Decentralized Finance (DeFi) has always promised a more open, borderless financial system. But until recently, DeFi lending protocols have been hamstrung by a fundamental problem: the need for over-collateralization. Borrowers often have to lock up assets worth more than their loan, limiting both capital efficiency and access for those without deep crypto pockets. Now, on-chain credit scores are rewriting the rules, unlocking new liquidity, and expanding financial inclusion across the blockchain landscape.

The Shift from Collateral to Creditworthiness

Traditional finance relies on credit bureaus to gauge borrower risk. In DeFi, this was impossible, until blockchain analytics evolved. Today’s blockchain credit assessment tools analyze users’ transaction histories, protocol interactions, and wallet behaviors to generate transparent, privacy-preserving crypto credit scores. These scores empower lenders to offer under-collateralized or even unsecured loans, something that was unthinkable just a few years ago.

This shift is more than technical; it’s transformative. Platforms like Credora, RociFi, Spectral, and Cred Protocol are at the forefront of this movement:

Leading Platforms Driving On-Chain Credit Scoring in DeFi

-

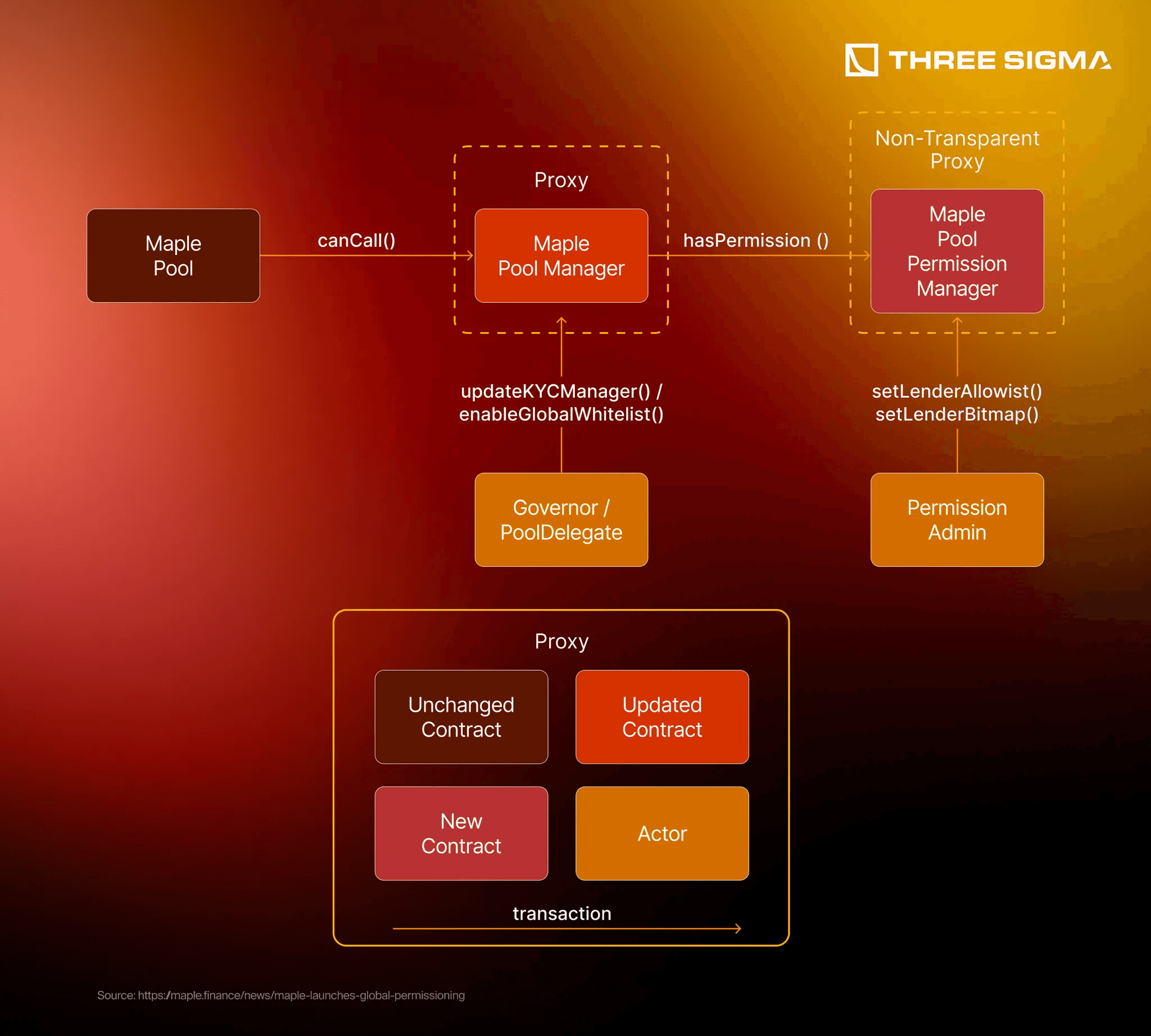

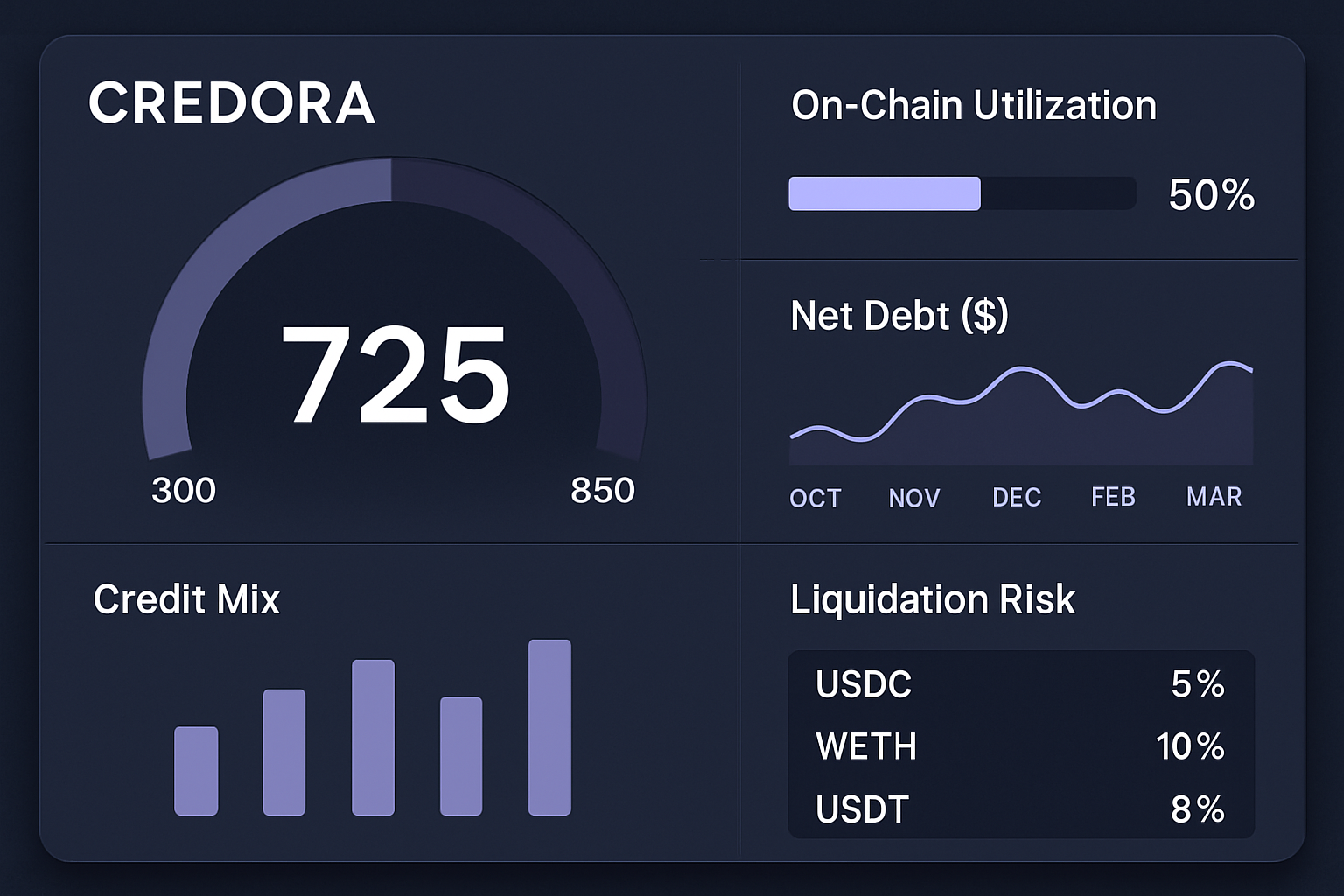

Credora: Launched on-chain credit scores in July 2024, empowering DeFi lenders and borrowers with transparent, real-time risk assessments. By partnering with multiple protocols, Credora enhances capital efficiency and trust across the ecosystem.

-

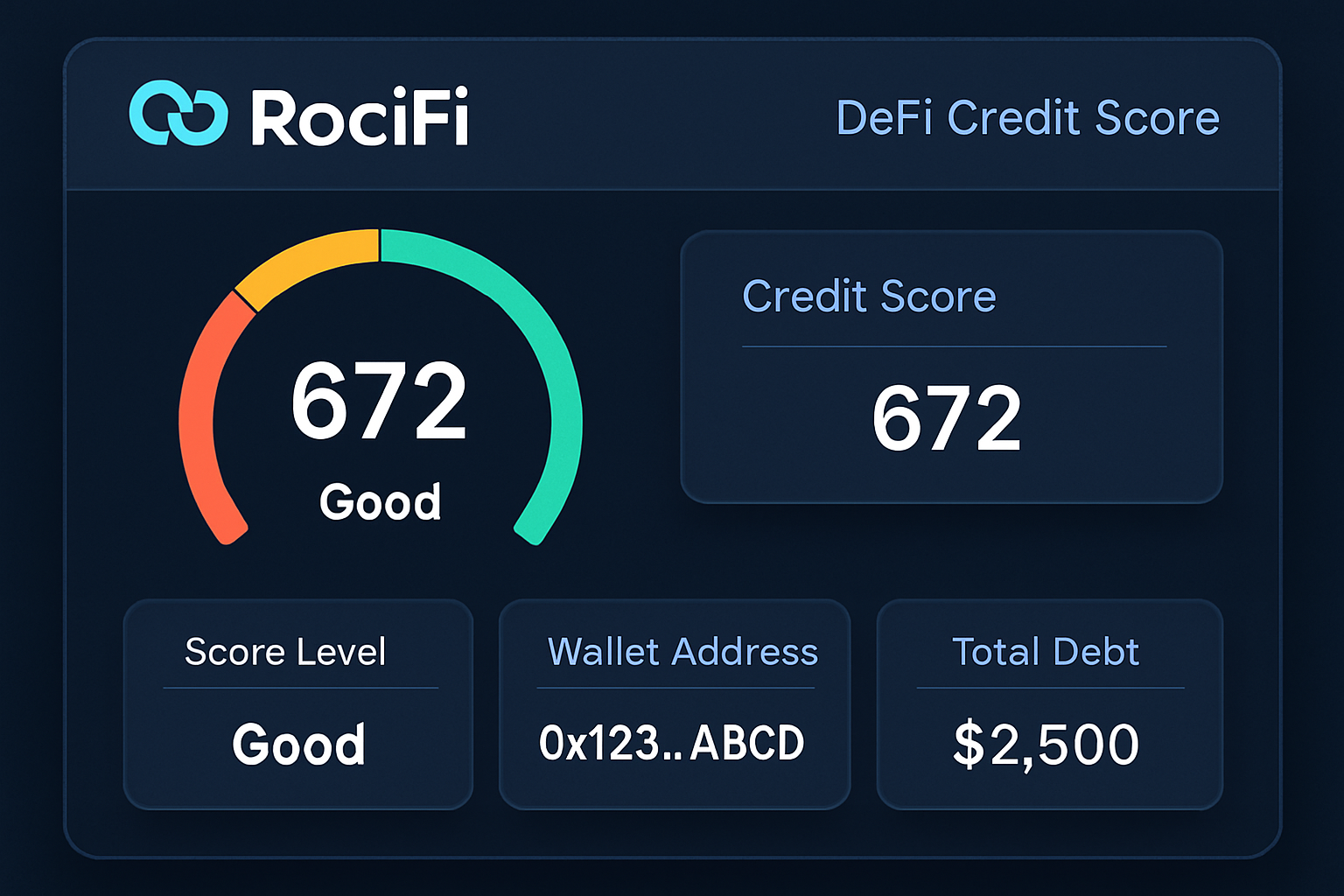

RociFi: Pioneers Non-Fungible Credit Scores (NFCS), unique soulbound tokens that reflect a user’s on-chain creditworthiness. RociFi enables under-collateralized loans, expanding access to DeFi lending through innovative credit modeling.

-

Spectral: Utilizes the Multi-Asset Credit Risk Oracle (MACRO) to issue Creditworthiness NFTs (cwNFTs), allowing users to leverage their blockchain reputation for better borrowing terms and broader financial opportunities.

-

Cred Protocol: Delivers real-time, cross-chain credit scoring and reporting by analyzing user activity across blockchains and protocols. Cred Protocol’s data-driven approach helps lenders accurately price risk and unlock new lending models.

Pioneering Protocols: How On-Chain Credit Scores Work in Practice

Credora made headlines in July 2024 by launching real-time on-chain credit scores in partnership with leading lending markets. Their analytics aggregate data across multiple blockchains and protocols, providing investors with granular risk assessments and borrowers with fairer access to capital.

RociFi takes a novel approach with its Non-Fungible Credit Scores (NFCS): soulbound tokens that represent a user’s on-chain reputation. These tokens unlock access to under-collateralized loans within RociFi’s ecosystem based on actual blockchain activity rather than arbitrary criteria.

Spectral, meanwhile, leverages its Multi-Asset Credit Risk Oracle (MACRO) to mint Creditworthiness NFTs (cwNFTs). These NFTs serve as portable proof of trustworthiness across DeFi platforms, streamlining onboarding and lowering barriers for responsible borrowers.

The Benefits: Efficiency, Inclusion and Trust in DeFi Lending Protocols

The impact of on-chain credit scoring isn’t just theoretical, it’s measurable:

- Capital Efficiency: By reducing collateral requirements, protocols can deploy more capital into productive use while offering better rates for both lenders and borrowers.

- Risk Management: Quantifiable metrics allow for dynamic interest rates tailored to individual risk profiles, not one-size-fits-all terms.

- Financial Inclusion: Users without large crypto holdings can now access loans based on their proven track record, broadening participation in decentralized finance.

- Ecosystem Trust: Transparent scoring models reduce information asymmetry between lenders and borrowers, fostering trust throughout the decentralized economy.

The implications are massive. As noted by industry analysts and recent research papers (read more here), efficient on-chain credit scores could unlock trillions of dollars in new liquidity, empowering entrepreneurs, traders, and everyday users alike.

A Glimpse Ahead: The Road to Mainstream Adoption

This is just the beginning. As data models mature and adoption spreads across protocols, we’ll see even greater integration between traditional finance logic and decentralized architecture. The future of lending is being built right now, on transparent code rather than closed-door committees, and it’s open to anyone ready to prove their reliability on-chain.

For DeFi lending protocols, the integration of on-chain credit scores is more than a technological upgrade, it’s a paradigm shift in how trust and risk are quantified. These blockchain-native credit models don’t just enable new loan products; they redefine what it means to be creditworthy in a decentralized world. As protocols like Credora, RociFi, Spectral, and Cred Protocol compete to set the standard, users benefit from increased choice and fairer access to liquidity.

Overcoming Challenges: Privacy, Data Integrity, and Adoption

Of course, progress isn’t without hurdles. One of the most pressing concerns for users is privacy. On-chain scoring must balance transparency with confidentiality, ensuring that sensitive financial data remains protected even as it’s used to build trust. Leading platforms are tackling this through cryptographic techniques and zero-knowledge proofs that verify creditworthiness without exposing granular transaction details.

Data integrity is another critical factor. Since scores are generated from blockchain activity, ensuring that data sources are reliable and free from manipulation is paramount. Protocols increasingly use cross-chain analytics and reputation-based mechanisms to guard against gaming or Sybil attacks.

Finally, widespread adoption depends on seamless user experience. Borrowers shouldn’t need a PhD in cryptography to access a loan. The most successful platforms will be those that abstract away complexity while delivering robust security and actionable insights for both lenders and borrowers.

Unlocking New Opportunities Across the Ecosystem

The ripple effects extend far beyond individual loans. As on-chain credit scoring unlocks undercollateralized lending, it also enables new types of financial products, dynamic lines of credit, real-time insurance underwriting, even decentralized identity solutions tied to economic behavior rather than paperwork or geography.

Lenders gain access to more granular risk assessment tools, which means they can confidently deploy capital at scale without falling back on blunt over-collateralization requirements. For borrowers with strong on-chain reputations but limited assets, this marks an unprecedented opportunity to participate fully in the digital economy.

The Path Forward: Building Decentralized Finance Trust at Scale

The promise of decentralized finance has always hinged on trust, trust in code, in transparency, in community-driven governance. On-chain credit scores represent the next evolution: programmable trust rooted in verifiable activity rather than opaque algorithms or subjective judgments.

As these systems mature and standards emerge across chains and protocols, expect even greater interoperability between traditional finance and DeFi platforms. The walls are coming down, and with them, barriers to opportunity for millions worldwide. If you’re building or participating in this new era of lending, now’s the time to leverage your blockchain reputation into tangible financial freedom.

Top Benefits of On-Chain Credit Scores in DeFi

-

Unlocks Under-Collateralized Lending: On-chain credit scores, as implemented by platforms like RociFi and Cred Protocol, allow users to access loans with less or no collateral by leveraging their blockchain transaction history.

-

Enhances Capital Efficiency: By reducing the need for excessive collateral, on-chain credit scoring systems free up capital for both borrowers and lenders, increasing liquidity across DeFi platforms such as Credora.

-

Improves Risk Assessment and Transparency: Solutions like Spectral provide quantifiable, real-time credit metrics—enabling lenders to make more informed decisions and set fairer interest rates.

-

Expands Financial Inclusion: On-chain credit scores empower users without significant assets to access DeFi loans based on their on-chain reputation, opening up financial services to a broader global audience.

-

Boosts Trust and Market Participation: Transparent, tamper-proof credit scoring mechanisms foster greater confidence among both borrowers and lenders, encouraging more users to participate in DeFi lending markets.