Decentralized finance (DeFi) has long been constrained by its reliance on overcollateralized lending models. Borrowers have typically needed to lock up more value in crypto assets than they receive in loans, a system that, while effective at mitigating risk, severely limits capital efficiency and excludes users without substantial digital holdings. Today, the emergence of on-chain credit scoring is transforming this paradigm by enabling undercollateralized crypto loans, an innovation poised to unlock trillions of dollars for the DeFi ecosystem.

From Overcollateralization to Credit-Based Lending

The traditional DeFi lending model, epitomized by protocols like Aave and Compound, requires borrowers to deposit collateral worth more than their loan amount. This mechanism is straightforward: if a borrower defaults, the protocol liquidates the collateral to cover losses. While effective for risk management, it creates a high barrier to entry and leaves vast pools of untapped liquidity.

On-chain credit scores offer a fundamentally different approach. By leveraging transparent blockchain data, transaction history, repayment records, protocol interactions, these scores quantify a user’s creditworthiness directly on-chain. Lenders can thus extend loans with reduced or even zero collateral requirements to borrowers with strong on-chain reputations. This shift not only improves capital efficiency but also democratizes access to DeFi lending markets.

The Mechanics of On-Chain Credit Scoring

An on-chain credit score aggregates multiple data points from a user’s blockchain activity:

- Repayment history: Timely repayments across various protocols signal reliability.

- Wallet longevity: Older addresses with consistent activity are generally less risky.

- Diversity of protocol usage: Interacting with multiple reputable platforms indicates higher engagement and trustworthiness.

- Liquidation events: Frequent liquidations lower a user’s score as they suggest poor risk management.

This data-driven assessment enables real-time, dynamic credit scoring that is both transparent and privacy-preserving. Unlike traditional credit bureaus that rely on opaque algorithms and off-chain reporting, on-chain systems allow anyone to verify the underlying data without exposing sensitive personal information.

Pioneering Protocols in Undercollateralized Lending

A new generation of DeFi protocols is integrating on-chain credit scores into their underwriting processes. For instance:

- 3Jane Protocol: Operating on Ethereum, 3Jane provides unsecured lines of credit based on verifiable proofs of both crypto and bank assets as well as future cash flows. The platform leverages models from Cred Protocol and Blockchain Bureau for scalable risk-adjusted underwriting.

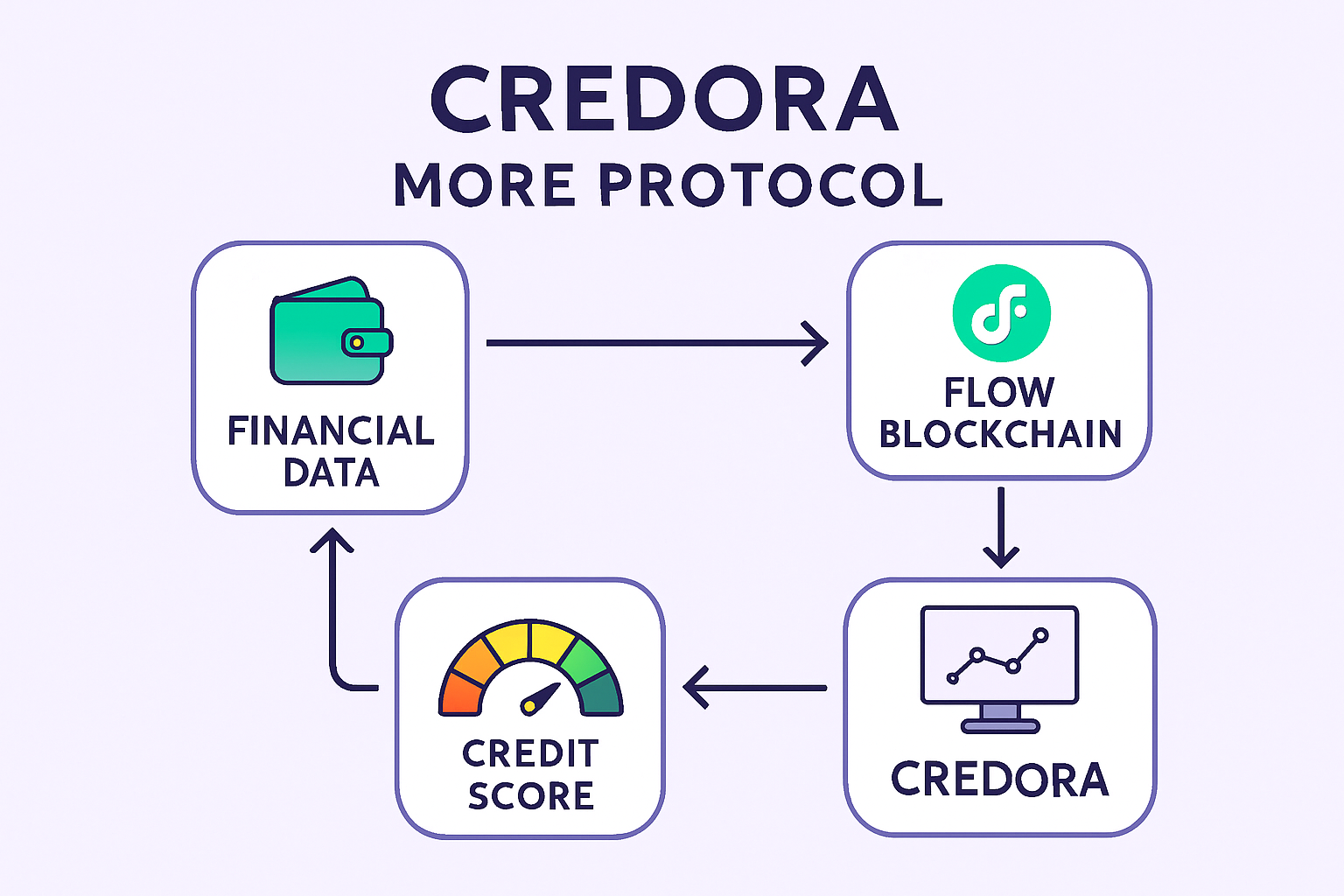

- Credora and More Protocol (Flow Blockchain): This partnership allows users to borrow up to 200% of their posted collateral using Credora’s real-time on-chain credit assessments, an unprecedented leap in capital efficiency within DeFi lending markets.

- MetisDAO: By utilizing Soulbound Tokens (SBTs), MetisDAO enables users to build an immutable reputation tied directly to their wallet address. This reputation layer empowers lenders to evaluate borrower histories without requiring excessive collateralization.

- Seamless Protocol (Base): Launched on Coinbase’s layer-2 solution Base, Seamless restricts borrowing privileges to authorized smart contracts or vaults, minimizing risk while facilitating undercollateralized borrowing for vetted participants.

The integration of these mechanisms is already catalyzing a shift away from overcollateralization toward more nuanced risk assessment models based on actual user behavior, not just asset balances.

Protocols deploying on-chain credit scoring are not only increasing capital efficiency but also broadening participation in decentralized finance. By removing the need for excessive collateral, these systems lower the entry barrier, allowing a wider demographic to access credit and liquidity. This is especially impactful for users in regions where traditional financial infrastructure is limited or where individuals lack established off-chain credit histories.

Risk Management and Incentive Design

While undercollateralized crypto loans introduce new opportunities, they also require sophisticated DeFi risk management. Protocols must balance inclusivity with protection against defaults. This is achieved through multi-layered risk frameworks that incorporate:

- Dynamic interest rates that adjust based on a borrower’s on-chain reputation and market conditions.

- Automated risk monitoring via smart contracts that flag or restrict borrowing for addresses with deteriorating credit scores.

- Staking mechanisms, where protocol participants backstop loan pools and share in both rewards and risks.

The result is a more resilient lending ecosystem where incentives are aligned for both lenders and borrowers. As protocols like Credora, 3Jane, and MetisDAO continue to refine their models, we’re witnessing the emergence of decentralized credit bureaus, entities that operate transparently, preserve user privacy, and foster trust across the Web3 landscape.

Top On-Chain Credit Scoring Protocols Powering Undercollateralized DeFi Loans

-

3Jane Protocol: A pioneering credit-based money market on Ethereum, 3Jane underwrites unsecured lines of credit using verifiable proofs of crypto and bank assets, future cash flows, and on-chain credit scores. It integrates scoring models from Cred Protocol and Blockchain Bureau for risk-adjusted lending at scale. Learn more.

-

Credora & More Protocol: Through a strategic partnership, Credora and More Protocol have introduced on-chain credit scoring to the Flow Blockchain. This enables borrowers on MORE Markets to access undercollateralized loans—up to 200% of their collateral—using Credora’s real-time credit scores. Read the announcement.

-

MetisDAO: By leveraging Soulbound Tokens (SBTs) for on-chain identity, MetisDAO allows users to build credit histories directly on-chain. This reputation system empowers lenders to assess creditworthiness, facilitating undercollateralized lending within the Metis ecosystem. Explore MetisDAO’s approach.

-

Seamless Protocol: Operating on Coinbase’s Base layer-2, Seamless Protocol offers an undercollateralized borrowing market using Integrated Liquidity Markets. Only authorized smart contracts or vaults can borrow, reducing risk for liquidity providers while enabling efficient undercollateralized lending. See Seamless Protocol in action.

The Road Ahead: Challenges and Opportunities

Despite rapid progress, several hurdles remain before undercollateralized lending reaches mainstream adoption. Key challenges include:

- Sybil resistance: Preventing users from gaming the system via multiple wallets remains an open technical problem. Solutions such as Soulbound Tokens (SBTs) and decentralized identity standards are promising but require further adoption.

- Data interoperability: Seamless aggregation of cross-chain activity is essential for holistic credit assessments. Ongoing innovation in oracle networks and data bridges will be crucial here.

- Regulatory clarity: As DeFi platforms begin to resemble traditional lenders in function, compliance requirements may evolve rapidly. Protocols must be agile to adapt while maintaining decentralization principles.

The upside is enormous: as more protocols integrate verifiable on-chain reputation systems, DeFi can unlock vast pools of idle capital currently sidelined by overcollateralization requirements. This transition has the potential to bring trillions of dollars into decentralized markets over the next decade, fueling innovation far beyond simple lending, think insurance, real-world asset financing, even payroll advances built atop transparent blockchain rails.

If you want a deeper dive into how DeFi protocols are leveraging these innovations to enable secure undercollateralized crypto lending at scale, read our detailed analysis at Crypto Credit Scores: How On-Chain Risk Scores Enable Under-Collateralized Crypto Loans.

A New Era for DeFi Credit Reputation

The evolution from asset-based to reputation-based lending marks a pivotal shift in blockchain finance. On-chain credit scoring not only enhances transparency but also ensures privacy preservation, a combination rarely achieved by legacy financial systems. As adoption grows and technical standards mature, expect to see an increasingly robust ecosystem where your digital footprint unlocks real economic opportunity, no matter your starting balance.