Decentralized finance (DeFi) has unlocked a world of permissionless lending and borrowing, but risk management remains a persistent challenge. Traditionally, DeFi protocols have relied on over-collateralization to protect lenders, often requiring borrowers to lock up assets worth far more than their loan. This approach, while effective at limiting defaults, restricts capital efficiency and excludes many would-be borrowers. Enter on-chain credit scores: a breakthrough in blockchain credit assessment that is rapidly reshaping how DeFi platforms evaluate risk, set loan terms, and expand access to credit.

Why DeFi Needs Better Risk Management

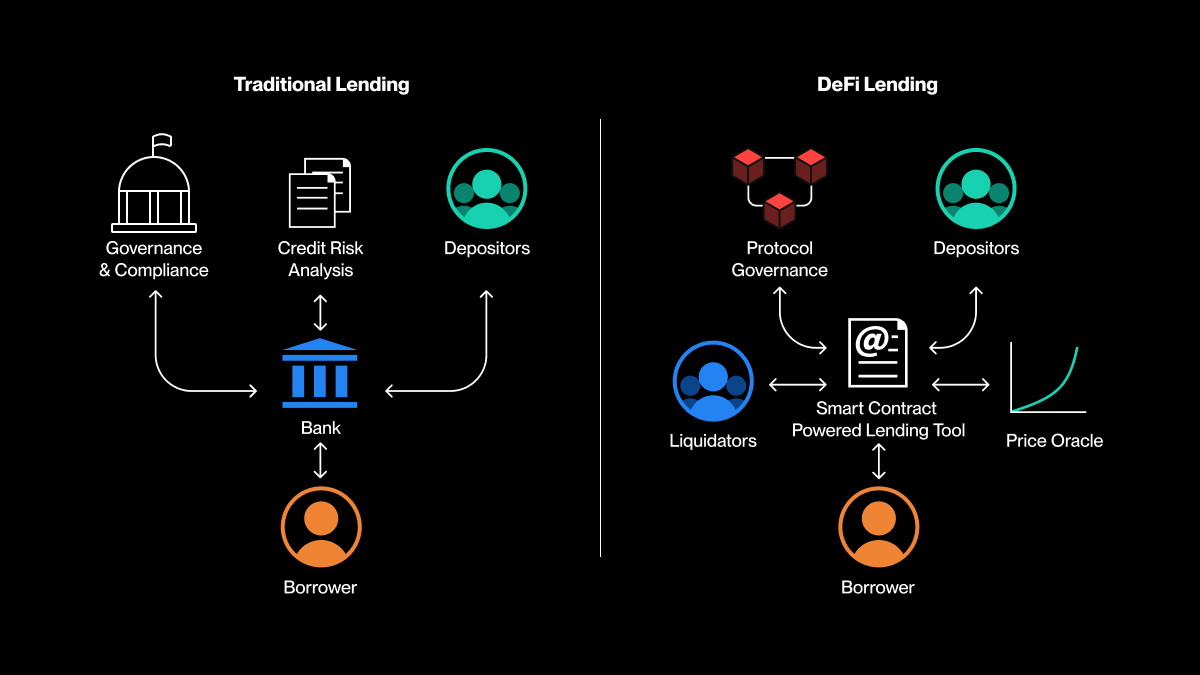

The heart of DeFi lending risk management lies in accurately assessing borrower reliability. Unlike traditional finance, where credit bureaus aggregate years of off-chain financial behavior, DeFi operates in a pseudonymous environment. This makes it difficult for protocols to distinguish between trustworthy borrowers and potential bad actors. The result? Protocols demand high collateral ratios, limiting capital efficiency and stifling innovation.

On-chain credit scores solve this by leveraging transparent, real-time data from the blockchain. These scores analyze wallet activity, transaction history, and protocol interactions to create a holistic risk profile. As a result, lenders can now make more nuanced decisions, offering differentiated rates and terms based on actual borrower behavior rather than blanket rules.

How On-Chain Credit Scores Work

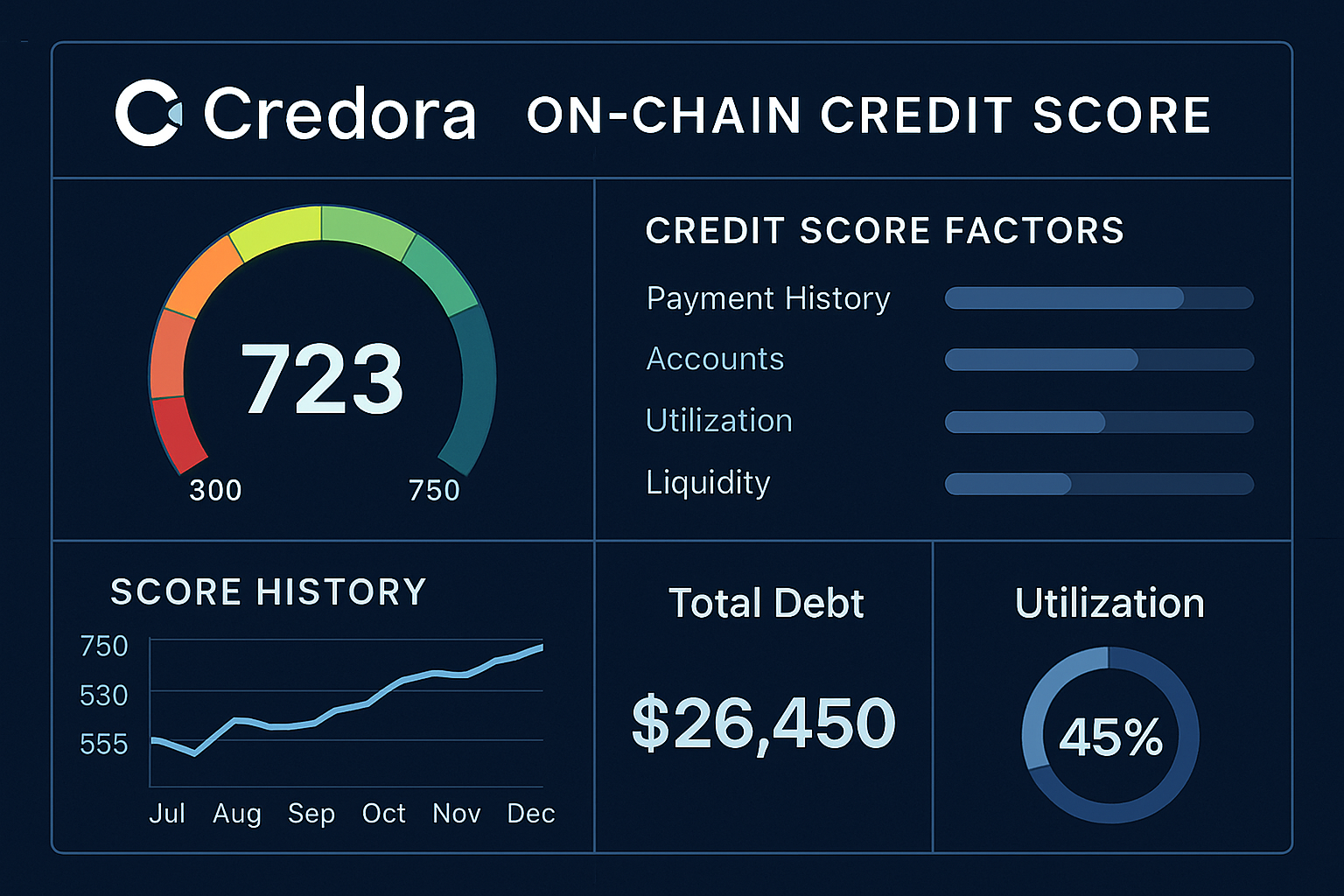

At their core, on-chain credit scores use advanced analytics and, increasingly, artificial intelligence to evaluate risk. By examining a wallet's history, loan repayments, participation in liquidity pools, and even governance activity, algorithms generate a probabilistic risk measure. The On-Chain Credit Risk Score (OCCR Score), for example, quantifies the likelihood of default based on observed blockchain activity (learn more about OCCR Scores).

AI-powered models can sift through vast datasets, identifying subtle patterns that human analysts might miss. This enables protocols to:

Key Benefits of On-Chain Credit Scoring for DeFi Lenders

- Enhanced Transparency and Real-Time Risk Assessment: On-chain credit scores, such as those provided by Credora, offer transparent, blockchain-based evaluations of borrower creditworthiness, enabling lenders to make more informed decisions based on up-to-date data.

- Automated and Dynamic Loan Terms: Integrating on-chain credit scores allows DeFi protocols to programmatically adjust interest rates, loan sizes, and durations in real time, optimizing risk management and operational efficiency.

- Facilitation of Under-Collateralized Lending: By leveraging on-chain credit profiles, platforms like FraxLend can safely offer loans with reduced collateral requirements, improving capital efficiency and expanding credit access.

- AI-Driven Credit Assessment: Solutions such as Creditlink utilize AI to analyze wallet activity and transaction history, generating nuanced credit scores that support more accurate lending decisions.

- Industry Adoption and Trust: Collaborations like Untangled Finance and Moody's Ratings demonstrate growing institutional trust in on-chain credit scoring, paving the way for broader adoption and integration in DeFi markets.

Importantly, this process is transparent and verifiable, anyone can audit the data and logic behind a given score, which builds trust in the system. As more protocols integrate on-chain risk analytics, DeFi lending is shifting toward a model that rewards good behavior and enables fairer, more efficient capital allocation.

Automating Loan Terms with Real-Time Credit Metrics

One of the most exciting outcomes of decentralized credit scoring is the ability to automate loan terms. Smart contracts can now adjust interest rates, collateral requirements, and even loan durations programmatically, based on a borrower's up-to-date credit profile. For example, if a wallet's credit score improves due to timely repayments or increased on-chain activity, the protocol can instantly offer better terms without manual intervention.

This automation not only streamlines operations for DeFi platforms but also enhances borrower experience. Lenders benefit from dynamic risk management, while borrowers gain access to more competitive rates and flexible loan structures. Leading platforms like Credora and Untangled Finance are already piloting these innovations, partnering with rating agencies and leveraging AI to refine their models (see how under-collateralized lending is becoming possible).

Enabling Under-Collateralized Lending and Expanding Access

Perhaps the most transformative impact of on-chain credit scores is their role in enabling under-collateralized lending. By providing a reliable, data-driven measure of borrower risk, DeFi protocols can confidently offer loans with lower collateral requirements. This unlocks capital for users who may not have large crypto holdings but possess strong on-chain reputations. The result is a more inclusive DeFi ecosystem where credit is allocated based on merit, not just wallet size.

Platforms Using On-Chain Credit Scores for DeFi Lending

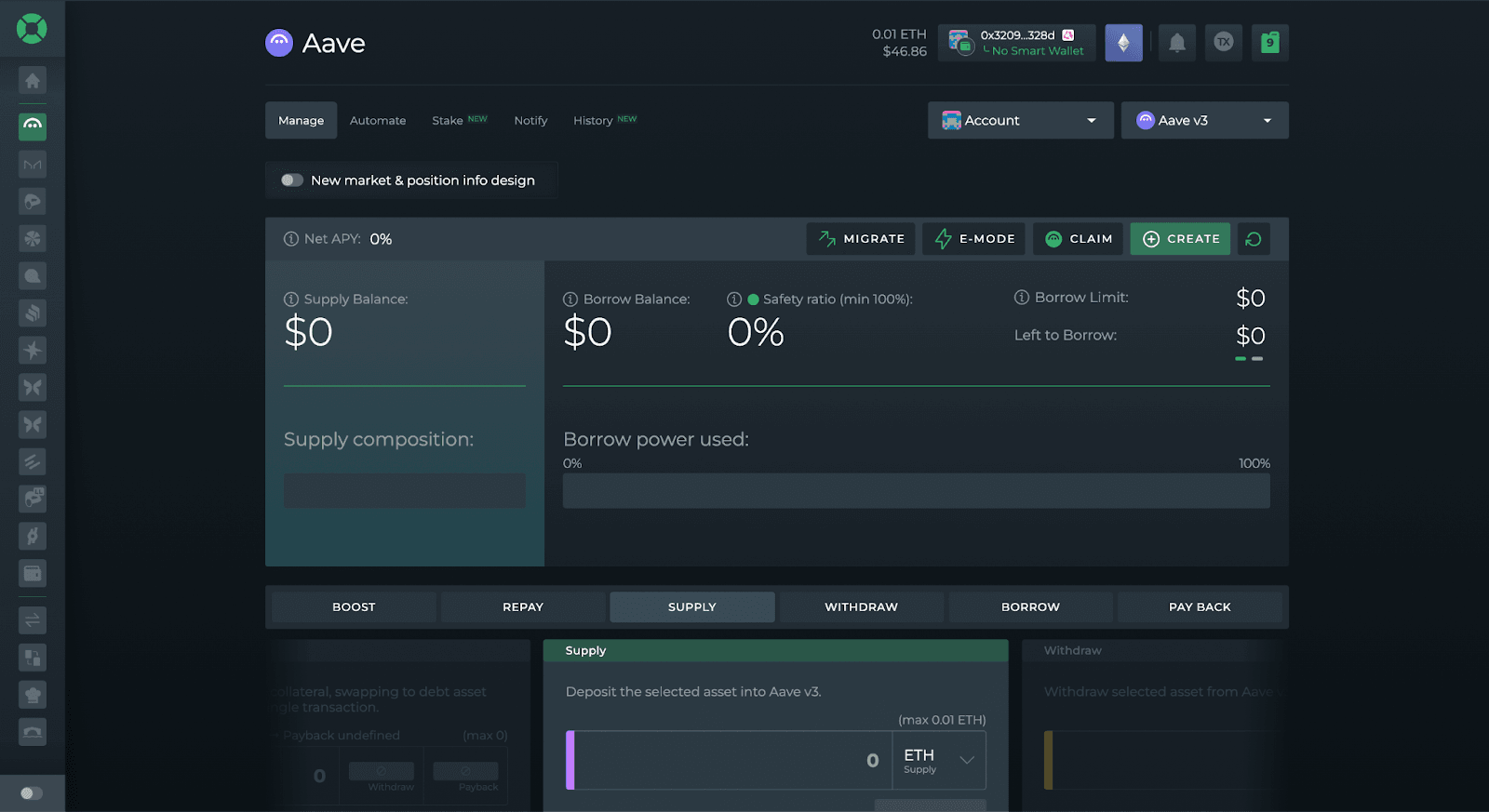

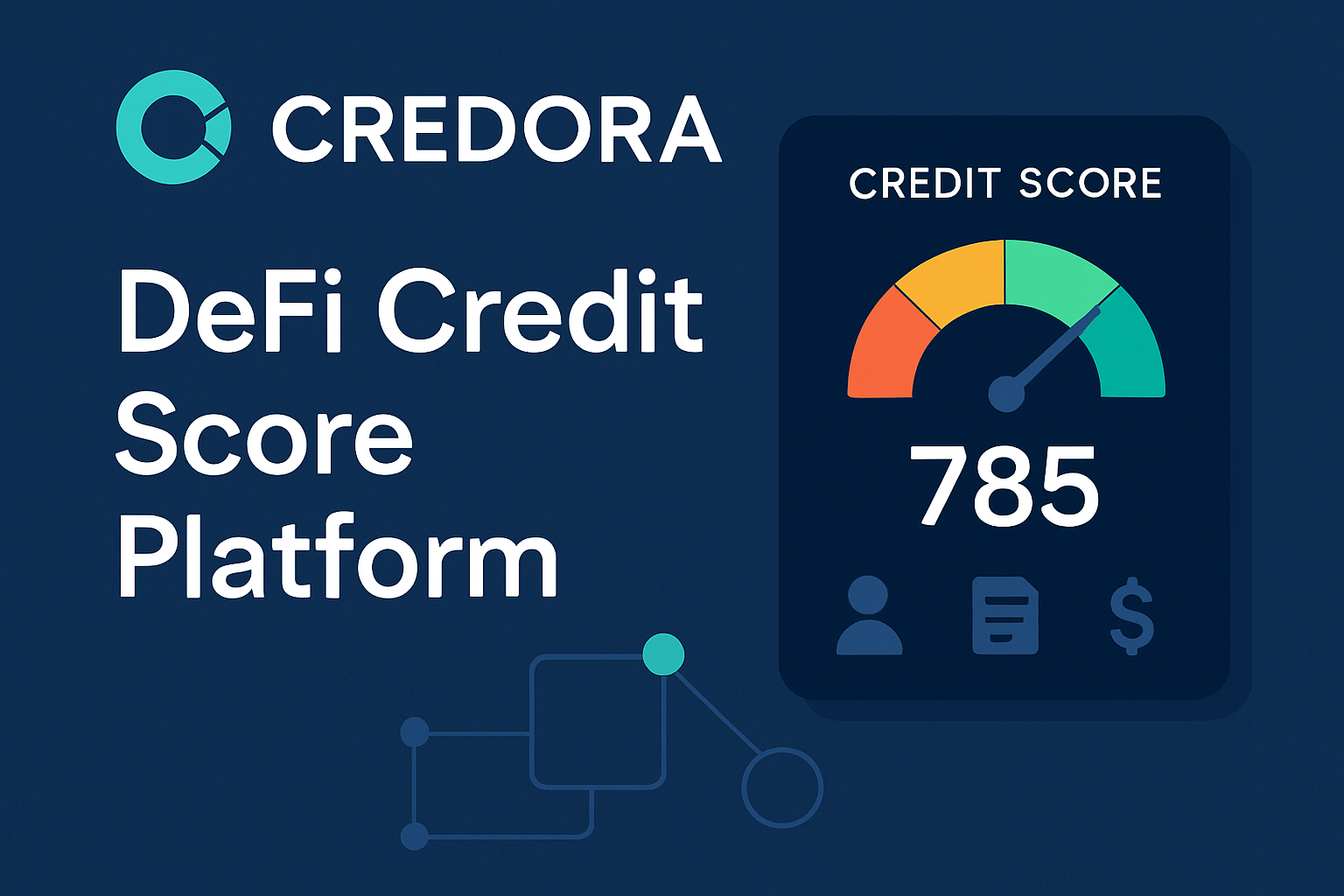

- Credora — Credora brings on-chain credit scores to decentralized lending markets, partnering with platforms like Clearpool and Obligate to enable under-collateralized loans and enhance transparency for both lenders and borrowers.

- Untangled Finance — In collaboration with Moody’s Ratings, Untangled Finance is piloting the integration of traditional credit ratings on-chain, aiming to make risk assessment in DeFi more transparent and efficient.

- Creditlink — Creditlink leverages AI-driven on-chain credit scoring to power Web3 applications, offering services such as Credit Scoring as a Service and Credit NFT Issuance to optimize trust and efficiency within DeFi ecosystems.

- Clearpool — This DeFi lending protocol utilizes on-chain credit assessments (in partnership with Credora) to facilitate under-collateralized institutional lending, improving capital efficiency and risk management.

- Obligate — Obligate integrates on-chain credit scores (via Credora) into its debt issuance platform, enabling programmable risk management and more accessible credit for institutional borrowers.

With AI-driven credit assessment, real-time transparency, and automated loan terms, decentralized credit scoring is rapidly becoming the backbone of modern DeFi lending risk management. As adoption grows, expect to see more efficient markets, reduced default rates, and an expanding pool of borrowers participating in the Web3 economy.

Another critical advantage of on-chain credit scoring is its ability to foster trust and accountability between pseudonymous borrowers and global lenders. Because every action is recorded on the blockchain, both good and bad credit behaviors are visible, creating a transparent track record that cannot be manipulated retroactively. This transparency is a game changer for Web3 lending trust, as it enables protocols to reward responsible participants and penalize risky behavior in real time.

Moreover, the integration of AI-powered analytics into decentralized credit scoring is making risk management more sophisticated than ever. Algorithms can continuously monitor wallet activity across multiple protocols, flagging anomalies or sudden risk spikes before defaults occur. This proactive approach empowers both lenders and protocols to respond swiftly to emerging risks, protecting pooled capital while keeping lending markets fluid.

Real-World Adoption: Moving from Theory to Practice

The movement toward blockchain-based risk assessment is more than theoretical. Real-world implementations are accelerating, with platforms like Credora, Untangled Finance, and Creditlink leading the charge. For example, Credora has brought institutional-grade scoring models on-chain, while Untangled Finance’s collaboration with Moody’s Ratings signals traditional finance’s growing interest in decentralized risk analytics. Creditlink’s Credit NFT Issuance even allows users to prove their creditworthiness across the Web3 ecosystem, optimizing access to new financial products.

This rapid innovation is also driving the creation of unified risk indices that integrate credit, liquidity, and governance factors for a holistic view of protocol health. As more DeFi projects adopt these frameworks, the entire ecosystem benefits from greater stability and investor confidence.

What’s Next for DeFi Lending Risk Management?

The future of DeFi lending lies in decentralized credit scoring that is transparent, automated, and privacy-preserving. As adoption of on-chain credit scores grows, expect to see:

Upcoming Trends in On-Chain Credit Scoring for DeFi

- Automated, Programmatic Loan Terms: DeFi protocols are increasingly using on-chain credit scores to automate loan terms—such as interest rates and collateral requirements—based on real-time borrower data. This trend enhances scalability and risk management by adjusting conditions dynamically. (Credora)

- Expansion of Under-Collateralized Lending: With improved on-chain credit assessments, DeFi platforms like FraxLend are enabling under-collateralized loans, making credit more accessible and capital allocation more efficient. (FraxLend Credit Risk Analytics)

- AI-Powered Credit Scoring: Artificial intelligence is being leveraged to analyze wallet activity and transaction history, producing more accurate and nuanced on-chain credit scores. Platforms like Creditlink are at the forefront of this trend, offering AI-driven credit scoring solutions for Web3 applications. (Creditlink)

- Integration with Traditional Credit Ratings: Partnerships such as Untangled Finance and Moody's Ratings are bringing established credit rating methodologies on-chain, aiming for greater transparency and efficiency in DeFi risk assessment. (Untangled Finance & Moody's)

- Enhanced Transparency and Real-Time Risk Monitoring: Platforms like Credora are setting new standards for transparency by providing real-time, on-chain credit scores that help lenders and investors better evaluate risk-adjusted returns. (Credora)

Protocols will increasingly compete on the quality of their risk analytics, offering borrowers tailored loan products while protecting lenders from systemic shocks. The days of one-size-fits-all collateral requirements are fading; instead, nuanced blockchain credit assessment will drive smarter decisions at every level.

If you’re a developer or protocol operator looking to integrate on-chain credit scoring into your platform, resources like this developer guide can help you get started.

The bottom line? On-chain credit scores are not just improving DeFi lending risk management, they’re setting the stage for a more efficient, inclusive, and resilient decentralized economy.

No comments yet. Be the first to share your thoughts!