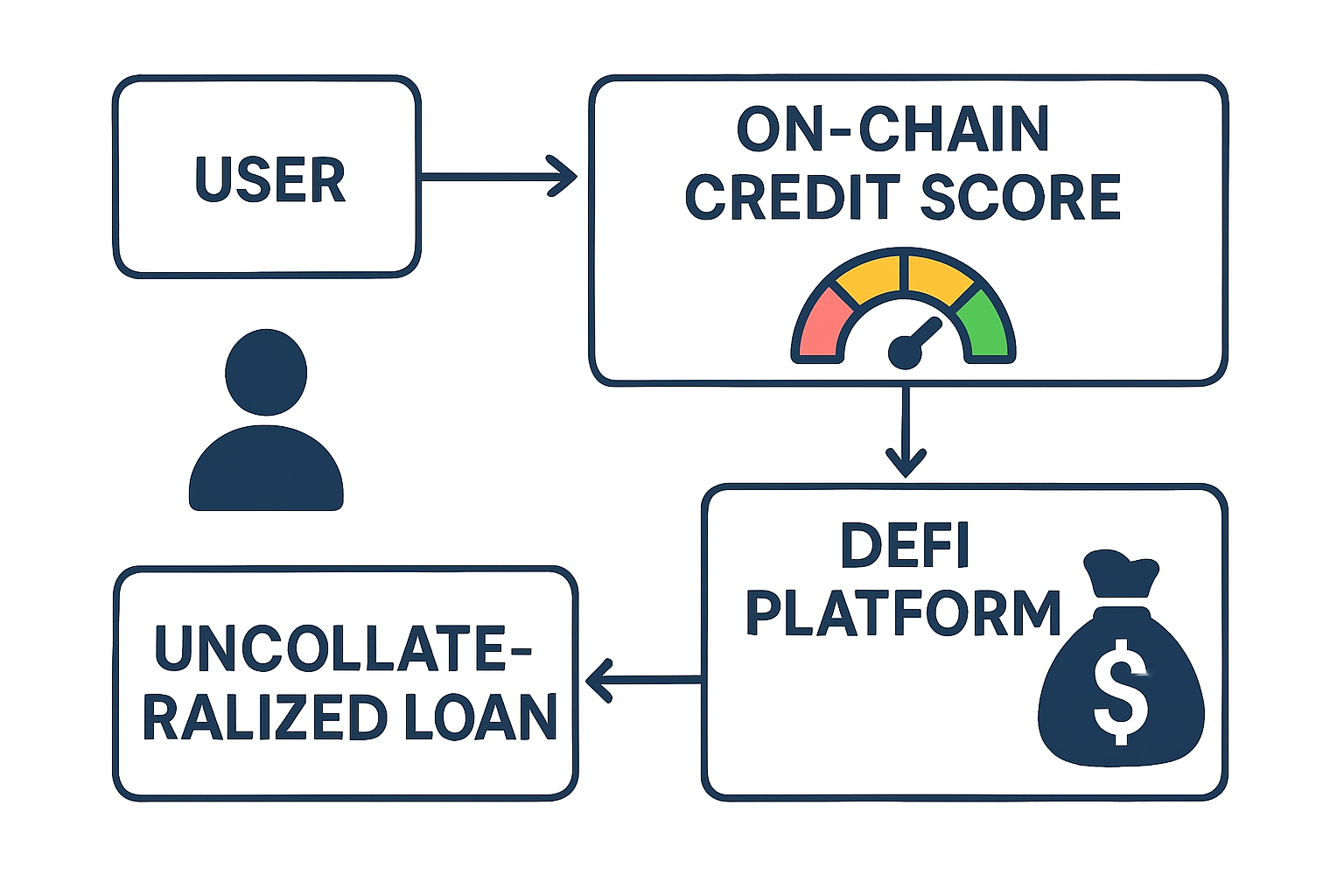

For years, the promise of decentralized finance (DeFi) has been shadowed by a fundamental limitation: access to lending has required users to over-collateralize, often locking up more value than they receive as a loan. This approach, while effective at mitigating protocol risk, creates an artificial barrier that excludes millions who lack substantial crypto holdings. The emergence of on-chain credit scores is poised to flip this paradigm, empowering DeFi users to access uncollateralized or under-collateralized loans based on their blockchain credit history rather than their wallet balance.

Why Over-Collateralization Holds DeFi Back

Traditional DeFi lending protocols like Aave and Compound require borrowers to deposit assets worth more than the loan amount, often with collateralization ratios as high as 150%. This model, while necessary in the absence of reliable identity and credit assessment, is inherently capital-inefficient. Users with solid repayment histories or active blockchain participation are treated the same as brand new wallets, stifling both financial inclusion and protocol growth.

Consider this: In traditional banking, your credit score unlocks unsecured credit cards and personal loans. In DeFi, until recently, your only option was to lock up more than you borrow. The result? Billions in dormant capital and a DeFi ecosystem unable to serve the next wave of users. As recent research from Visa and Mitosis University highlights, unlocking DeFi uncollateralized loans could bring trillions of dollars in new liquidity to the space.

How On-Chain Credit Scores Work

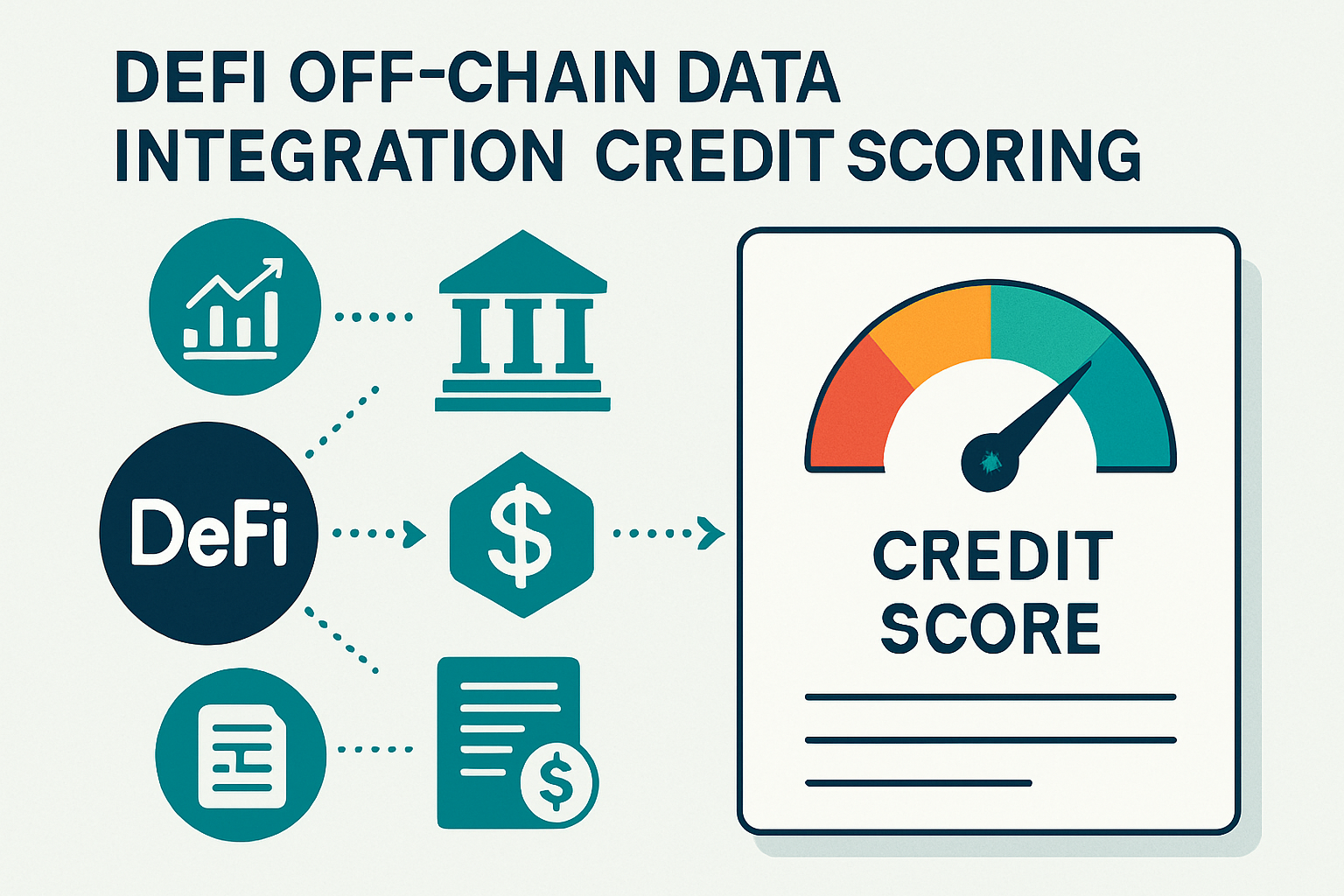

On-chain credit scoring protocols like Cred Protocol, AlphaLine, Spectral Finance, and 3Jane are pioneering new ways to assess decentralized lending risk. Instead of relying on opaque, centralized data, these systems analyze transparent blockchain activity to build a blockchain credit assessment tailored to each user. Key data points include:

Key Data Points in On-Chain Credit Scoring

-

Transaction History: Comprehensive record of all on-chain transactions, including transfers, swaps, and contract interactions, used to assess financial activity and behavior.

-

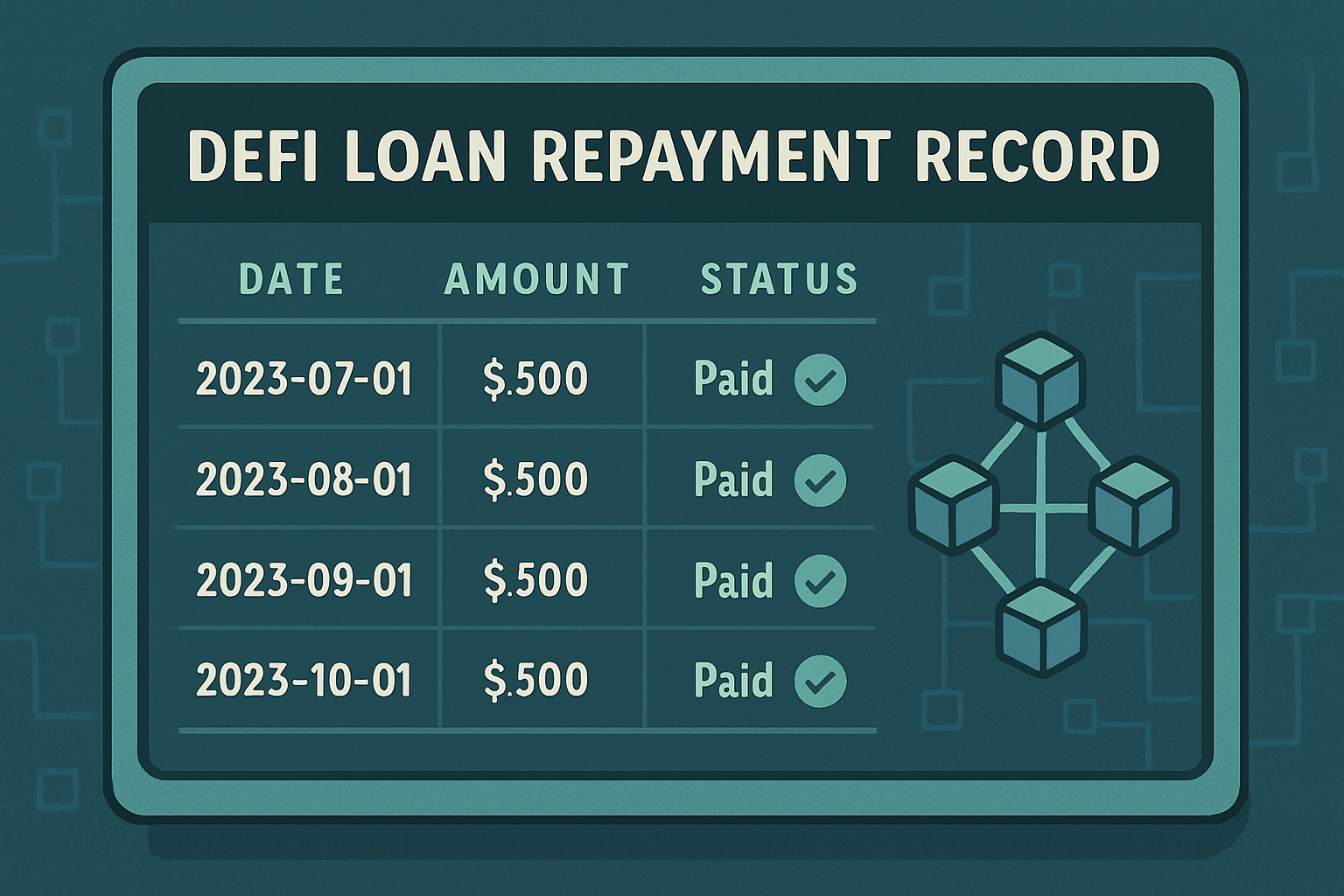

Loan Repayment Records: Detailed history of past DeFi loan repayments, defaults, and punctuality, providing evidence of a user’s reliability as a borrower.

-

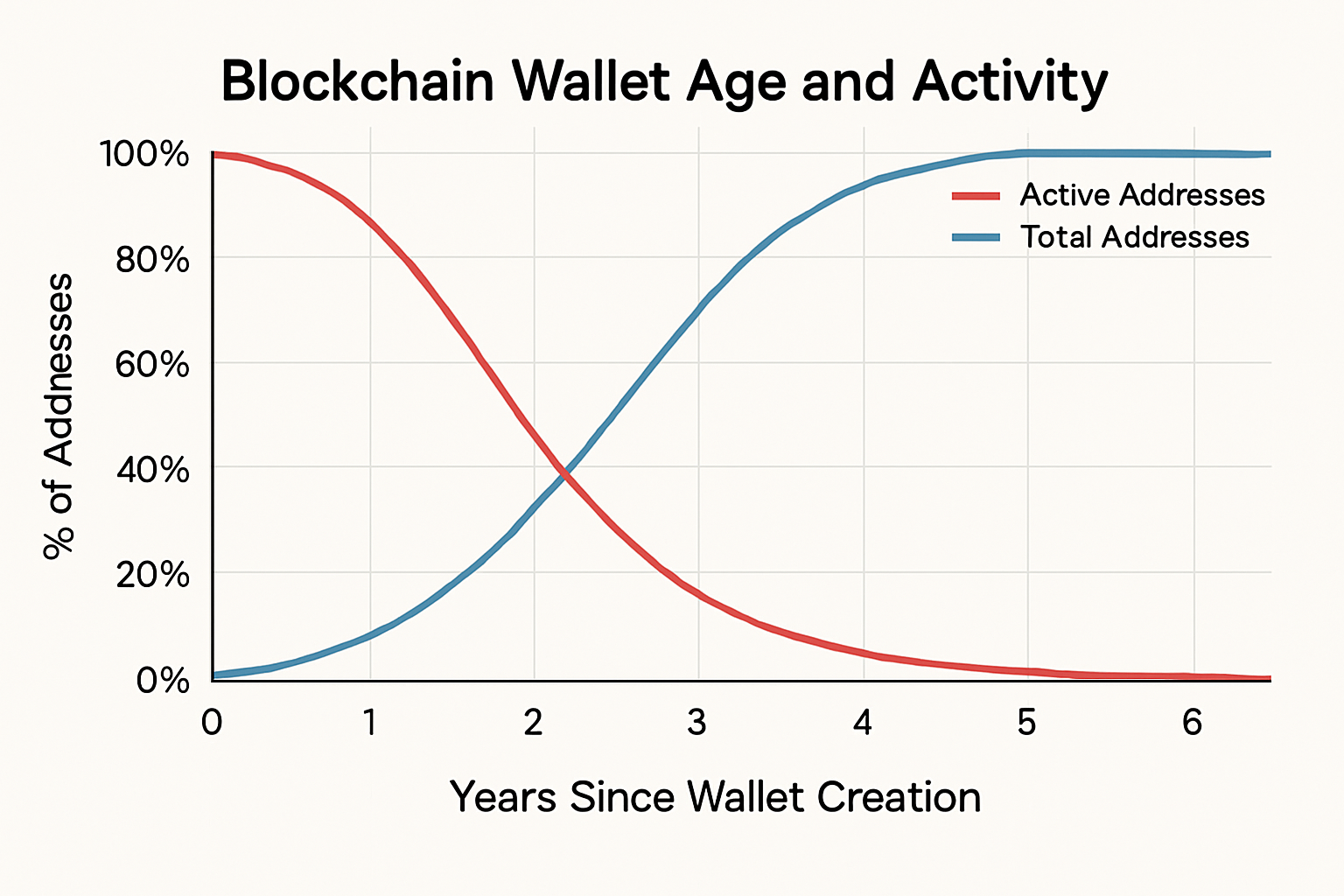

Wallet Age and Activity: The length of time a wallet has been active and the frequency of its use, indicating stability and long-term engagement in the ecosystem.

-

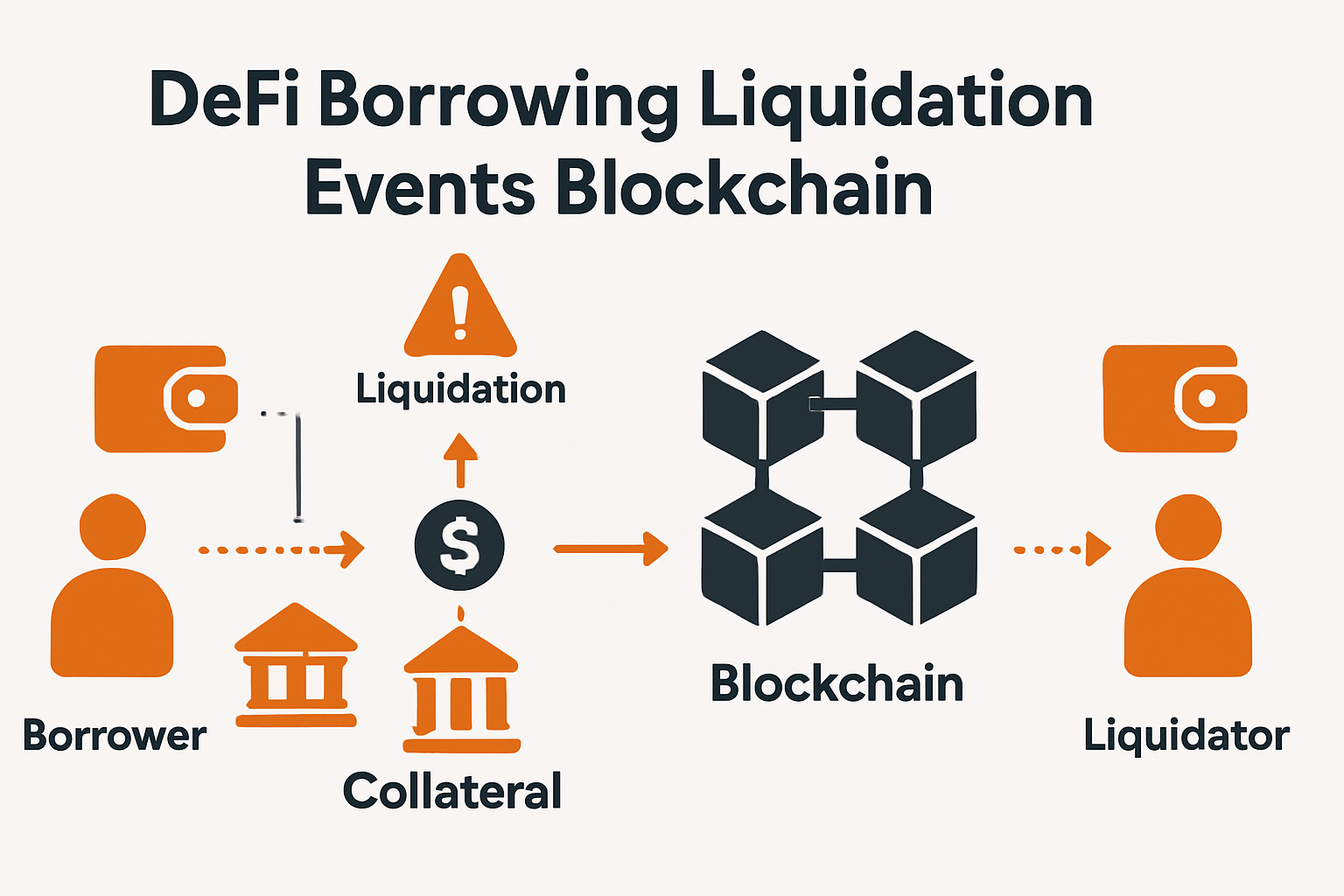

Borrowing and Liquidation Events: Analysis of previous borrowing activity and any liquidation events, as tracked by protocols like Spectral Finance through their MACRO score.

-

On-Chain Asset Holdings: Assessment of current and historical balances of cryptocurrencies and tokens held in the wallet, reflecting financial strength and diversification.

-

Interaction with DeFi Protocols: Evaluation of engagement with established DeFi platforms (e.g., Aave, Compound), which can signal trustworthiness and experience.

-

Participation in Governance: Involvement in protocol governance votes or DAO activities, suggesting commitment and reputation within the community.

-

Off-Chain Data Integration: For protocols like 3Jane, verifiable off-chain data such as bank balances and income may be incorporated to enhance credit assessment.

Protocols use advanced analytics and machine learning to weigh these factors and generate a dynamic score. For example, Spectral’s MACRO score incorporates multi-asset transaction data and liquidation events, while 3Jane factors in both on-chain and off-chain data like verified bank balances, without compromising privacy thanks to zero-knowledge proofs.

“On-chain credit scoring is about more than just lending, it’s about trust, reputation, and unlocking capital for everyone in the decentralized economy. ”

The Real-World Impact: From Exclusion to Inclusion

The practical effect of on-chain credit scores is profound. Users who previously couldn’t access loans due to lack of collateral can now leverage their crypto credit history to secure funds. This shift is especially significant for users in emerging markets and for crypto-native entrepreneurs with rich on-chain activity but limited fiat assets.

Protocols like 3Jane now offer unsecured USDC credit lines using verifiable on-chain and off-chain data, while AlphaLine dynamically adjusts interest rates based on a borrower’s real-time risk profile. The result? More inclusive and efficient lending markets, with risk managed transparently and algorithmically rather than through blunt collateral requirements.

Key Players and Protocol Innovations

The field is rapidly evolving. Here are some of the most important platforms shaping the landscape:

Top DeFi Protocols Offering Uncollateralized Loans via On-Chain Credit Scores

-

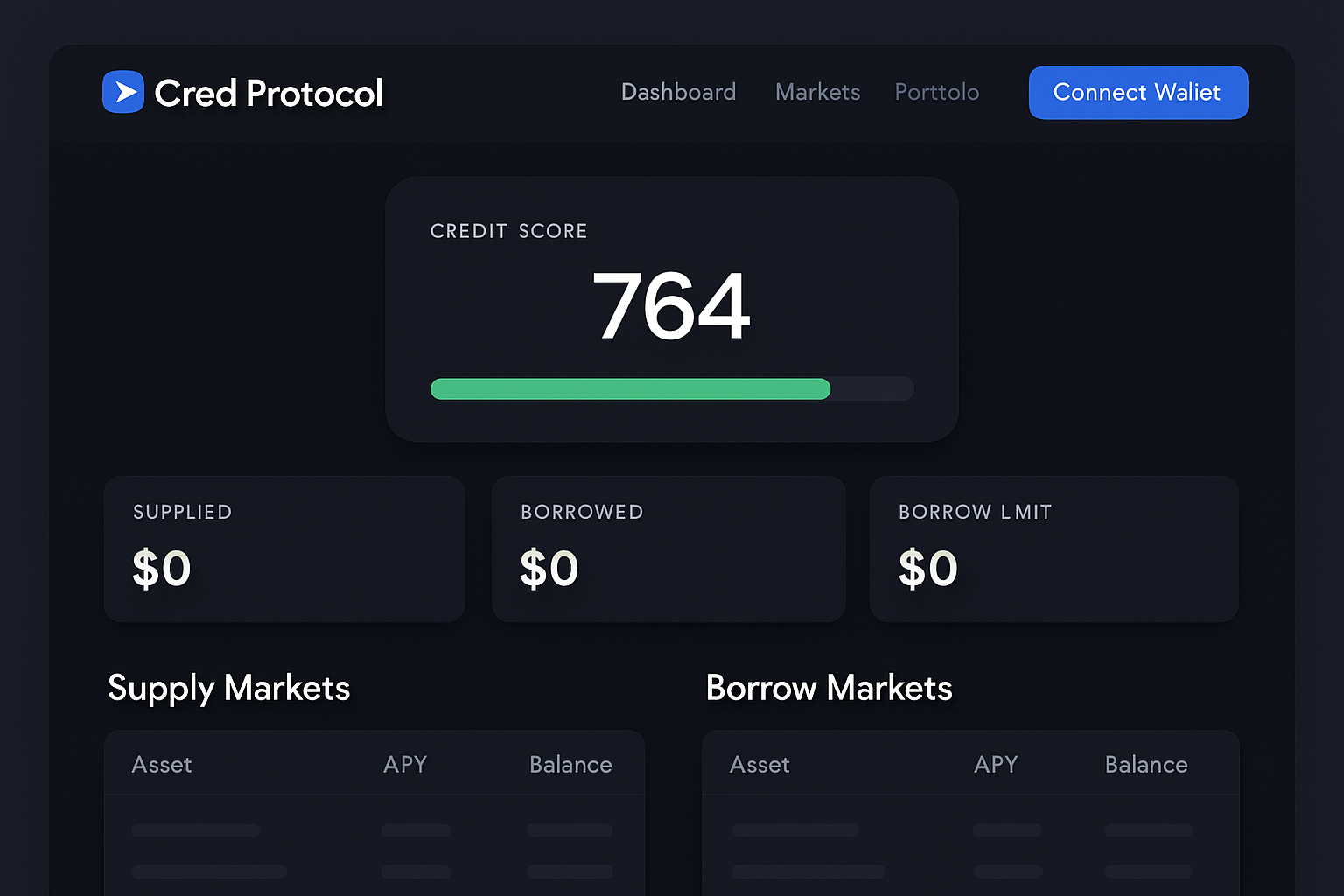

Cred Protocol: Cred Protocol quantifies on-chain lending risk by developing decentralized credit scores. Its system analyzes a user’s blockchain activity—including transaction history and loan repayments—to assess creditworthiness, enabling access to uncollateralized loans for a broader range of DeFi users. Learn more

-

3Jane Protocol: Launched in early 2025, 3Jane offers unsecured USDC credit lines by evaluating both on-chain and off-chain data, such as bank balances and income. The protocol leverages zero-knowledge privacy technology and provides instant lending decisions based on a comprehensive credit assessment. Explore 3Jane

-

AlphaLine Protocol: AlphaLine introduces dynamic on-chain credit scores by analyzing transaction history, collateral, and repayment behavior. The platform facilitates under-collateralized loans with interest rates that adjust in real time according to the borrower’s evolving credit profile. See AlphaLine details

-

Spectral Finance: Spectral utilizes its Multi-Asset Credit Risk Oracle (MACRO) score, which aggregates on-chain data like borrowing history and liquidation events. This credit score helps lenders assess risk and enables borrowers to access uncollateralized loans based on their on-chain reputation. Discover Spectral

Each protocol brings a unique approach to privacy, data integration, and risk assessment. For a deeper dive into how these systems work and their impact on DeFi lending, see this guide on how on-chain risk scores enable under-collateralized lending in DeFi.

As these credit scoring systems mature, they are fundamentally altering the risk calculus for both lenders and borrowers. Lenders can now differentiate between high- and low-risk borrowers on-chain, enabling more competitive rates and tailored loan products. Borrowers, in turn, gain access to capital without sacrificing liquidity or exposing themselves to unnecessary liquidation risk. This dynamic creates a virtuous cycle: as more users build positive blockchain credit assessments, protocols can safely expand uncollateralized lending volumes.

Transparency remains at the heart of this evolution. Unlike traditional credit bureaus, where algorithms are hidden and data is siloed, on-chain credit scores are auditable, interoperable, and resistant to tampering. Users maintain sovereignty over their financial identity, often leveraging privacy-preserving technologies like zero-knowledge proofs to share only what’s necessary for credit evaluation.

Challenges and Next Steps

Despite rapid progress, several challenges must be addressed before DeFi uncollateralized loans reach mainstream scale:

- Sybil resistance: Preventing users from gaming the system with multiple wallets remains a technical hurdle.

- Data integration: Combining on-chain and off-chain data (such as income or employment verification) while preserving privacy is still an active area of research.

- Regulatory uncertainty: As DeFi lending becomes more sophisticated, protocols must navigate evolving legal frameworks around identity, privacy, and consumer protection.

The industry is responding with creative solutions. Zero-knowledge attestations allow users to prove aspects of their identity or credit history without revealing sensitive details. AI-powered analytics improve risk modeling by detecting patterns invisible to manual review. And new governance models give communities a say in how credit policies evolve over time.

What This Means for DeFi Users

The implications for everyday users are profound. No longer must individuals rely solely on their asset holdings to participate in decentralized lending markets. Instead, they can build a portable crypto credit history, unlocking better terms as their reputation grows across protocols. For entrepreneurs and small businesses operating on-chain, this could mean access to working capital that was previously out of reach.

The next wave of innovation will focus on making these systems even more user-friendly, abstracting away complexity so that anyone can benefit from decentralized finance without deep technical knowledge. Expect to see wallets integrating real-time credit dashboards, automated borrowing suggestions based on your score, and seamless cross-protocol lending experiences.

How to Get Started Building Your On-Chain Credit Score

Practical Tips to Build Your On-Chain Credit History

-

Maintain a Consistent Repayment Record: Timely repayment of DeFi loans on platforms like Cred Protocol and 3Jane Protocol is crucial. Your on-chain credit score heavily weighs your loan repayment history, so avoid late payments or defaults.

-

Engage Regularly with Reputable DeFi Platforms: Use well-established protocols such as Cred Protocol, AlphaLine Protocol, and Spectral Finance to build a diverse and verifiable on-chain transaction history. Frequent, responsible activity across multiple platforms strengthens your credit profile.

-

Link Off-Chain Financial Data Where Supported: Some protocols, such as 3Jane Protocol, allow users to verify off-chain data like bank balances or income. Connecting these data sources can boost your creditworthiness and unlock larger or unsecured credit lines.

-

Monitor and Improve Your On-Chain Credit Score: Regularly check your credit score on platforms like Spectral Finance (MACRO score) or Cred Protocol. Understand the factors affecting your score and take proactive steps—such as increasing transaction volume or improving repayment consistency—to enhance your profile.

If you’re ready to explore these opportunities yourself, or want to understand how your blockchain activity might impact your borrowing power, check out our comprehensive resource: How On-Chain Credit Scores Enable Undercollateralized Crypto Loans: A Practical Guide for DeFi Users.

The rise of transparent, decentralized credit scoring is not just a technical milestone but a cultural one. It signals a shift toward an open financial system where trust is algorithmic yet personal, rooted not in legacy institutions but in the collective history we write together on-chain. As adoption accelerates, expect trillions in new value, and millions of new participants, to flow into DeFi’s expanding universe.