In 2024, the landscape of decentralized finance (DeFi) lending underwent a seismic shift. The introduction of on-chain credit scores fundamentally changed how risk is assessed, capital is allocated, and users interact with lending protocols. Gone are the days when DeFi lending was synonymous with overcollateralization and limited access. Today, blockchain-based credit assessments are unlocking a new era of efficiency, transparency, and inclusivity.

Why On-Chain Credit Scores Matter in DeFi Lending

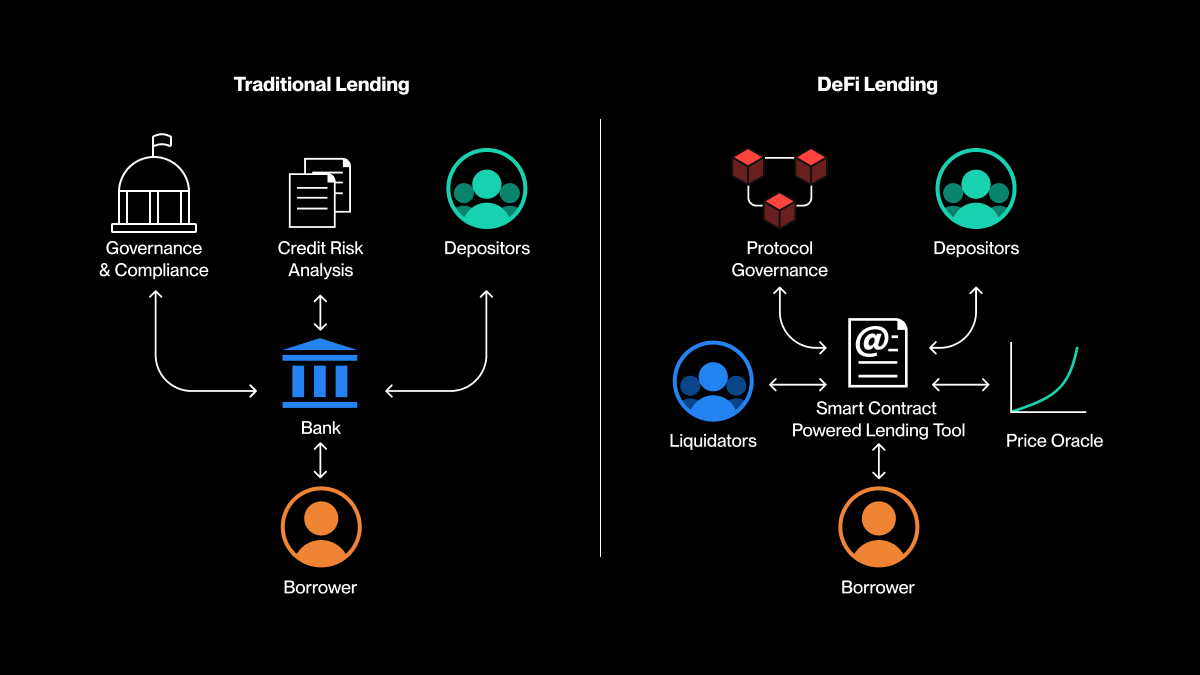

Historically, DeFi platforms like Aave and Compound relied on hefty collateral requirements to protect lenders, often demanding borrowers lock up more crypto than they wished to borrow. This approach, while secure, excluded the unbanked, underbanked, and those without substantial digital assets. Enter on-chain credit scoring: a decentralized, data-driven approach that evaluates a user’s creditworthiness based on their blockchain transaction history, protocol interactions, and repayment patterns. The result? A nuanced risk profile that enables undercollateralized or even uncollateralized loans for reputable borrowers.

Platforms such as Credora and Goldfinch have set the pace, integrating on-chain credit models to offer more competitive loan terms. These protocols now assess risk using transparent, tamper-proof data, allowing them to lower interest rates and collateral requirements for users with strong on-chain reputations. It’s a radical upgrade in the DeFi lending experience, opening the door for millions previously sidelined by traditional models.

How Blockchain Credit Assessment Works

So, how do these blockchain credit assessments actually function? At their core, on-chain credit scores aggregate and analyze a user’s public transaction history. This includes wallet activity, borrowing and repayment records, protocol participation, and even engagement with real-world asset (RWA) tokenization. Algorithms sift through this data to produce a score – a transparent signal of creditworthiness that DeFi platforms can trust.

For example, Credora’s system, launched in July 2024, partners with Clearpool and Obligate to bring credit scores on-chain, boosting transparency and efficiency in the lending market. Meanwhile, Goldfinch leverages both on- and off-chain data to power undercollateralized lending for small businesses in emerging markets. These advances are not just technical upgrades; they’re catalysts for global financial inclusion.

Expanding Access: From Overcollateralized to Reputation-Based Lending

The most profound impact of crypto credit scoring in 2024 is its role in expanding access to capital. By moving beyond the blunt instrument of overcollateralization, DeFi lending platforms can now serve a broader, more diverse user base. Borrowers with strong on-chain reputations gain access to better terms, while lenders benefit from more accurate risk pricing and healthier protocol utilization rates.

This shift is already reflected in the numbers: as of Q4 2024, the outstanding loans through on-chain lending applications jumped 18% above the previous $16.2 billion benchmark. Tokenization of real-world assets further widens the opportunity set, allowing DeFi platforms to bridge the gap between crypto and traditional finance.

Aave (AAVE) Price Prediction 2026-2031

Forecast based on DeFi trends, on-chain credit innovation, and evolving market conditions as of Q4 2025.

| Year | Minimum Price | Average Price | Maximum Price | % Change (Avg, YoY) | Market Scenario Insights |

|---|---|---|---|---|---|

| 2026 | $190.00 | $245.00 | $320.00 | +3.7% | Post-credit-score adoption consolidation; moderate growth as DeFi lending matures. |

| 2027 | $210.00 | $282.00 | $370.00 | +15.1% | Bullish scenario with increased RWA tokenization and mainstream DeFi adoption. |

| 2028 | $230.00 | $325.00 | $420.00 | +15.2% | Potential regulatory clarity boosts institutional participation; volatility remains. |

| 2029 | $250.00 | $360.00 | $470.00 | +10.8% | Sustained growth as on-chain credit scoring becomes standard across DeFi. |

| 2030 | $265.00 | $395.00 | $520.00 | +9.7% | Enhanced interoperability and cross-chain lending drive new user influx. |

| 2031 | $280.00 | $420.00 | $560.00 | +6.3% | Market matures; competition intensifies but Aave retains leadership in DeFi lending. |

Price Prediction Summary

Aave (AAVE) is projected to steadily appreciate through 2031, building on the transformative impact of on-chain credit scoring and the growing integration of real-world assets in DeFi lending. While year-over-year growth rates may moderate as the sector matures, significant upside remains, especially under favorable regulatory and adoption scenarios. Investors should expect both bullish and bearish periods, with price ranges reflecting evolving market dynamics.

Key Factors Affecting Aave Price

- Broader adoption of on-chain credit scoring and undercollateralized lending.

- Tokenization of real-world assets (RWAs) expanding DeFi use cases.

- Potential for regulatory clarity or new compliance requirements impacting DeFi protocols.

- Continued innovation in DeFi protocol security and interoperability.

- Competition from other lending protocols (e.g., Compound, Maker) and traditional finance.

- Overall macroeconomic conditions and crypto market sentiment.

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis.

Actual prices may vary significantly due to market volatility, regulatory changes, and other factors.

Always do your own research before making investment decisions.

Of course, challenges remain. Technical hurdles in aggregating on-chain data, privacy concerns, and the need for standardized scoring methodologies are all front and center. But the momentum is undeniable: on-chain credit scores are powering a more open, efficient, and resilient DeFi ecosystem. For a deep dive into how these systems enable undercollateralized lending, check out this guide.

As on-chain credit scores mature, they’re not just transforming risk models – they’re redefining who gets to participate in the global financial system. For the first time, individuals with limited access to traditional credit are building portable, tamper-proof reputations on public blockchains. This is especially meaningful for users in emerging markets or those previously excluded by legacy banking rails. The decentralized credit bureau model is gaining traction, enabling protocols to assess borrowers without relying on opaque, centralized data sources.

Risk Management Gets Smarter (and Fairer)

One of the most underrated benefits of blockchain credit assessment is its impact on risk management. Protocols can now distinguish between high- and low-risk borrowers with unprecedented granularity. Instead of blanket liquidation triggers or one-size-fits-all collateral ratios, platforms can tailor loan terms based on dynamic, real-time credit data. This reduces unnecessary liquidations and creates a healthier lending environment for everyone involved.

For lenders, this means more predictable returns and lower default rates. For borrowers, it’s a chance to leverage their positive on-chain behavior for better rates and higher capital efficiency. The result? Lending pools that are both safer and more attractive – a win-win for protocol health and user growth. More details on how these mechanisms lower risk can be found here.

Challenges Ahead: Privacy, Standards, and Adoption

Despite the progress, several hurdles remain. Privacy is top of mind: while transparency is a strength of blockchain, users are rightfully concerned about exposing too much of their financial history. Leading protocols are experimenting with zero-knowledge proofs and selective disclosure tools to balance transparency with user privacy.

Another challenge is the lack of standardized scoring methodologies across platforms. As more DeFi lending protocols roll out their own versions of on-chain credit scores, interoperability and consistency will become critical for trust and adoption. Industry-wide standards could accelerate integration and make it easier for users to port their reputation across ecosystems.

DeFi Lending in 2025: The New Normal

With Aave trading at $236.22, Compound at $37.53, and Maker sitting at $1,388.49, the DeFi lending sector is entering a new era defined by data-driven trust instead of brute-force collateralization. The next wave of growth will likely come from further integrating real-world assets and expanding global access through decentralized identity solutions.

For builders and users alike, the message is clear: on-chain credit scoring isn’t just an upgrade – it’s the foundation for the next trillion dollars in DeFi lending. If you’re interested in how reputation-based lending is reshaping capital markets, read our analysis on reputation-based DeFi lending.