In 2024, the decentralized finance (DeFi) landscape underwent a pivotal transformation as on-chain reputation scores emerged as the backbone of next-generation credit markets. Historically, DeFi lending protocols relied on overcollateralization to mitigate risk, often demanding borrowers deposit assets worth 150% or more of their desired loan. This restriction, born from the absence of reliable credit assessment tools, stifled capital efficiency and excluded users without substantial crypto holdings. The arrival of blockchain-native reputation systems has fundamentally altered these dynamics by introducing a transparent, data-driven approach to evaluating borrower trustworthiness.

From Collateral Walls to Reputation Rails: The Shift in DeFi Credit Markets

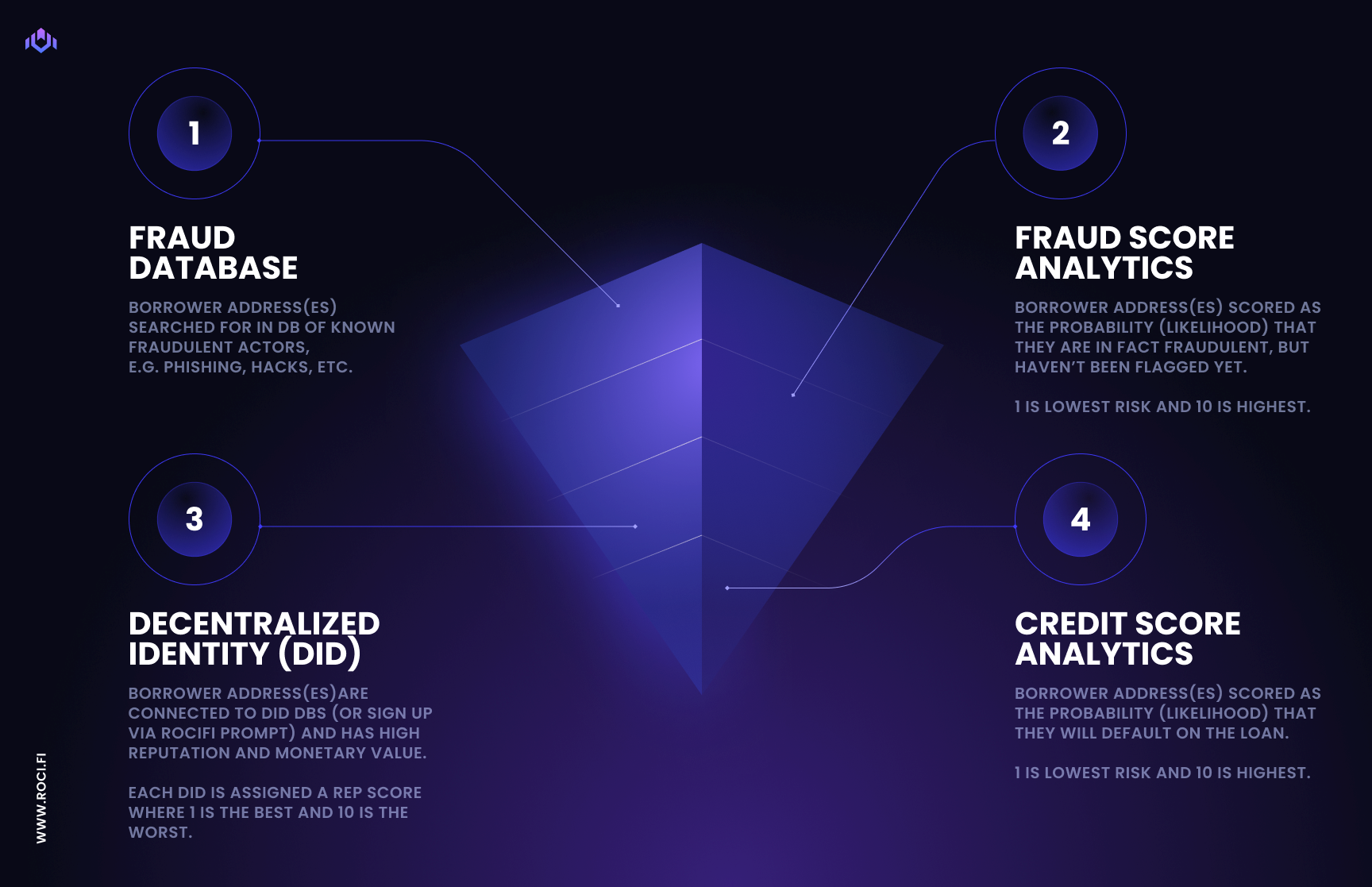

On-chain reputation scores, probabilistic measures derived from a user’s blockchain activity, have become essential for unlocking undercollateralized and even unsecured loans in DeFi. Unlike traditional credit bureaus that rely on opaque algorithms and off-chain financial data, decentralized credit bureaus analyze wallet interactions directly on-chain. These systems aggregate metrics such as transaction frequency, liquidity provision history, smart contract interactions, protocol participation, and repayment behavior across lending platforms.

Projects like ARCx and Spectral have pioneered decentralized scoring protocols that assign dynamic Web3 trust metrics to user addresses. By leveraging advanced analytics and machine learning models trained on vast sets of public ledger data, these protocols provide granular insights into both individual and institutional risk profiles. In July 2024, Credora’s integration of credit scores on-chain with partners like Clearpool and Obligate marked a watershed moment for transparent DeFi lending solutions. These advances have enabled more nuanced risk management strategies for lenders while broadening access to capital for borrowers who lack traditional credit histories.

How On-Chain Reputation Scores Work: Technical Foundations

The core premise behind on-chain reputation scoring is straightforward yet technically intricate: every blockchain transaction is an immutable datapoint that contributes to a user’s evolving financial identity. Decentralized scoring engines ingest this raw transaction history, trades on DEXs like Uniswap or Curve, liquidity positions in Aave or Compound, governance participation in DAOs, and synthesize it into a composite crypto credit score.

Protocols such as Cred Protocol and Deep Reputation Scoring frameworks utilize probabilistic models (e. g. , zScore-based analysis) to quantify wallet-level risk. These models weigh factors including:

- Transaction volume: Higher sustained activity signals economic engagement

- Diversity of protocol usage: Interacting with varied DeFi platforms demonstrates sophistication

- Repayment history: Timely loan repayments are critical trust indicators

- Time-weighted account age: Older wallets with consistent positive behavior are scored favorably

- Anomalous patterns detection: Identifying Sybil attacks or wash trading attempts ensures integrity

Key Metrics Used by Leading Crypto Credit Score Protocols

- Wallet Transaction History: Protocols like ARCx and Spectral analyze the frequency, volume, and diversity of on-chain transactions to assess a user's financial activity and reliability.

- Liquidity Provision and DeFi Participation: Metrics such as liquidity supplied to protocols like Aave and Compound, as well as engagement with decentralized exchanges, are used to gauge a user's risk appetite and commitment to the ecosystem.

- Borrowing and Repayment Behavior: Leading protocols, including Credora and Clearpool, evaluate timely loan repayments, default rates, and borrowing patterns to determine creditworthiness.

- Smart Contract Interaction Diversity: The variety and complexity of smart contracts a user interacts with, as tracked by Reputation DAO and ARCx, signal technical proficiency and ecosystem engagement.

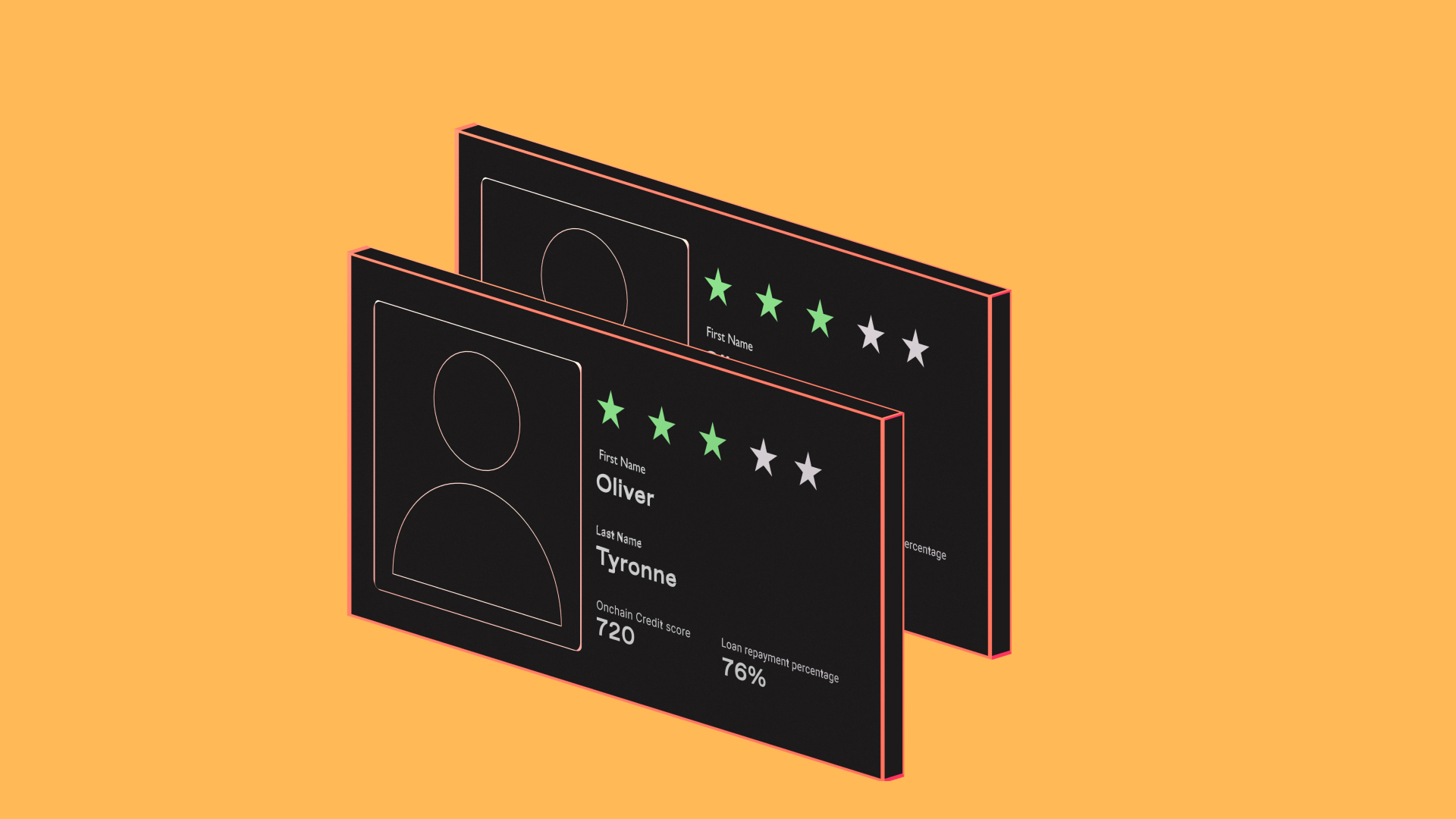

- Asset Holdings and Portfolio Stability: Protocols assess wallet balances, asset diversity, and portfolio volatility to measure financial resilience and risk exposure.

- Identity and Real-World Data Integration: Reputation DAO incorporates off-chain data, such as KYC and traditional credit information, to enhance the accuracy of on-chain credit assessments.

This data-driven approach enables more precise risk assessment compared to legacy systems that often overlook the nuances of digital asset ownership and peer-to-peer financial behavior. Importantly, users retain sovereignty over their identity; most protocols employ privacy-preserving techniques such as zero-knowledge proofs or selective disclosure mechanisms to protect sensitive information while still enabling robust blockchain credit assessment.

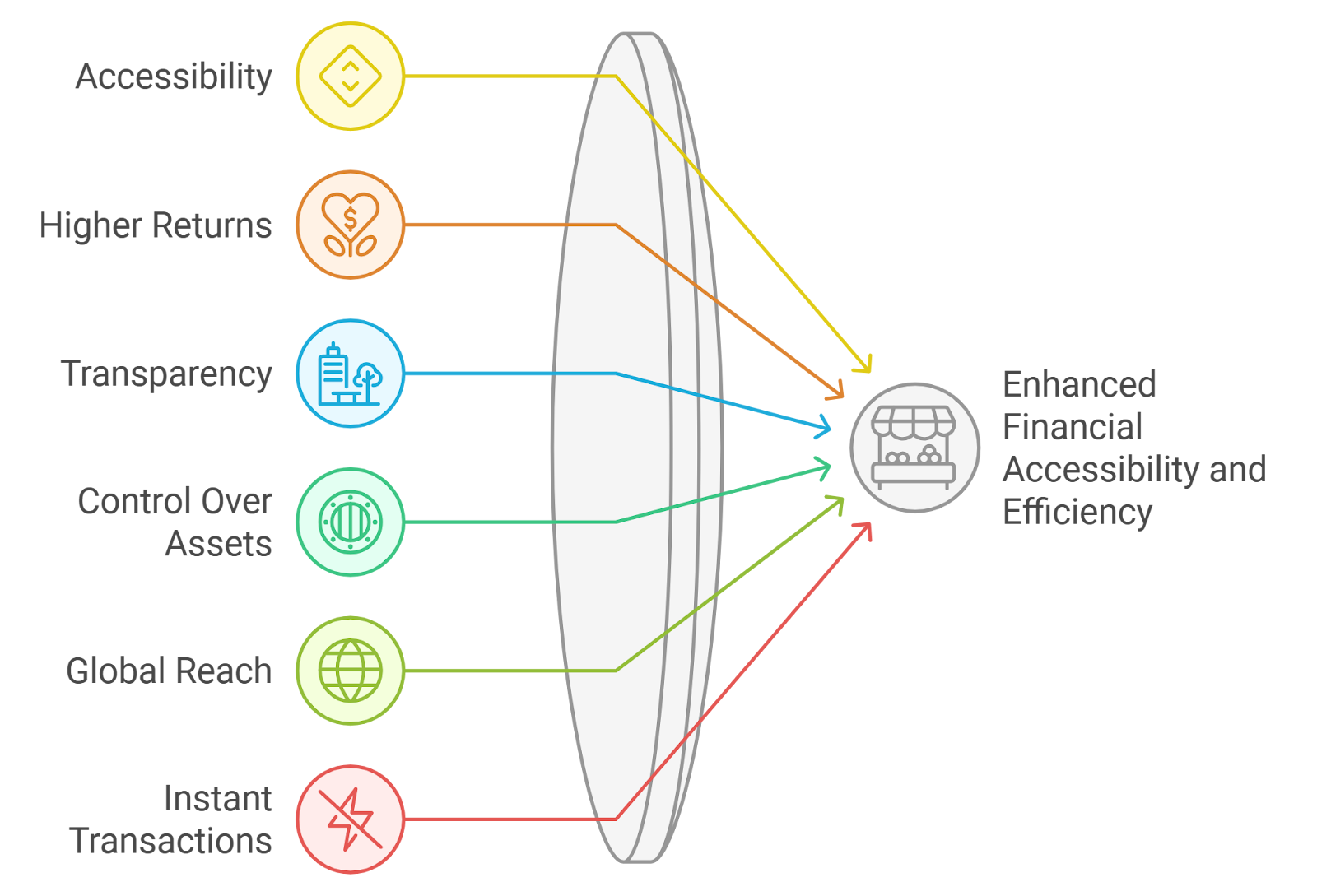

The Impact: Inclusion, Efficiency, and Transparency in Web3 Lending

The proliferation of on-chain reputation scores has catalyzed several paradigm shifts within DeFi:

- Financial inclusion: Users lacking formal banking relationships can now build crypto-native reputations through their on-chain actions alone.

- Improved capital efficiency: By enabling undercollateralized lending models, protocols unlock trapped liquidity and reduce barriers for emerging market participants.

- User empowerment: Individuals control their own reputational footprint, no centralized authority dictates access or terms.

- Ecosystem transparency: All scoring logic is verifiable on public ledgers or open-source codebases.

This new model is not without its technical challenges. The pseudonymous nature of wallet addresses complicates the construction of comprehensive user profiles; behavioral modeling must adapt across diverse DeFi contexts where incentives and risks vary widely between protocols. Yet the momentum is undeniable, as highlighted by Reputation DAO’s bridge between Web3 identities and real-world financial data streams, and the sector continues to iterate rapidly toward scalable solutions.

To explore further how these advances are unlocking collateral-free lending opportunities in DeFi markets, see our deep dive at /how-on-chain-reputation-scores-unlock-uncollateralized-loans-in-defi.

As 2024 unfolded, the practical applications of on-chain reputation scores began to reshape DeFi credit risk models at scale. Lenders now employ dynamic algorithmic frameworks to price risk, moving beyond static collateral ratios and toward adaptive, user-specific terms. This evolution has enabled the emergence of truly programmatic credit markets where loan conditions are continually recalibrated in response to a borrower’s evolving blockchain credit assessment.

Real-World Adoption: Protocols and Use Cases Leading the Charge

Major DeFi lending platforms have integrated crypto credit score protocols directly into their onboarding and risk management flows. For example, Clearpool leverages Credora’s on-chain scoring to facilitate institutional lending pools with tailored risk tranching, while Obligate uses decentralized credit bureaus to automate KYC-light processes for compliant borrowers. Reputation DAO’s multi-source approach, bridging on-chain analytics with verified off-chain credentials, enables a new spectrum of hybrid Web3 trust metrics that are already powering innovative lending products.

Meanwhile, retail-focused protocols like ARCx and Spectral provide granular wallet-level scores that users can port across ecosystems. This portability is critical: it allows individuals to build reputational capital that persists even as they migrate between protocols or chains, cementing the foundation for a robust decentralized credit bureau infrastructure.

Top DeFi Platforms Using On-Chain Reputation Scores in 2024

- Credora integrated on-chain credit scores in July 2024, partnering with Clearpool and Obligate to enable transparent, efficient undercollateralized lending in DeFi markets.

- Reputation DAO bridges DeFi and traditional finance by allowing users to leverage real-world financial data and on-chain activity for nuanced credit assessments, expanding DeFi lending access.

- ARCx offers a decentralized scoring protocol that analyzes users’ on-chain trading history, liquidity provision, and smart contract interactions to assign credit scores for DeFi lending.

- Spectral provides a decentralized credit scoring system that evaluates wallet behavior and historical transactions, supporting on-chain identity and reputation-based lending.

- Cred Protocol delivers transparent, decentralized credit scoring by analyzing on-chain transaction data, helping users build blockchain-based financial reputations for use in lending protocols.

Challenges Ahead: Security, Privacy, and Standardization

While the momentum is strong, several hurdles must be addressed before on-chain reputation scoring achieves universal adoption. Sybil resistance remains a persistent technical challenge; sophisticated actors may attempt to game the system by distributing activity across multiple wallets. Advanced anomaly detection algorithms and cross-protocol behavioral analysis are essential tools in combating these threats.

Privacy preservation is equally critical. As more granular behavioral data feeds into scoring engines, maintaining user confidentiality without sacrificing transparency demands ongoing innovation, zero-knowledge proofs and selective disclosure frameworks continue to evolve as industry standards. Additionally, interoperability between competing scoring protocols and agreement on standardized metrics will be crucial for ecosystem-wide trust.

The future of DeFi credit markets will hinge not just on technical sophistication but on community-driven governance of these reputation systems, ensuring fairness, auditability, and resilience against manipulation.

Looking Forward: The Roadmap for Decentralized Credit Bureaus

The trajectory of DeFi lending is clear: as blockchain-native reputation systems mature, they will unlock unprecedented capital flows while minimizing systemic risk. The next phase will likely see deeper integration with real-world assets (RWAs), expansion into emerging markets lacking traditional financial infrastructure, and increased regulatory engagement as decentralized credit bureaus prove their robustness at scale.

For users and builders alike, mastering these new Web3 trust metrics is no longer optional, it’s foundational for accessing opportunity in the next era of programmable finance. To understand how undercollateralized lending is being powered by these innovations right now, explore our latest coverage at /how-on-chain-reputation-scores-are-powering-under-collateralized-defi-lending-in-2025.

How confident are you in DeFi's shift to reputation-based lending using on-chain credit scores?

With the rise of on-chain reputation systems in 2024, DeFi lending is moving beyond overcollateralization to more inclusive, credit score-based models. Do you trust these new systems to make DeFi lending safer and fairer?

No comments yet. Be the first to share your thoughts!