Decentralized finance (DeFi) lending platforms are rapidly evolving, but their risk assessment tools have long lagged behind traditional finance. Historically, DeFi lending has relied on heavy over-collateralization, a blunt instrument that limits capital efficiency and excludes many would-be borrowers. The emergence of on-chain credit scores is set to change this paradigm entirely by introducing real-time, transparent, and data-driven risk assessments that leverage the full transparency of blockchain activity.

Why Traditional DeFi Risk Assessment Falls Short

Most DeFi protocols to date have managed risk by requiring borrowers to lock up assets worth far more than the loan amount. This approach is simple but inefficient. It fails to account for individual borrower behavior or creditworthiness and instead assumes all users present equal risk. As a result, capital sits idle and access to credit is restricted mainly to those with substantial crypto holdings.

The lack of nuanced risk assessment also exposes lenders to sudden market shocks and makes it challenging for protocols to attract institutional capital. Without a way to differentiate between high- and low-risk borrowers based on actual behavior, DeFi platforms remain vulnerable to both systemic and idiosyncratic risks.

The Rise of On-Chain Credit Scores: A New Era for DeFi Lending

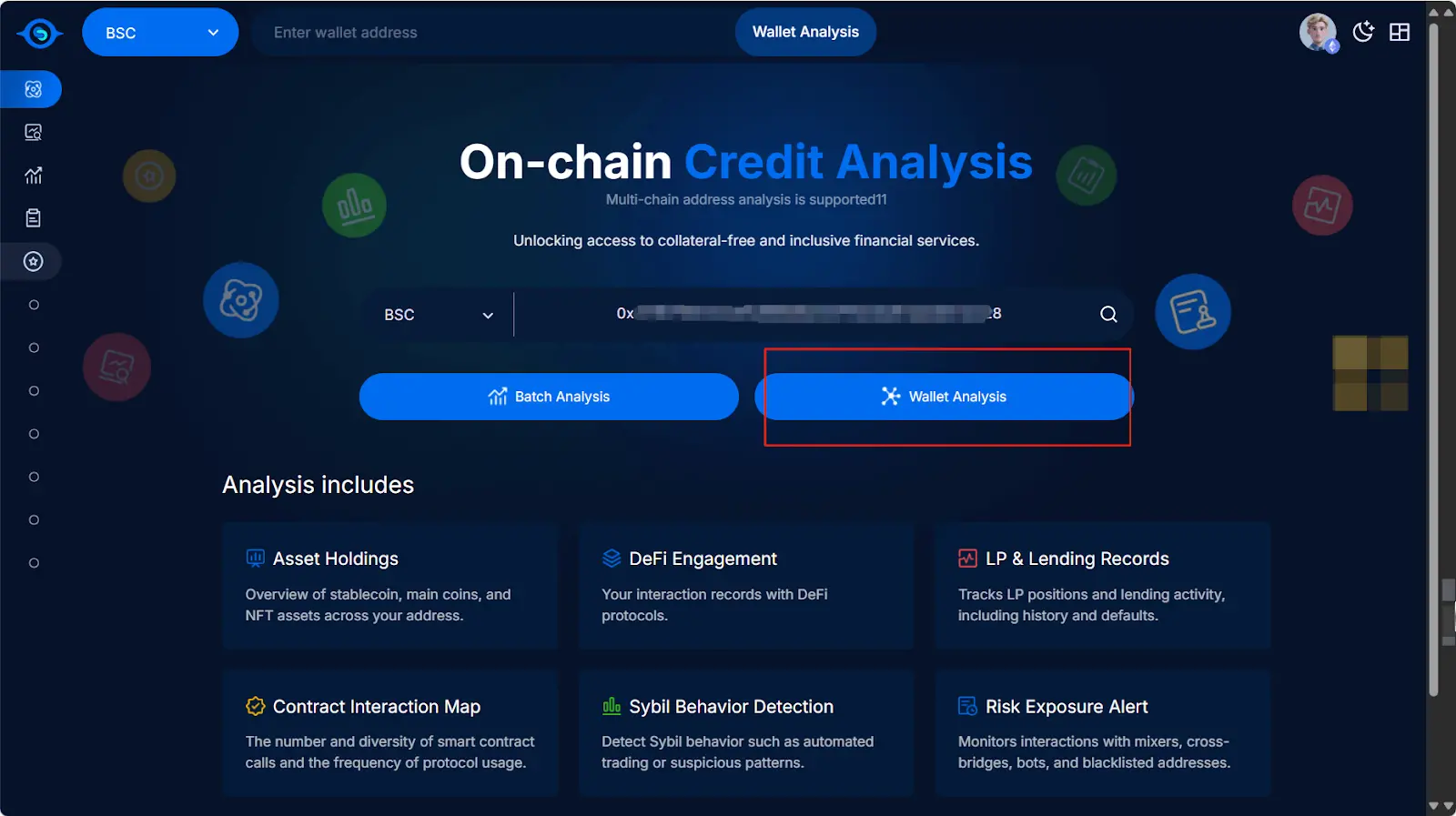

On-chain credit scores are transforming how risk is evaluated in decentralized markets. These scores analyze blockchain-native data such as wallet transaction history, repayment records, interaction with smart contracts, and even participation in governance or liquidity pools. By building a dynamic profile of each user’s financial behavior, these systems enable protocols to assess risk far more precisely than with static collateral ratios alone.

The integration of on-chain credit scores into DeFi lending protocols means loan terms can be tailored in real time: lower interest rates or higher loan-to-value (LTV) ratios for trustworthy borrowers, stricter terms for those deemed higher risk. This not only reduces default rates but also unlocks new opportunities for under-collateralized or even uncollateralized lending, long considered the holy grail for crypto credit markets.

Real-Time Transparency and Automated Risk Management

A key advantage of blockchain-based scoring is continuous monitoring. Unlike legacy systems that rely on periodic updates or opaque reporting, on-chain assessments are always current. A borrower’s score can change instantly as new transactions occur or as their exposure across protocols shifts.

This real-time transparency supports automated adjustments via smart contracts, interest rates can rise if a borrower’s score drops; collateral requirements can be eased when positive behavior is detected. Protocols like Credora are already providing consensus-based ratings accessible directly on-chain, mapping these new metrics to familiar scales from traditional credit agencies for easier adoption by institutional players.

For an in-depth look at how these innovations power safer lending environments while improving capital allocation efficiency, see our guide here.

With this infrastructure in place, DeFi lending platforms are beginning to realize the potential for more sophisticated risk management. Smart contracts can now programmatically adjust loan terms in response to changes in a borrower’s on-chain credit score, minimizing manual intervention and operational risk. This not only streamlines protocol operations but also allows for a more responsive and resilient lending environment, one that adapts to evolving market conditions and user behavior.

Unlocking Under-Collateralized Lending

Perhaps the most transformative impact of on-chain credit scoring is its ability to unlock under-collateralized and even unsecured lending within DeFi. By providing granular, real-time credit profiles, protocols can confidently extend credit beyond the rigid boundaries of over-collateralization. This shift mirrors developments in traditional finance but with added transparency and automation unique to blockchain systems.

Platforms leveraging AI-powered risk analytics, such as those highlighted by Bitdeal, are already using wallet behavior and repayment history to build trust scores that support nuanced lending decisions. As a result, borrowers with robust on-chain reputations can access better terms, while lenders benefit from improved risk-adjusted yields and reduced default rates. The ecosystem moves closer to capital allocation efficiency reminiscent of mature financial markets, but with the added speed and openness of Web3.

Bridging Institutional Trust Gaps

The integration of on-chain credit scores is also closing the trust gap between decentralized protocols and institutional investors. Collaborations like S and amp;P Global Ratings’ Stablecoin Stability Assessments published on-chain exemplify how familiar frameworks from legacy finance are being adapted for the crypto-native world. These developments enable funds, DAOs, and treasuries to allocate capital more confidently, leveraging real-time risk metrics rather than static or subjective assessments.

This convergence is further supported by decentralized credit bureaus that synthesize both blockchain data and traditional financial indicators into composite scores. The result: a unified risk index that incorporates creditworthiness, liquidity exposure, governance participation, and more, providing a holistic view of protocol- and wallet-level risks.

What’s Next for DeFi Credit Risk Assessment?

The evolution of blockchain credit scoring is far from finished. As data sources expand and machine learning models become more sophisticated, expect even richer borrower profiles that account for everything from cross-chain activity to social reputation signals within Web3 communities. The next generation of decentralized lending will likely feature interoperable scoring standards adopted across protocols, enabling seamless reputation portability as users move between platforms.

For those looking to explore how these advances enable safer under-collateralized lending, and why they matter for both lenders and borrowers, consider our deeper dive at this resource.

The upshot? On-chain credit scores represent more than just an incremental improvement, they signal a structural shift in how risk is managed throughout decentralized finance. By combining transparency, automation, and data-driven insights, these tools empower both users and protocols to participate in a fairer, safer financial system where yield is truly earned, not simply assumed.

No comments yet. Be the first to share your thoughts!