Decentralized finance (DeFi) has unlocked powerful new ways for users to borrow and lend assets without traditional banks, but its earliest lending protocols have relied almost exclusively on overcollateralization. This means borrowers must lock up more value than they wish to borrow, limiting both capital efficiency and participation from users who lack substantial crypto holdings. As DeFi matures, on-chain credit scores are emerging as a transformative solution, allowing protocols to move beyond these constraints and usher in an era of undercollateralized lending.

Why Overcollateralization Has Held DeFi Back

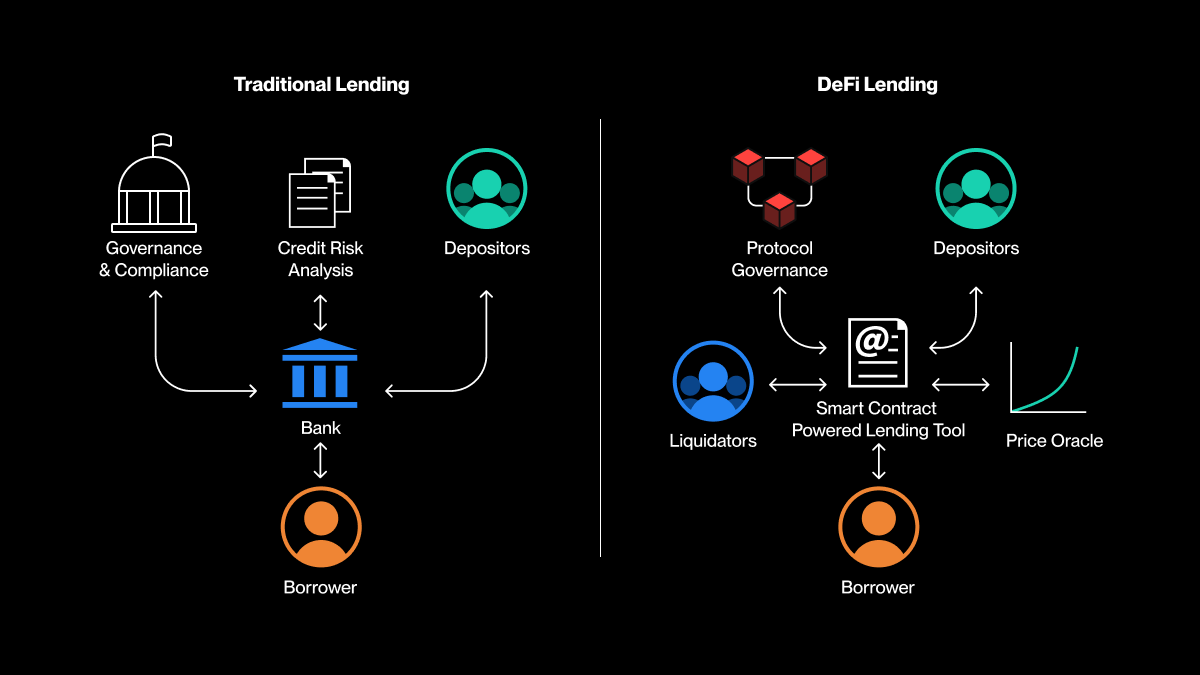

The original ethos of DeFi was permissionless access. Yet, requiring users to deposit $1.50 or even $2.00 worth of ETH or stablecoins just to borrow $1 undermines that vision. While this model protects lenders against defaults in a trustless environment, it also means:

- Capital Inefficiency: A large portion of user assets sits idle as collateral rather than circulating productively in the ecosystem.

- Exclusion: Many would-be borrowers are locked out if they cannot post sufficient collateral, despite being creditworthy by other measures.

- Lack of Credit History Utilization: Traditional finance rewards responsible borrowers with better terms; classic DeFi ignores this dimension entirely.

This is why the industry is now looking toward decentralized credit assessment tools that can measure blockchain reputation and risk more dynamically.

The Rise of On-Chain Credit Scoring

On-chain credit scores analyze users’ blockchain activity - their transaction history, wallet balances, repayment patterns, and interactions with smart contracts - to generate a real-time profile of financial behavior. Unlike opaque centralized bureaus, these scores are built from transparent and immutable data recorded directly on public blockchains. The result? A decentralized alternative to FICO-style scoring that can unlock new forms of lending.

The implications for DeFi are profound:

- Undercollateralized Loans Become Possible: Borrowers with robust on-chain reputations can access loans with lower collateral requirements or even none at all. This dramatically improves capital utilization across protocols.

- Lenders Get Smarter Risk Tools: Platforms can tailor loan terms - interest rates, loan-to-value ratios - based on individualized risk profiles rather than one-size-fits-all rules.

- Financial Inclusion Expands: Users who previously couldn’t participate due to lack of upfront assets but who demonstrate positive financial behaviors gain access to new opportunities.

If you want a deeper dive into how these systems work under the hood and their impact on capital efficiency, you’ll find a thorough breakdown here: How On-Chain Credit Scores Enable Undercollateralized Lending in DeFi.

Pioneering Protocols: Who’s Leading the Charge?

A wave of innovative projects is building out infrastructure for decentralized credit assessment and undercollateralized loans:

- Credora: Facilitated over $1.5 billion in crypto loans by providing transparent on-chain credit assessments for both individuals and institutions.

- Spectral: Their Multi-Asset Credit Risk Oracle (MACRO) delivers FICO-like scores (300-850 range) based entirely on wallet activity and protocol interactions.

- SolCred: Combines real-time Solana blockchain data with machine learning models to create comprehensive borrower profiles for more efficient lending markets.

This surge in development is not just theoretical; real-world volumes are growing as protocols adopt these tools to offer new products outside the rigid boundaries of overcollateralization. For a technical exploration into how risk scoring works across platforms, see our resource: How On-Chain Credit Scores Improve Risk Assessment for DeFi Lending Platforms.

But the road to fully decentralized, credit-based lending is not without its hurdles. As the ecosystem matures, protocols and users must navigate several critical challenges to ensure these systems remain robust, fair, and truly decentralized.

Key Challenges for On-Chain Credit Scoring

Data privacy sits at the heart of the debate. On-chain activity is inherently transparent, but users deserve control over how their financial behaviors are analyzed and shared. Emerging solutions like zero-knowledge proofs allow credit scores to be calculated without revealing sensitive wallet details, striking a balance between transparency and privacy. Leading protocols are racing to implement these cryptographic safeguards as user adoption grows.

Standardization is another pressing issue. With a proliferation of credit scoring platforms, each with its own methodology, borrowers may find their scores inconsistent across different DeFi protocols. The lack of interoperability can fragment user experiences and limit the network effects that make decentralized finance so powerful. Industry-wide collaboration on open standards will be essential for seamless lending markets that span chains and platforms.

Sybil resistance, or preventing users from gaming the system by creating multiple wallets, remains a technical challenge unique to blockchain-based identity. Protocols are experimenting with social graph analysis, reputation staking, and multi-factor authentication to ensure credit scores reflect genuine history rather than manufactured activity.

The Road Ahead: What Widespread Adoption Could Unlock

If these obstacles can be overcome, on-chain credit scoring could unlock trillions in new value for DeFi. Under-collateralized lending would become accessible not just for crypto whales but for everyday users building their blockchain reputations over time. Capital would flow more efficiently across protocols, fueling innovation in everything from merchant finance to real-world asset tokenization.

The ripple effects extend beyond DeFi itself. As blockchain-based credit histories become portable across Web3 applications, from NFT marketplaces to DAOs, the concept of self-sovereign financial reputation will take root. Users will finally own their data and leverage it wherever opportunity arises.

This is not just theory: projects like Credora and Spectral are already demonstrating how decentralized risk assessment can power real-world lending at scale. For an actionable guide on how you can start building your own on-chain reputation or tap into undercollateralized loans today, see our primer: How On-Chain Credit Scores Empower DeFi Users to Access Uncollateralized Loans.

The future of DeFi lending will be shaped by those who master the art of decentralized trust, balancing transparency with privacy, efficiency with security, inclusion with integrity. By embracing on-chain credit scores as a foundation for risk assessment and access, we move closer to a world where financial opportunity is limited only by your actions, not your starting balance.

No comments yet. Be the first to share your thoughts!