Decentralized Identity (DID) is quietly supercharging the future of on-chain credit scoring in Web3. Instead of relying on banks or centralized agencies to verify who we are, DIDs put individuals in the driver’s seat, letting them control their own data and privacy. This isn’t just a technical upgrade - it’s a fundamental shift in financial empowerment and trust.

What Makes Decentralized Identity the Missing Link?

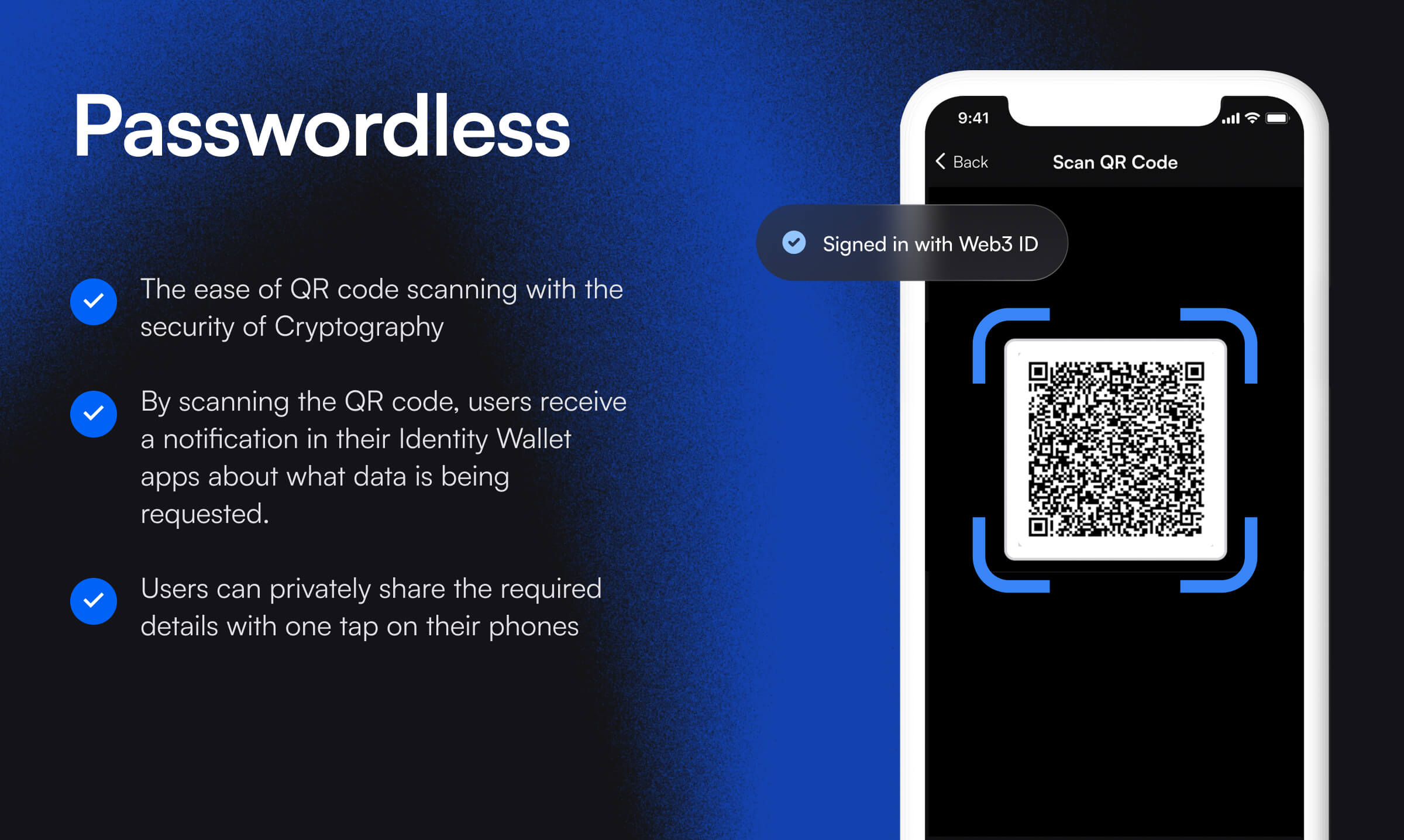

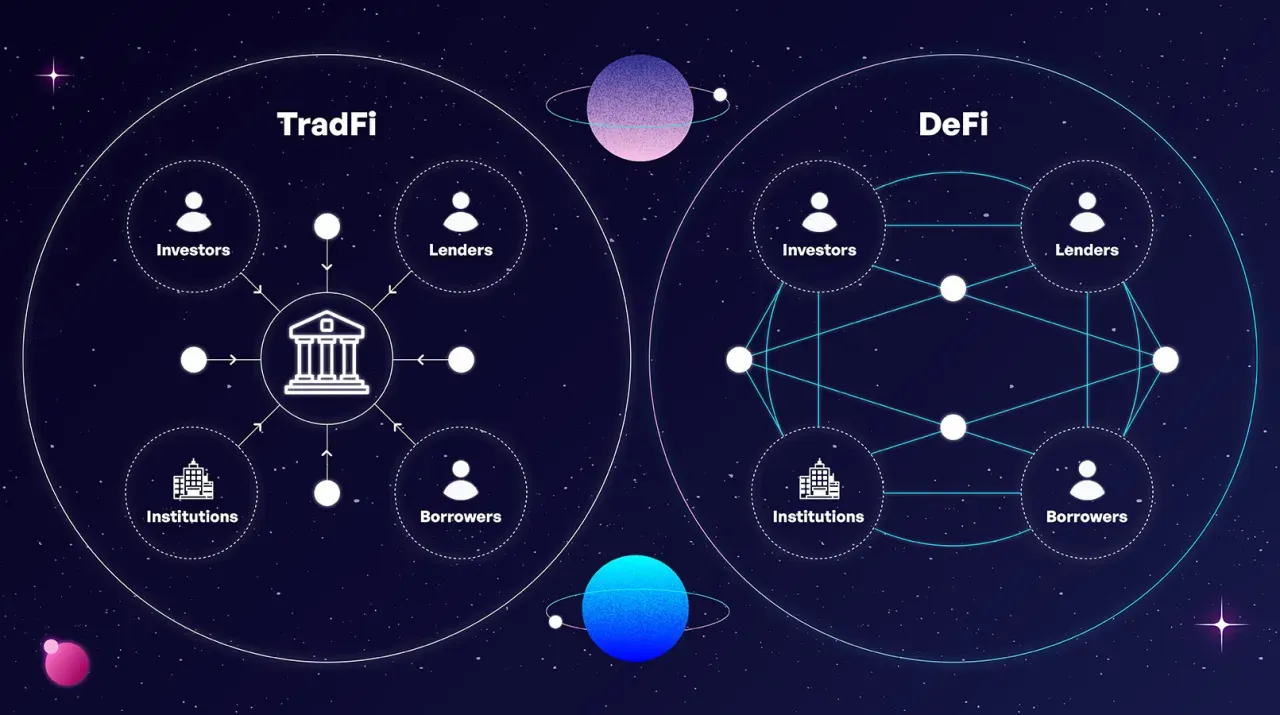

In traditional finance, your creditworthiness is locked behind closed doors and siloed databases. In contrast, decentralized identity Web3 solutions like idOS are building an open, portable identity layer for digital finance. With idOS, you verify your KYC once and can access any stablecoin app on any blockchain, no need to repeat the process for every new protocol. This interoperability is a game-changer for both users and developers.

The beauty of DIDs lies in their self-sovereign nature. You own your credentials, decide what to share, and move seamlessly between platforms without losing reputation or privacy. As highlighted by industry voices:

DID-Powered Credit Scoring: The New Trust Layer

On-chain credit scoring is evolving beyond simple wallet analytics. Today’s most innovative projects are blending DID frameworks with advanced analytics to create transparent and fair credit systems:

Top DID-Powered On-Chain Credit Scoring Projects

- DeCredit: Pioneering a credit oracle that blends on-chain and off-chain data, DeCredit empowers users to manage their credit profiles in Web3 with more accurate, comprehensive scoring. Learn more

- Creditlink: Leveraging AI-driven analytics, Creditlink builds composable credit modules that enhance trust across DeFi, DAOs, and cross-chain ecosystems. Their services include Credit Scoring as a Service and Credit NFT Issuance. Explore Creditlink

- Reputation DAO: Offering verifiable, decentralized credit scores, Reputation DAO bridges off-chain data (like KYC and traditional credit) with on-chain protocols, helping DAOs and smart contracts assess risk more reliably. Discover Reputation DAO

- CreDA: Using DIDs and verifiable credentials, CreDA links on-chain and off-chain financial data to deliver privacy-preserving credit scores, expanding DeFi access globally. Read about CreDA

- zkMe: With zkCreditScore, zkMe enables anonymous bridging of US FICO credit scores on-chain, supporting privacy and credibility for DeFi and real-world asset tokenization. See zkMe in action

DeCredit, for example, merges both on-chain and off-chain data through its credit oracle (decredit.io). Creditlink leverages AI to build modular credit profiles that travel with you across DeFi ecosystems (creditlink.info). Meanwhile, Reputation DAO brings verifiable off-chain information like AML/KYC directly into smart contracts, bridging real-world trust into decentralized protocols (chaincatcher.com). CreDA uses verifiable credentials to link off-chain financial data with DeFi lending while preserving privacy (elastos.info). And then there’s zkMe's zkCreditScore, which enables anonymous bridging of US FICO scores on-chain using zero-knowledge proofs (blog.zk.me).

The Rise of Privacy-Preserving KYC in Blockchain Finance

KYC has always been a sticking point for crypto adoption, users want access but not at the expense of privacy or decentralization. Solutions like Blockpass’ On-Chain KYC® 2.0 are transforming digital identity by creating reusable digital IDs that work across multiple services while keeping sensitive data under user control. Privacy-preserving verification methods such as device-based face checks (no fancy scanners needed!) are making onboarding smoother than ever.

This new era means you can prove who you are, or at least that you’re trustworthy, without oversharing personal details or relying on third-party gatekeepers. It’s not just about compliance; it’s about building real trust between strangers in an open ecosystem.

Projects like idOS and Blockpass are leading the charge in making privacy-preserving KYC a practical reality for everyday users. With solutions that let you verify once and roam freely across DeFi, your digital identity becomes as portable as your wallet. No more clunky onboarding or redundant document uploads, just seamless, secure access to the decentralized economy.

The implications for on-chain credit scoring are profound. By leveraging self-sovereign identities, DeFi protocols can move beyond over-collateralization, a major friction point that locks out millions from borrowing and lending opportunities. Instead, risk assessment becomes about real behavior and verifiable credentials, not just how much crypto you can lock up.

Unlocking Capital and Inclusion with DID-Based Credit

Let’s talk about what this means for users and the broader Web3 ecosystem. First, DID-powered credit scoring unlocks capital efficiency. Lenders can offer better terms to borrowers with strong reputations, even if they don’t have a long history on one particular chain or protocol. This is especially powerful for users in emerging markets or those without access to traditional credit systems.

The integration of off-chain data via platforms like DeCredit, Creditlink, and CreDA means that even if you’re new to crypto, your real-world financial behavior can help you get started in DeFi. Meanwhile, innovations like zkMe’s zkCreditScore bring established metrics (like FICO scores) into the world of smart contracts, without doxxing your identity.

Top Benefits of DID-Based On-Chain Credit Scoring

- Privacy-First Credit Assessments: Decentralized Identity (DID) platforms like idOS and Blockpass empower users to control and selectively share personal data, enabling credit scoring without exposing sensitive information. Privacy-preserving technologies such as zero-knowledge proofs (used by zkMe's zkCreditScore) ensure that only necessary data is revealed to lenders or protocols.

- True Portability Across Platforms: With DIDs, your verified identity and credit history travel with you—across blockchains and DeFi apps. Solutions like idOS and Creditlink make it possible to verify once and access multiple services, eliminating repetitive KYC checks and unlocking seamless experiences throughout the Web3 ecosystem.

- Financial Inclusion for All: DID-powered credit scoring (as seen with DeCredit and CreDA) integrates both on-chain and off-chain data, allowing people without traditional credit histories to access DeFi lending and other financial services. This opens doors for the unbanked and underbanked globally.

- Trustless and Transparent Risk Assessment: Platforms like Reputation DAO and DeCredit leverage DIDs and smart contracts to automate credit scoring, reducing bias and human error. This trustless approach ensures risk is assessed transparently, with verifiable credentials and auditable logic.

- Reduced Collateral, More Efficient Capital: By enabling accurate, reputation-based lending, DID-based systems (such as Creditlink and CreDA) can lower or remove over-collateralization requirements. This means users can borrow more with less locked capital, making DeFi lending more accessible and efficient.

This isn’t just theory, it’s happening now. DAOs are using composable credit modules to streamline membership decisions; NFT marketplaces are rewarding reputable buyers and sellers; lending pools are slashing collateral requirements thanks to more accurate risk models powered by DIDs.

What’s Next? Scaling Trust Across Chains and Borders

The future looks bright, and interoperable. As DID standards mature and more protocols adopt privacy-preserving KYC solutions, expect to see a Cambrian explosion of cross-chain financial products built on trust rather than brute-force collateralization.

Your reputation will be as portable as your assets. Whether you’re seeking a loan on Ethereum or joining a DAO on Solana, your verified credentials will travel with you. And because these systems minimize data leakage through selective disclosure and zero-knowledge proofs, you won’t be giving up privacy for convenience.

If you’re building in Web3, or simply want fairer access to decentralized finance, now is the time to pay attention to decentralized identity initiatives like idOS network credit score projects and privacy-preserving KYC blockchain tools. They’re not only making compliance easier but also opening doors for global financial inclusion at a scale we’ve never seen before.

No comments yet. Be the first to share your thoughts!