Decentralized finance (DeFi) has long promised open access to financial tools, yet its lending markets have been hamstrung by overcollateralization requirements. For most users, borrowing in DeFi means locking up more assets than they receive – a system that restricts capital efficiency and excludes millions who lack substantial crypto holdings. Now, the emergence of on-chain credit scores is rewriting the rules, paving the way for undercollateralized lending and unlocking new opportunities across the decentralized economy.

Why Overcollateralization Limits DeFi’s Potential

Overcollateralization has been DeFi’s answer to trustless lending: deposit $1,000 worth of ETH, borrow $600 in stablecoins. This model protects lenders from default but leaves borrowers with poor capital utilization and makes DeFi inaccessible for those without hefty portfolios. The result? Billions in idle assets and a market that can’t compete with the flexibility of traditional finance.

The next wave of DeFi growth hinges on breaking these barriers. As highlighted by Onchain’s recent research, on-chain credit scores could bring trillions of dollars into DeFi, attracting both retail and institutional participants who demand more efficient credit markets.

The Mechanics of On-Chain Credit Scoring

An on-chain credit score is an algorithmic measure of a wallet’s financial reliability based entirely on blockchain data. Every transaction, loan repayment, yield farming activity, or participation in governance becomes part of a transparent credit history. Protocols analyze this data to assess:

- Repayment behavior: Has the borrower consistently repaid loans on time?

- Diversification: Does the wallet interact with multiple protocols or stick to one?

- Risk appetite: Are there signs of reckless leverage or frequent liquidations?

- Total value transacted: How much capital has flowed through this address?

This approach replaces opaque credit checks with transparent, objective measures accessible to anyone on-chain. Projects like Credora and Huma Finance are pioneering these systems – their protocols ingest real-time blockchain data and generate dynamic risk profiles that lenders can use to offer loans with reduced collateral requirements.

New Tools for Trust: Reputation Tokens and Hybrid Models

The innovation doesn’t stop at raw transaction analysis. Some protocols are introducing non-transferable reputation tokens – often called Soulbound Tokens (SBTs) – which serve as proof of a user’s trustworthiness within the ecosystem. These tokens are permanently linked to a specific wallet address and can encode achievements like successful loan repayments or protocol participation.

This creates a portable blockchain reputation system that can be referenced across multiple platforms, reducing friction for borrowers seeking undercollateralized loans elsewhere in DeFi.

Meanwhile, hybrid models are bridging Web2 and Web3 by incorporating off-chain data such as traditional credit scores or KYC attestations via decentralized oracle networks. This fusion allows protocols to capture both on-chain behavior and real-world financial reliability – broadening access while maintaining transparency.

The Road Ahead: Challenges and Opportunities

The promise is enormous but so are the hurdles. Privacy remains a top concern; while all blockchain activity is public, sensitive personal information must be protected without undermining transparency. Standardizing scoring methodologies is another challenge – without universal benchmarks, it’s hard for lenders to compare risk across platforms.

Despite these obstacles, one thing is clear: as on-chain credit assessment matures, undercollateralized DeFi lending will become not just possible but practical – opening doors for new users and unleashing capital that has long sat idle behind collateral walls.

Forward-thinking DeFi protocols are already piloting these systems, and the results are promising. Borrowers with strong on-chain credit scores can now access loans with minimal or even zero collateral, while lenders gain confidence from transparent, data-driven risk models. This shift is laying the groundwork for a truly open financial ecosystem where trust is algorithmic and opportunity is accessible.

Top Platforms Pioneering Undercollateralized DeFi Lending

-

Credora – A leader in on-chain credit assessment, Credora enables undercollateralized lending by providing transparent credit scores based on users’ blockchain activity and financial behavior.

-

Clearpool – This decentralized credit marketplace offers unsecured institutional lending powered by on-chain credit risk analysis, allowing trusted borrowers to access capital without heavy collateral requirements.

-

Goldfinch – Goldfinch brings real-world undercollateralized lending to DeFi, using both on-chain and off-chain data to assess borrower creditworthiness and expand access to capital globally.

-

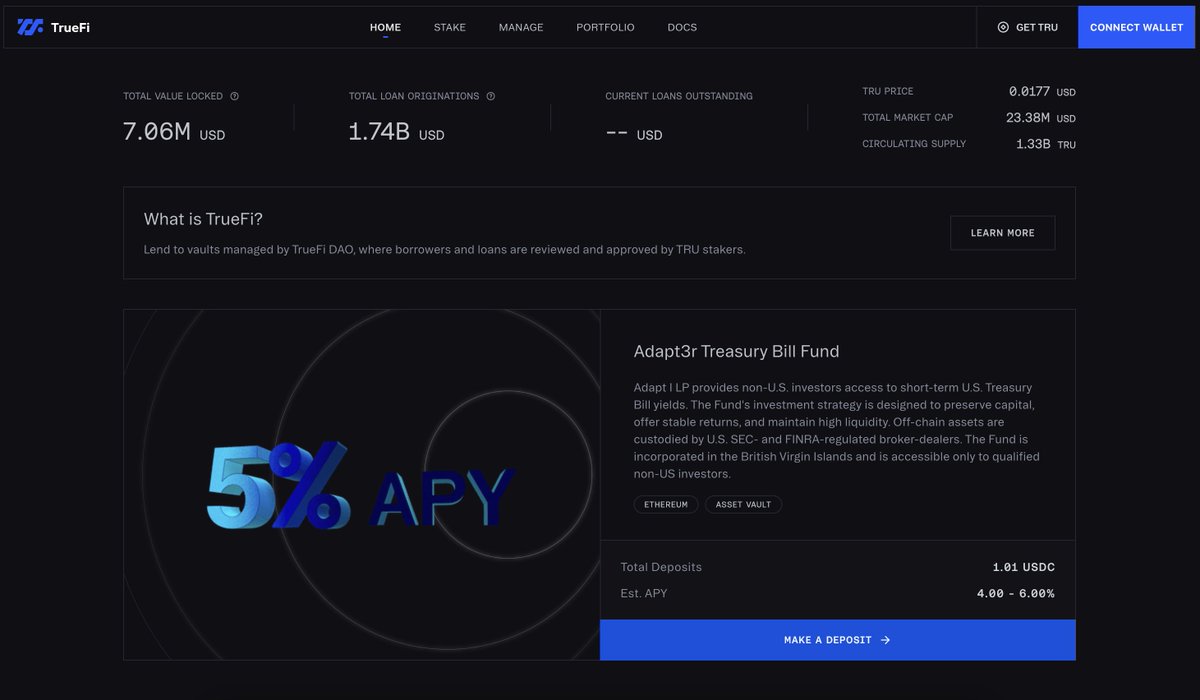

TrueFi – TrueFi pioneered unsecured lending pools in DeFi, leveraging on-chain credit scoring and community governance to vet borrowers and manage risk transparently.

-

Arcadia Finance – Arcadia integrates on-chain credit scores and soulbound reputation tokens to facilitate undercollateralized loans, focusing on composable credit and transparent borrower profiles.

Beyond individual lending, the ripple effects extend to the broader crypto economy. As more users build verifiable reputations through consistent on-chain behavior, network effects kick in: protocols can collaborate on shared reputation standards, secondary markets for credit risk emerge, and institutional capital finds new avenues for participation. The endgame? A DeFi landscape that rivals traditional finance in both efficiency and inclusivity.

What’s Next for On-Chain Credit Scores?

The evolution of decentralized credit protocols will depend on a few key factors:

- Interoperability: Seamless reputation portability across blockchains and platforms will be vital. Imagine earning your credit score on one protocol and instantly qualifying for undercollateralized loans elsewhere.

- Privacy-Preserving Tech: Zero-knowledge proofs and related innovations could allow users to share proof of good credit without exposing every detail of their financial history.

- Community Governance: As these systems grow, decentralized governance will play a crucial role in setting standards, updating risk models, and ensuring fair access.

This momentum is already attracting attention from both crypto-native builders and traditional financial institutions seeking to bridge into Web3. The result? A flywheel of innovation that promises to unlock trillions in untapped value for borrowers, lenders, and the entire DeFi ecosystem.

If you’re ready to explore how your own blockchain activity could unlock new opportunities – or if you want to understand more about the mechanics behind these emerging systems – dive deeper with our comprehensive guide: How On-Chain Credit Scores Enable Undercollateralized Lending in DeFi.