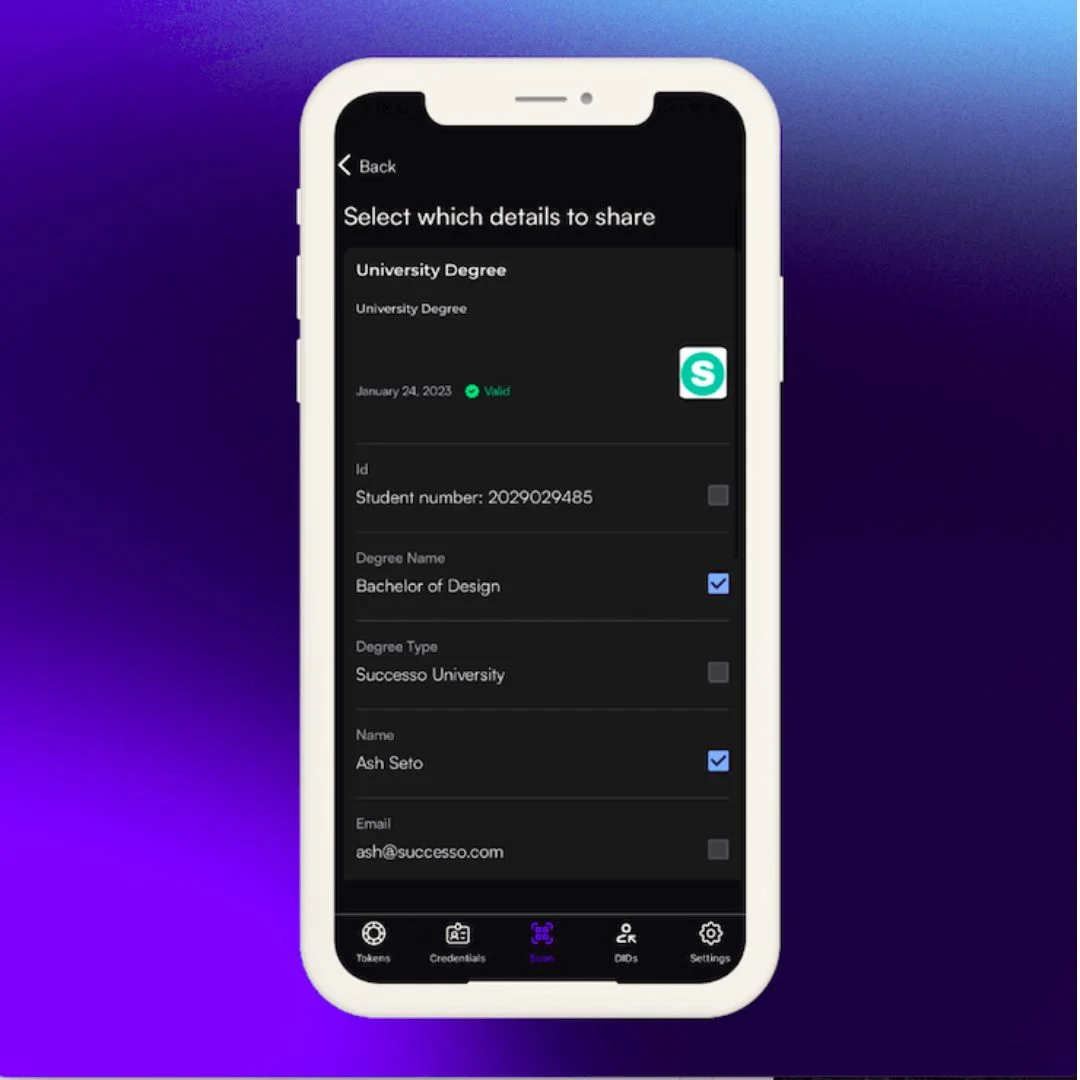

What’s truly game-changing is how these systems preserve privacy. Zero-knowledge proofs and privacy-preserving cryptography allow users to prove their creditworthiness without exposing sensitive details. Your wallet can carry its reputation score everywhere in the Web3 world, no need to hand over your identity or financial history to a centralized authority.

“On-chain reputation is quickly becoming the backbone of trust in DeFi lending. It’s not just about what you own, but how you participate in the ecosystem. ”

Expanding Access and Inclusion

Decentralized credit scoring isn’t just a technical upgrade, it’s a catalyst for financial inclusion. In traditional finance, millions are excluded from credit markets due to lack of documentation or rigid scoring models. In contrast, on-chain reputation is open to anyone who participates in DeFi, regardless of geography or background.

This opens up new opportunities for small businesses, freelancers, and users in emerging markets who have historically been underserved by banks. As stablecoins and smart contract lending protocols proliferate globally, we’re seeing the foundations laid for a more inclusive financial system, one built on transparency, merit, and programmable trust.

Top Benefits of Decentralized Credit Scores in DeFi

- Boosts Financial Inclusion: By leveraging on-chain data, protocols such as Cred Protocol allow users without traditional credit histories to build trust and access global lending markets.

- Enhances Transparency & Trust: Platforms like ArthaNet use blockchain’s immutable records and machine learning to create transparent, tamper-proof credit scores, fostering trust in trustless environments.

- Enables Real-Time Risk Assessment: With AI-powered solutions like AJEndless AI, DeFi protocols can instantly evaluate borrower risk, leading to smarter, faster lending decisions.

- Protects User Privacy: Many decentralized credit systems integrate zero-knowledge proofs and privacy-preserving tech, so users can prove creditworthiness without exposing sensitive personal data.

Challenges Ahead, and Why They Matter

No innovation comes without hurdles. Decentralized credit scoring systems must continually address challenges like data manipulation (Sybil attacks), evolving privacy standards, and cross-protocol interoperability. The arms race between transparency and privacy will shape how these systems mature.

But as protocols collaborate on open standards and leverage advances in AI-driven analytics and privacy tech, the ecosystem grows stronger. Initiatives like Cred Protocol’s cross-chain API or RociFi’s integration with oracle networks point toward a future where your Web3 credit score is as portable as your wallet, and just as secure.

What Comes Next?

The rise of decentralized credit scoring marks a turning point for DeFi lending. As these systems mature, expect to see:

- More capital-efficient lending: Less collateral locked up means more liquidity circulating across protocols.

- Diversification of risk models: Lenders can tailor offers based on granular borrower profiles rather than one-size-fits-all rules.

- A flourishing secondary market: Reputation-backed loans could be bundled into new financial products or traded across platforms.

- Greater user empowerment: Your on-chain activity becomes an asset that unlocks opportunity, not a barrier to entry.

If you’re ready to dive deeper into how decentralized credit scores are transforming risk management and opening new doors for borrowers and lenders alike, check out our guide: How On-Chain Credit Scores Are Transforming DeFi Lending Beyond Overcollateralization.

No comments yet. Be the first to share your thoughts!