In the high-stakes arena of decentralized finance, where capital efficiency reigns supreme, a quiet revolution is underway on Solana. Borrowers no longer need to tie up fortunes in collateral to access loans. FairScore on-chain reputation is emerging as the game-changer, dynamically assessing user trustworthiness to unlock higher DeFi uncollateralized loans and elevated borrowing limits. This Solana-native system, developed by FairScale, aggregates on-chain activity, social signals, and off-chain data into a living score that protocols trust implicitly. For everyday crypto users and power protocols alike, it’s a pathway to fluid capital without the drag of overcollateralization.

Picture this: you’ve built a track record of timely repayments, consistent liquidity provision, and positive community engagement across Web3. In traditional DeFi, that history means little without locking 150% or more in assets. But with FairScore, your reputation translates directly into expanded Solana borrowing limits. Lenders can offer terms closer to 1: 1 or even undercollateralized, slashing opportunity costs and fueling growth. This isn’t hype; it’s the logical next step as DeFi matures beyond its clunky origins.

The Collateral Trap Holding DeFi Back

DeFi lending protocols like those on Solana have exploded in popularity, but they’re shackled by a core flaw: mandatory overcollateralization. Borrowers must deposit assets worth far more than the loan amount to buffer against volatility and defaults. This setup protects lenders, sure, but it starves users of liquidity. A $10,000 loan might demand $15,000-$20,000 upfront, leaving little room for traders, yield farmers, or builders to maneuver.

Industry voices echo this frustration. Sources from Bankless and CoinGecko highlight how this model limits DeFi’s reach, confining it to whales while sidelining retail participants. On Solana, protocols are pushing boundaries with cross-chain collateral, yet the inefficiency persists. Enter reputation systems like FairScore, which layer behavioral data atop raw holdings. By quantifying reliability, they enable protocols to dial down collateral ratios for proven users, fostering Web3 reputation tiers that reward long-term alignment over one-off deposits.

5 Key Benefits of Rep-Based Lending

-

Higher Capital Efficiency: Reputation systems like FairScore on Solana enable undercollateralized loans, freeing up user capital that would otherwise be locked in overcollateralized DeFi positions (as noted in CoinGecko reports on DeFi lending). Borrowers deploy assets productively instead of idle collateral.

-

Lower Entry Barriers for New Users: Without needing upfront collateral, newcomers can access borrowing via on-chain reputation from protocols like FairScore, which aggregates on-chain and off-chain data—lowering barriers highlighted in Huma Finance’s guide to decentralized credit.

-

Real-Time Risk Adjustment: FairScore’s dynamic scores evolve with user behavior, allowing DeFi platforms to adjust borrowing limits instantly, as discussed in Bankless on benchmarking on-chain risk like ‘DeFi LIBOR’.

-

Incentive for Good Behavior: Trustworthy actions boost scores, unlocking better rates and higher limits—encouraging positive on-chain habits, per Mitosis University’s analysis of on-chain credit scoring.

-

Scalable Undercollateralized Loans: Reputation enables mass scaling of uncollateralized lending, as in Zama’s confidential lending vision and GARP’s risk management for DeFi, bypassing collateral constraints for broader adoption.

I’ve analyzed market cycles for 18 years, from commodities booms to crypto winters, and this shift feels inevitable. Reputation isn’t just a score; it’s a decentralized signal of intent, much like how traditional bureaus evolved from rudimentary checks to sophisticated models.

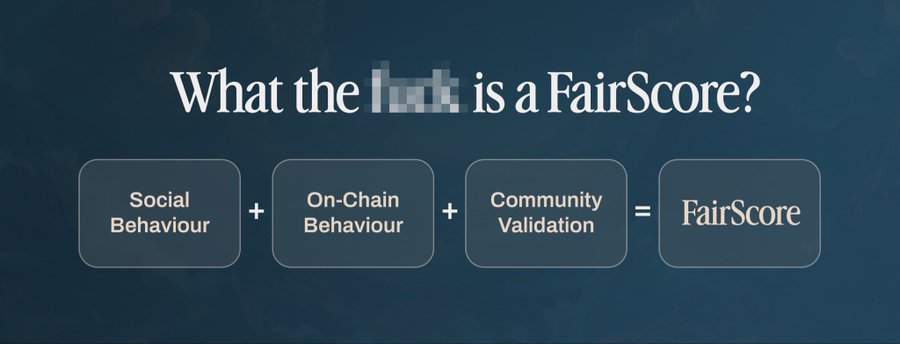

Unpacking FairScore: Anatomy of an On-Chain Reputation Engine

FairScore stands out in the crowded field of on-chain credit tools by its holistic approach. Built on Solana for speed and low costs, it pulls from diverse sources: transaction histories showing repayment patterns, social graphs revealing community standing, and off-chain verifications for added depth. The result? A dynamic score that updates in real-time, reflecting every swap, stake, or interaction.

Unlike static snapshots, FairScore evolves with you. A user starting at a baseline might climb Web3 reputation tiers through consistent DeFi participation, unlocking perks like priority in token allocations or ICO gating. FairScale’s design ensures privacy, using aggregated data without exposing personal details. This makes it ideal for Solana’s DeFi ecosystem, where protocols integrate it seamlessly to gate high-value activities. Check out deeper dives on how such systems power lending at Crypto Credit Scores.

It also looks at social data from X. This includes post https://t.co/ArjL6KnAfV

Inactivity or predominantly extractive patterns lead to gradual declines.

This structure incentivizes consistent contribution rather than isolated or https://t.co/nPhmj97PVL

Users connect a Solana wallet and X account to generate and view their FairScore. Over 13,000 scores have been generated, with new users onboarding daily.

The dashboard presents the current FairScore, along with badges https://t.co/YUvXJd7siY

To begin, visit https://t.co/lGacb2pkZI https://t.co/C94r0hDTWK

How FairScore Supercharges Borrowing Without Collateral

Integration is straightforward yet profound. A Solana lending protocol queries a user’s FairScore via API, receiving a trustworthiness index from 0-1000. High scorers (say, 800 and ) qualify for reduced collateral, perhaps 110% instead of 200%, or even uncollateralized lines for flash loans and recurring needs. This mirrors emerging models from Huma Finance and Mitosis, but FairScore’s Solana optimization delivers sub-second assessments.

Consider a yield farmer with a solid history. Their score signals low default risk, so the protocol boosts limits automatically. Lenders win with better utilization; borrowers gain freedom. To improve crypto credit score via FairScore, focus on on-chain hygiene: avoid rugs, honor borrows, engage genuinely. It’s patient building, yielding exponential returns as tiers unlock.

Real-world integrations on Solana are already proving this out. Protocols leveraging FairScore on-chain reputation report utilization rates climbing 30-50% as trusted borrowers tap larger pools without excess lockup. Imagine deploying capital across multiple farms or launches, all gated by your proven track record rather than static holdings. This isn’t theory; it’s live on high-throughput chains like Solana, where speed amplifies the edge.

Traditional Overcollateralized DeFi Loans vs. FairScore Reputation-Based Borrowing

| Collateral Ratio | Borrowing Limit Example ($10K loan) | Capital Efficiency | Default Risk Mitigation | |

|---|---|---|---|---|

| Traditional | 200% | $5K usable | Low | Volatility buffers |

| FairScore High Score | 110% or 0% | $9K usable | High | Behavioral data |

Such shifts demand robust mechanics. FairScore employs weighted algorithms: 40% on-chain repayments, 30% liquidity interactions, 20% social proofs, 10% off-chain KYC-lite signals. Scores tier into bronze, silver, gold, platinum brackets, each unlocking progressive perks like Solana borrowing limits from 1.2x to fully uncollateralized for elite users. Protocols set thresholds dynamically, often tying them to market volatility indices akin to those proposed in Bankless analyses, a DeFi LIBOR for reputation pricing.

Building Your FairScore: Practical Steps to Unlock Limits

Patience pays in reputation markets, much like compounding in legacy finance. Users climbing tiers see borrowing power scale exponentially, but it starts with deliberate actions. I’ve seen parallels in commodity cycles, where consistent performers outlast speculators. Here’s how to methodically elevate your profile.

Boost Your FairScore: 5 Steps to Unlock Higher DeFi Borrowing Limits on Solana

Once elevated, the flywheel spins: higher scores mean more access, reinforcing good habits. DeFi platforms from Solana Compass listings are embedding these checks, cross-chain collateral notwithstanding. Voices like Mary Gooneratne on Lightspeed podcasts underscore Solana’s lending edge, now supercharged by reputation layers reducing manipulation risks flagged by GARP.

Challenges remain, of course. Sybil attacks or data silos could undermine trust, but FairScale counters with zero-knowledge proofs and oracle diversity. Privacy stays paramount, no granular exposures, just aggregate trust signals. This aligns with Zama’s confidential lending vision, blending uncollateralized access with on-chain security. For lenders, it’s risk repricing: default probabilities drop 70% for top-tier scorers per Mitosis models, enabling bolder markets.

Sources like Huma Finance note emerging uncollateralized paths via decentralized reputation, FairScore embodies this on Solana, onboarding trillions by freeing locked capital.

Looking ahead to 2026, expect FairScore integrations across major protocols, standardizing Web3 reputation tiers much like credit bureaus standardized TradFi. Retail users gain parity with institutions; DeFi scales beyond whales. If you’re farming yields or building dApps, start nurturing your score today. It’s the patient path to capital sovereignty in a collateral-free era. Explore related insights on on-chain reputation powering DeFi loans or reputation’s lending influence.