Web3 is on the verge of a seismic shift, and it’s not just about NFTs or smart contracts. The real revolution? Decentralized reputation and identity. As Bitcoin holds steady at $115,482.00, the spotlight is turning to how crypto credit scores are being woven into the fabric of digital identity across blockchain ecosystems. This integration doesn’t just promise more secure lending - it’s unlocking a new era of trust, efficiency, and inclusivity for users and protocols alike.

The Rise of Decentralized Reputation: Why Web3 Needs Credit Scores

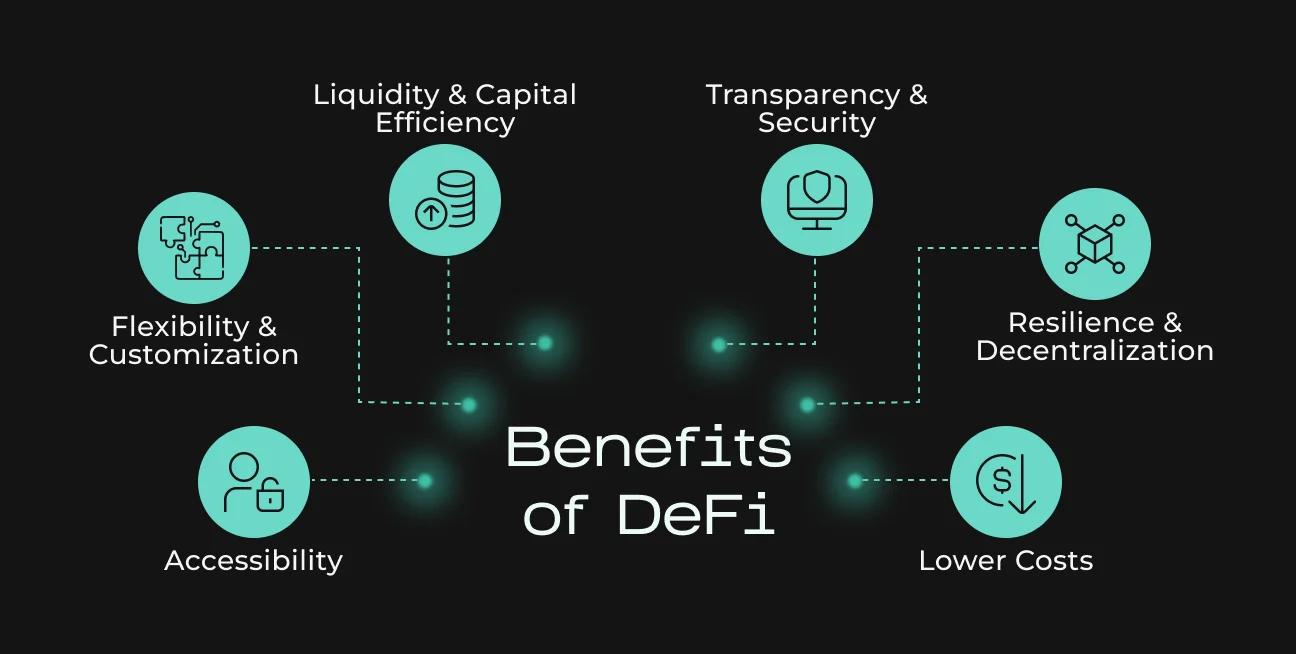

Traditional finance relies on centralized credit bureaus to assess risk, but these systems are riddled with inefficiencies and privacy concerns. Web3 flips the script by empowering individuals through self-sovereign identity (SSI) - where you control your data, not some faceless institution. Integrating crypto credit scores into this landscape enables users to carry their financial reputation across platforms, opening doors to loans, DAOs, and even real-world asset tokenization.

The latest wave of innovation is all about composability and privacy:

Top 5 Crypto Credit Scoring Protocols Powering Web3 Identity

- zkMe's zkCreditScore: zkMe enables anonymous on-chain bridging of US FICO credit scores, enhancing privacy while empowering DeFi and real-world asset tokenization with trusted, verifiable identities.

- DeCredit's Credit Oracle: DeCredit fuses on-chain and off-chain credit data into a decentralized scoring oracle, giving users control over their credit profiles and supporting self-sovereign identity solutions.

- TransUnion's DeFi Credit Score Integration: TransUnion, a leading credit bureau, now provides credit scores to blockchain networks, allowing users to share their credit history with dApps for more accessible and secure DeFi lending.

- Spectral's Web3 Credit Scores: Spectral is building decentralized credit risk infrastructure for Web3, enabling composable credit scores that can be integrated across DeFi and identity platforms.

- Creditlink's AI-Driven Credit Modules: Creditlink leverages AI-powered credit modules and NFTs to deliver credit scoring as a service, boosting trust and risk management for DAOs, DeFi, and cross-chain applications.

From AI-driven modules by Creditlink, to privacy-first solutions like zkMe's zkCreditScore, decentralized reputation is rapidly becoming the backbone of DeFi risk management. Major players like TransUnion are even bridging off-chain scores onto blockchain networks (read more here), signaling that mainstream adoption is accelerating.

How On-Chain Credit Scores Power Next-Gen Web3 Identity Solutions

The fusion of on-chain analytics with digital identity unlocks powerful new use cases:

- Frictionless DeFi lending: Users with verifiable credit can access loans with lower collateral requirements.

- DAO membership and governance: Reputation-based access ensures only trusted actors participate in key decisions.

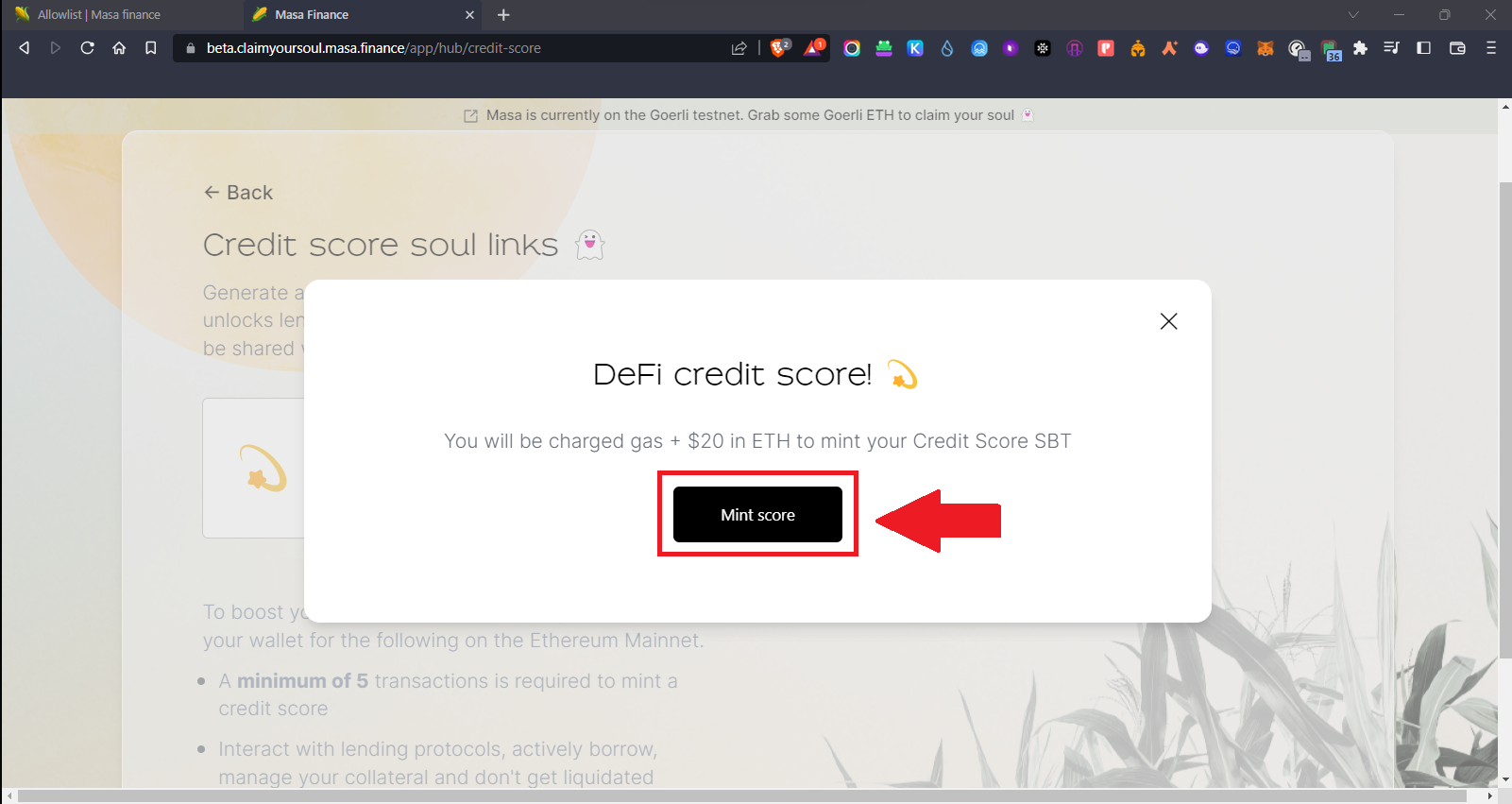

- KYC without compromise: Protocols like Masa Finance mint soulbound tokens for KYC and credit verification directly on Ethereum (see Cointelegraph coverage).

- Anonymity meets credibility: Zero-knowledge proofs allow users to prove their trustworthiness without revealing sensitive details - a game changer for privacy-centric DeFi.

This isn’t theoretical - it’s already live. Protocols like DeCredit's Credit Oracle combine on-chain and off-chain data in stages, moving from centralized feeds toward fully decentralized models where users own their distributed identities (DIDs). Meanwhile, SecureScore’s blockchain network (learn more here) puts privacy front-and-center, ensuring only authorized parties access your trust score.

Pushing the Boundaries: Privacy-Preserving Credit Scoring in Action

If you think integrating traditional FICO scores into crypto sounds wild - you’re right. zkMe’s zkCreditScore lets users bridge US FICO scores onto public blockchains anonymously, using zero-knowledge proofs to verify without exposing private details (details here). This opens doors for undercollateralized lending and real-world asset tokenization while safeguarding user privacy.

The implications are massive: platforms can tap a broader pool of users while minimizing risk; individuals can leverage their hard-earned reputation globally; all with security baked in at every layer. And as AI-powered decentralized scoring models emerge (see IdeaUsher), expect smarter, fairer algorithms that draw from both Web2 and Web3 data sources for maximum accuracy.

But this is just the beginning. The next evolution in Web3 identity solutions will be defined by interoperability, composability, and user-centric control. As more protocols adopt decentralized reputation infrastructure, the days of being locked into a single ecosystem, or judged by opaque algorithms, are numbered. Instead, your on-chain actions, creditworthiness, and even governance participation become portable credentials you can leverage across DeFi platforms, NFT marketplaces, or DAOs.

What’s Next? The Roadmap for Decentralized Credit and Identity

The integration of crypto credit scores with identity solutions is catalyzing a new wave of products and services:

- Composable Identity Layers: Modular identity stacks let users selectively share credentials, proving creditworthiness for a loan or DAO membership without exposing their full history.

- Cross-Chain Reputation: As bridges mature, expect to see credit scores travel seamlessly between Ethereum, Solana, and beyond, enabling trust across fragmented Web3 silos.

- Soulbound Credentials: Innovations like Masa Finance’s soulbound tokens are creating non-transferable proof of KYC and credit status, setting new standards for Sybil resistance and anti-fraud measures.

- AI-Enhanced Scoring: AI models are pulling from both blockchain analytics and traditional data feeds to build nuanced risk profiles that adapt as user behavior evolves.

Real-World Use Cases for Crypto Credit Scores in Web3

- DeFi Lending with DeCredit's Credit Oracle: DeCredit's oracle integrates on-chain and off-chain credit data, empowering users to leverage their creditworthiness for lower collateral loans on decentralized platforms.

- AI-Powered Risk Assessment by Creditlink: Creditlink's composable credit modules use AI to optimize lending, DAO participation, and cross-chain trust, enabling smarter, more inclusive financial services in Web3.

- Privacy-First Credit Sharing via zkMe's zkCreditScore: zkMe enables users to anonymously bridge their US FICO scores on-chain, allowing dApps to verify creditworthiness without compromising privacy.

- Secure Digital Identities from SecureScore: SecureScore provides blockchain-based digital identities with built-in credit and trust scores, helping platforms verify users securely and efficiently.

- Traditional Credit Data in DeFi with TransUnion: TransUnion brings established credit scores to blockchain networks, allowing users to share verified credit histories directly with DeFi lenders for streamlined borrowing.

- Reputation Building through Spectral's Web3 Scores: Spectral's decentralized credit scoring infrastructure lets users build on-chain reputations, unlocking access to loans, governance, and other Web3 privileges.

- On-Chain KYC and Credit with Masa Finance: Masa Finance issues soulbound tokens for KYC and credit scores, standardizing identity verification and credit assessment within Ethereum-based ecosystems.

- Credential Management by ShoCard: ShoCard leverages blockchain for secure management of identity and credit credentials, enabling users to prove their trustworthiness across multiple platforms.

- Cross-Platform Reputation with cheqd's DSID: cheqd's Decentralized Self-Sovereign Identity (DSID) allows users to enrich their reputation scores by integrating data feeds from both Web2 and Web3, enhancing their trust profile everywhere.

The market is responding fast. Lenders are slashing collateral requirements for users with robust on-chain reputations. DAOs are using decentralized scores to vet contributors. Even mainstream institutions like TransUnion are signaling confidence by bridging off-chain data into DeFi (see details). This convergence isn’t just technical, it’s cultural. It marks a shift from exclusionary gatekeeping to radical financial inclusion.

Risks and the Path Forward

No system is perfect. Privacy remains paramount; even with zero-knowledge proofs and privacy-preserving protocols like SecureScore or zkMe’s zkCreditScore, there are ongoing debates about data sovereignty and algorithmic bias. As more AI-driven modules come online (see Creditlink), transparency in scoring criteria will be crucial to avoid replicating TradFi’s pitfalls in the decentralized world.

The good news? The open-source ethos of Web3 means these systems are auditable, and communities have a say in how reputation frameworks evolve. This participatory approach will be key to balancing innovation with user protection as crypto credit scoring becomes ubiquitous across digital identities.

Bitcoin at $115,482.00: Why Market Momentum Magnifies the Stakes

The timing couldn’t be better. With Bitcoin holding strong at $115,482.00, liquidity is surging into DeFi protocols hungry for more efficient risk management tools, and decentralized reputation fills that gap perfectly. As these systems mature, expect borrowing costs to fall for reputable users while fraudsters find fewer loopholes to exploit.

If you’re building or investing in Web3 today, integrating crypto credit scores isn’t optional, it’s table stakes for trust in the next generation of digital economies.

No comments yet. Be the first to share your thoughts!