Imagine a world where your blockchain wallet is your passport to financial trust. That’s the promise of on-chain credit scores: a decentralized reputation system built for the next era of DeFi lending. As the crypto economy matures, the old rules of over-collateralization and anonymous risk are being rewritten. On-chain credit scoring is leading this charge, unlocking new capital flows and making DeFi lending smarter, fairer, and radically more inclusive.

From Wallet Activity to Credit Reputation

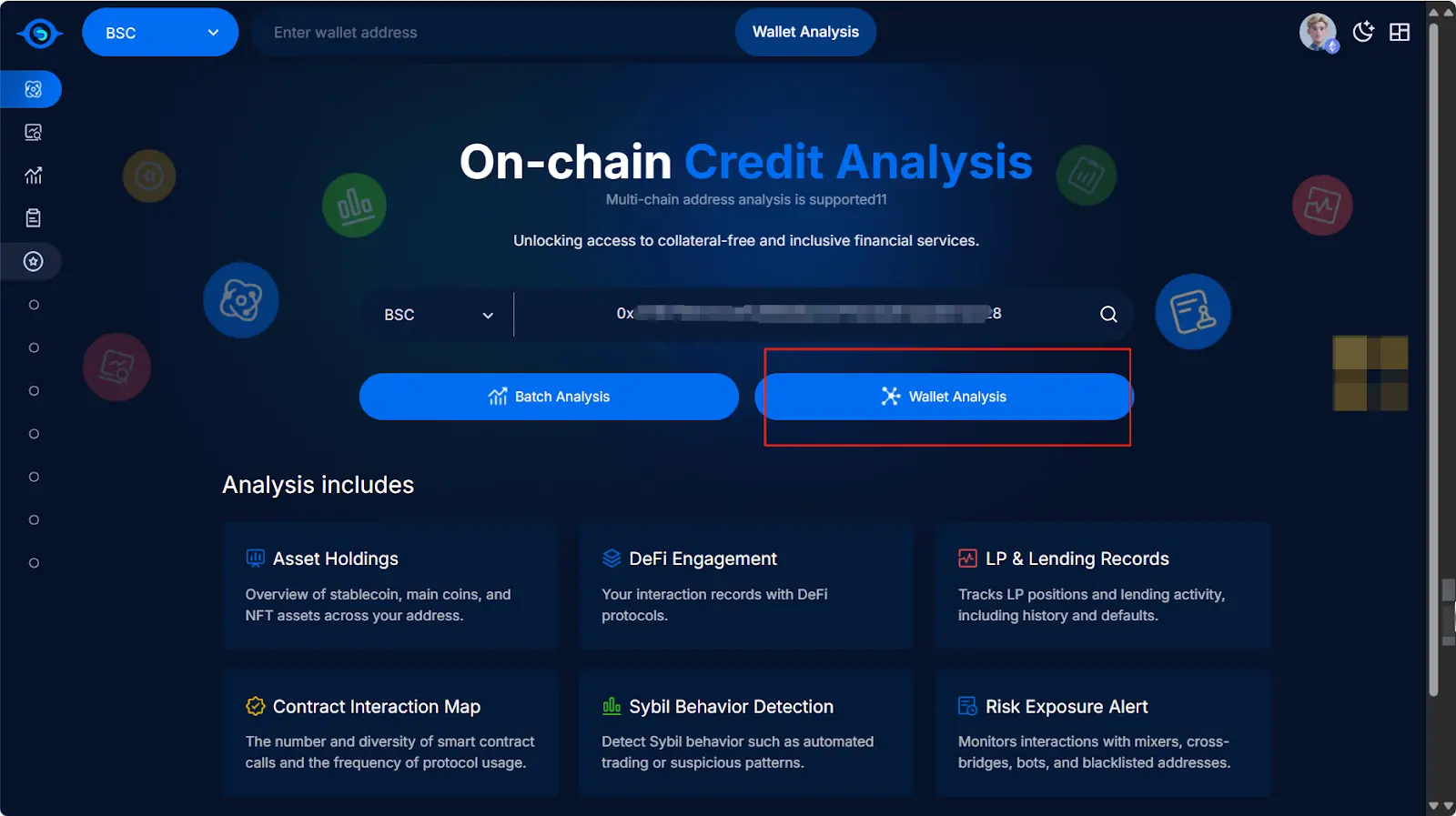

Traditional finance relies on opaque, centralized credit bureaus. In contrast, on-chain credit scores are generated by analyzing your public blockchain footprint. Every transaction, liquidity provision, loan repayment, staking action, becomes part of your evolving digital reputation. The key innovation? These scores are tied to wallet addresses rather than personal identities, preserving privacy while enabling trust. DeFi protocols can now assess who’s trustworthy based on hard data, not paperwork.

Key Benefits of On-Chain Credit Scores in DeFi

- Financial Inclusion: On-chain credit scores allow users without traditional credit histories to access DeFi lending, opening financial services to a broader, global audience.

- Transparency & Security: Credit assessments are recorded on immutable blockchains, ensuring transparent and tamper-proof evaluations that foster trust among users and lenders.

- Capital Efficiency: Lenders can offer under-collateralized or uncollateralized loans to users with strong on-chain credit scores, maximizing capital utilization across DeFi platforms.

- Automated & Always-On Access: On-chain credit scoring enables automated, 24/7 lending and borrowing, powered by smart contracts and stablecoins.

- Privacy by Design: Credit scores are tied to wallet addresses, not personal identities, preserving user privacy while enabling reputation-based lending.

- Interoperable Reputation: Users can port their on-chain credit scores (like RociFi NFCS or CreDA cNFTs) across supported DeFi platforms, building a portable reputation and unlocking better loan terms.

Here’s how the process unfolds:

- Data Collection: Protocols aggregate your on-chain activity, asset holdings, transaction volumes, DeFi interactions, directly from the blockchain ledger.

- Score Calculation: Advanced algorithms and AI models crunch this data to generate a real-time credit score. It’s not just about wallet balance; it’s about patterns of responsible behavior, repayment consistency, and protocol engagement.

- Score Utilization: Your score can be minted as an NFT or digital credential. Flash it to DeFi platforms to access better loan terms: lower collateral requirements, reduced interest rates, or even uncollateralized loans for top performers.

Why On-Chain Credit Scores Are Exploding in 2025

In 2025, on-chain credit scores are at the heart of a trillion-dollar shift in DeFi. With unprecedented transparency and automation, these scores are breaking down barriers:

- Financial Inclusion: No traditional credit history? No problem. If you’re active and responsible on-chain, you can build a wallet trust score that opens doors to new financial opportunities.

- Capital Efficiency: Lenders can finally offer under-collateralized or even uncollateralized loans, something that’s been nearly impossible in pure crypto until now. More capital is put to work, and everyone wins.

- Security and Transparency: Because everything’s on-chain, credit scores are tamper-proof and auditable. No backroom deals or hidden criteria, just verifiable blockchain data.

Want to dive deeper into how this tech is transforming trust? Check out how on-chain credit scores are transforming trust and lending in DeFi.

Real-World Protocols: Who’s Building DeFi’s Reputation Layer?

The race to define decentralized credit bureaus is heating up. Here are three standout projects shaping the on-chain credit landscape:

- CreDA: Analyzes users’ blockchain activity and lets them mint Credit NFTs (cNFTs), unlocking leveraged lending and low-collateral loans via partners like FilDA.

- RociFi: Issues Non-Fungible Credit Scores (NFCS) based on wallet behavior. These scores serve as both loan credentials and trust signals across DeFi.

- Credora: Integrates on-chain credit scores into lending markets, boosting transparency and enabling risk-based pricing for borrowers and lenders alike.

Each protocol takes its own approach to crypto credit scoring, but all share one goal: make blockchain reputation as powerful as any legacy credit report, without sacrificing privacy or decentralization.

But this new era of blockchain credit assessment isn’t without its growing pains. As protocols race to integrate wallet trust scores, the industry faces three core challenges: privacy, standardization, and Sybil resistance. Let’s break them down.

Overcoming Challenges: Privacy, Interoperability, and Security

Data privacy is non-negotiable. While on-chain data is public by design, linking wallet addresses to real-world identities could undermine user security and DeFi’s open ethos. The best decentralized credit bureaus are doubling down on zero-knowledge proofs and selective disclosure, proving your score without revealing every detail of your transaction history.

Standardization is the next frontier. With dozens of protocols calculating scores in slightly different ways, borrowers face a fragmented landscape. Imagine if every bank had its own FICO scale! Cross-protocol standards are emerging to ensure your reputation follows you wherever you go in DeFi, no matter which chain or dApp you’re using.

Sybil attacks remain a persistent threat. Bad actors could spin up thousands of wallets to game the system for uncollateralized loans. Combatting this requires robust identity heuristics, behavioral analytics, and ongoing monitoring, all while preserving user pseudonymity.

What’s Next for DeFi Lending Reputation?

The momentum behind DeFi risk analysis tools is only accelerating. As more capital pours into uncollateralized lending markets, expect on-chain credit scores to become a default layer for everything from borrowing stablecoins to accessing premium yield vaults. Wallet reputation will soon influence far more than just loan terms, it could unlock governance rights, exclusive protocol access, or even serve as a universal Web3 passport.

Key Use Cases Unlocked by On-Chain Credit Scores in 2025

- Uncollateralized and Under-Collateralized Lending: On-chain credit scores enable DeFi platforms like RociFi and CreDA to offer loans with little or no collateral, making DeFi lending more accessible and capital efficient.

- Automated, Risk-Based Loan Pricing: By integrating real-time credit data, DeFi lenders can dynamically adjust interest rates and loan terms based on a borrower's on-chain score, improving risk management and transparency.

- Broader Financial Inclusion: On-chain credit scoring opens up lending to users without traditional credit histories, especially in emerging markets, driving global access to decentralized financial services.

- Interoperable Credit Markets: Standardized on-chain credit scores enable cross-platform lending and borrowing, allowing users to leverage their reputation seamlessly across various DeFi ecosystems.

This shift isn’t just technical, it’s cultural. By rewarding responsible behavior and transparency over anonymity and speculation, decentralized credit bureaus are setting new norms for trust in crypto finance. Forget the old gatekeepers: now your actions on-chain speak louder than any off-chain paperwork ever could.

Ready to Build Your On-Chain Reputation?

If you’re serious about maximizing your DeFi potential in 2025 and beyond, it pays to start optimizing your wallet trust score today:

- Repay loans promptly: Every successful repayment boosts your score across integrated platforms.

- Diversify protocol engagement: Interact with reputable lending pools, DEXs, and staking services.

- Avoid risky behaviors: Liquidations or defaulting on obligations can tank your crypto credit profile fast.

This isn’t just about access, it’s about leverage and opportunity as the decentralized economy scales up. Want more actionable strategies? Explore our deep dive into how on-chain credit scores power trust and lower risk in DeFi lending.

The bottom line? The future of DeFi belongs to those who treat their wallet as both a key, and a credential, for global financial access. Your next big opportunity could be just one transaction away from a higher score, and an open door into Web3’s most dynamic lending markets.

No comments yet. Be the first to share your thoughts!