Imagine a world where a farmer in Kenya, a developer in Argentina, and a startup in Vietnam can all access capital from a global pool of lenders, without ever meeting, trusting, or even knowing one another. This is not a utopian vision but the emerging reality of on-chain credit scoring in decentralized finance (DeFi). The shift from collateral-heavy, permissioned lending to borderless, algorithmically-assessed trust is unlocking new economic potential for billions.

Why Traditional DeFi Lending Hits a Wall

DeFi’s early promise was radical inclusivity: anyone could lend or borrow crypto assets by interacting with smart contracts. However, the absence of reliable credit assessment forced protocols to demand excessive collateral, often 150% or more of the loan value. This model, while trustless, essentially excluded anyone without significant crypto holdings and failed to serve those who needed credit most.

The core problem? Lack of decentralized reputation. Without a way to gauge borrower risk on-chain, lenders defaulted to over-collateralization as their only safety net. This approach limited capital efficiency and stunted DeFi’s reach compared to traditional finance, where nuanced credit scores enable under-collateralized and unsecured loans at scale.

“On-chain credit scoring is not just an upgrade for DeFi, it’s the key to unlocking a $1.5 trillion opportunity in borderless lending. “

The Mechanics of On-Chain Credit Scoring

So how does on-chain credit scoring work? Unlike opaque, centralized bureaus, these systems analyze transparent blockchain data, balances, transaction history, protocol interactions, and even cross-chain activity, to generate a Web3 credit score. This score acts as a decentralized reputation layer, enabling protocols to calibrate risk and offer tailored loan terms.

Consider platforms like RociFi and Creditlink. RociFi’s Non-Fungible Credit Scores (NFCS) are composable digital identities that reflect a user’s financial behavior across DeFi. Creditlink leverages AI to create modular credit profiles usable by DAOs, lending protocols, and cross-chain bridges. Reputation DAO goes further by integrating real-world data and decentralized identity, bridging the gap between Web3 and TradFi risk models.

Key Benefits of On-Chain Credit Scoring in DeFi

-

Enables Under-Collateralized Lending: On-chain credit scoring allows borrowers to access loans with less collateral by assessing their blockchain-based financial history, increasing capital efficiency compared to traditional over-collateralized DeFi lending.

-

Improves Risk Assessment: Platforms like RociFi and Creditlink use on-chain data and AI to evaluate user behavior, enabling lenders to make more informed decisions and offer tailored interest rates.

-

Fosters Financial Inclusion: On-chain credit scoring opens DeFi lending to a broader, global user base, including those without access to traditional credit systems, by leveraging transparent blockchain data rather than centralized credit bureaus.

-

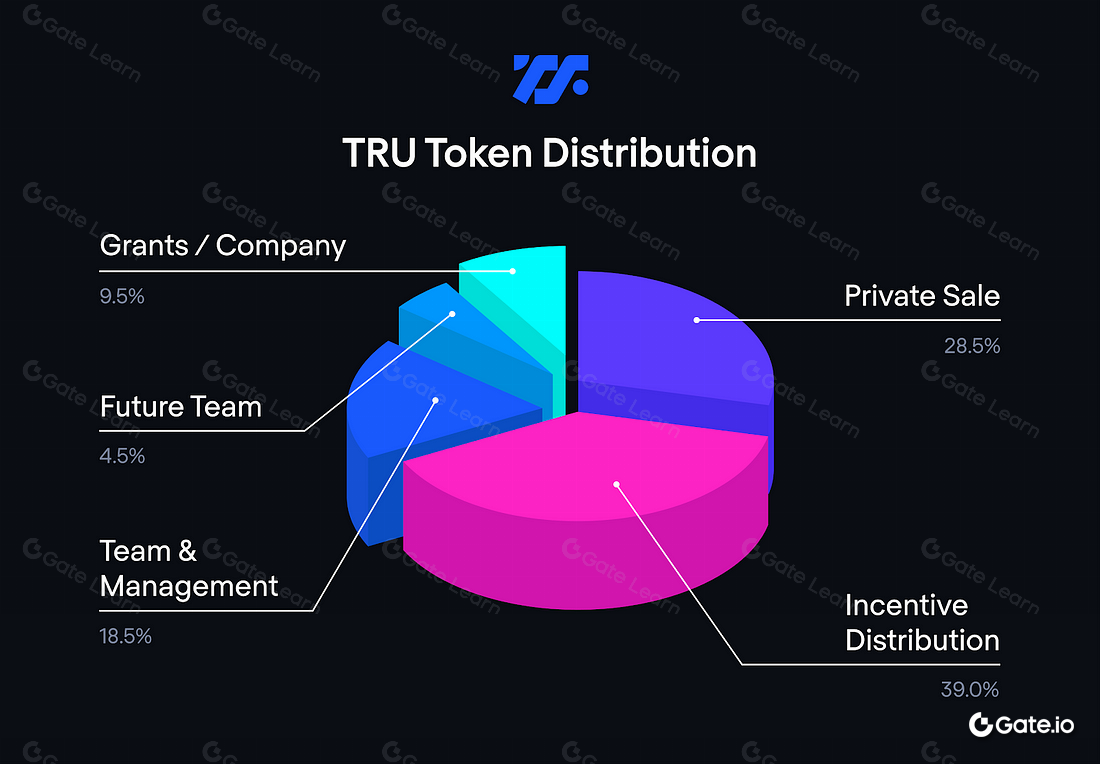

Supports Reputation-Based Lending: Projects like TrueFi use both on-chain and off-chain data to build crypto-native credit scores, enabling reputation-based lending and reducing reliance on collateral.

-

Enhances Transparency and Trust: All credit assessments and lending activities are recorded on the blockchain, ensuring transparency, auditability, and trustless interactions between lenders and borrowers.

-

Bridges DeFi and Traditional Finance: Solutions like Reputation DAO integrate real-world financial data with DeFi, allowing users to leverage their traditional financial history and identity for on-chain credit, expanding lending opportunities.

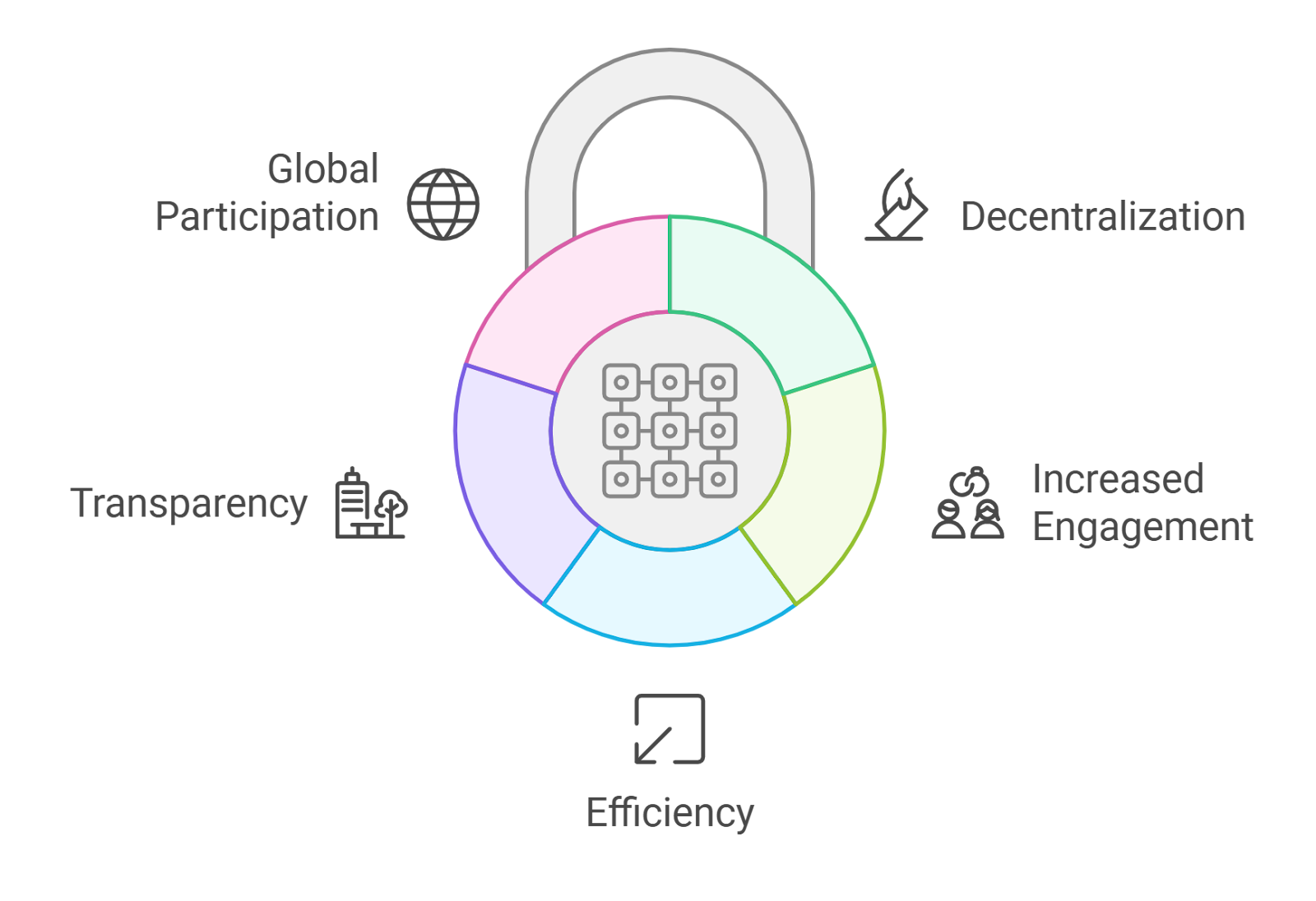

This evolution means that for the first time, lenders can offer permissionless loans based on trust scores rather than hard collateral. Borrowers with strong on-chain reputations can access capital more efficiently, while lenders enjoy improved risk-adjusted yield, mirroring the sophistication of traditional fixed income markets but without geographic or institutional barriers.

Borderless Lending: Real-World Impact and Use Cases

The implications are profound. A developer in Southeast Asia can build up a blockchain trust score through consistent DeFi activity, then access working capital from a DAO headquartered in Europe. A small business in Africa can borrow stablecoins to fund expansion, backed not by land titles but by years of transparent on-chain payments and repayments.

This composability extends beyond lending. Protocols like Cred Protocol and LayerBankFi are experimenting with blockchain-based credit modules that plug into everything from NFT marketplaces to decentralized insurance pools, creating an interoperable reputation layer for all of Web3.

For a deeper dive into how these systems empower DeFi platforms, see our guide on how on-chain credit scores empower DeFi lending platforms.

From Over-Collateralization to Trustless Efficiency

On-chain credit scoring is already reshaping DeFi’s risk landscape. By providing granular wallet-level risk assessments, protocols can offer differentiated interest rates and leverage options based on actual user behavior rather than blanket rules. This approach reduces systemic risk while making lending more accessible and efficient for all participants.

Crucially, this shift is not just theoretical. Platforms like TrueFi are already combining on-chain and off-chain data to create robust crypto-native credit scores, enabling reputation-based lending at scale. This hybrid approach means that DeFi lenders can extend under-collateralized loans with confidence, knowing that both blockchain behavior and select real-world data points are factored into risk models. The result: capital flows more freely, and users without deep crypto reserves are no longer sidelined.

These innovations are also driving the development of decentralized credit bureaus, protocols that act as open, composable layers for credit assessment across the Web3 ecosystem. By standardizing how blockchain trust scores are calculated and shared, these bureaus are laying the groundwork for interoperable, borderless finance where a user’s reputation follows them across any protocol, wallet, or chain.

Challenges, Privacy, and the Road Ahead

Of course, the path to borderless, trustless lending is not without hurdles. Privacy remains a key concern: while blockchain transparency enables granular credit analysis, it also raises questions about user data exposure and potential discrimination. Zero-knowledge proofs and privacy-preserving computation are emerging as solutions, allowing protocols to verify creditworthiness without revealing sensitive details. For example, zkCredit and other privacy-first initiatives are pioneering models where users can prove their eligibility for loans without exposing every transaction.

Another challenge is adoption. Many DeFi users are still unfamiliar with how blockchain trust scores work or why they matter. Education and user experience improvements are critical to ensure that on-chain credit scoring doesn’t become a new gatekeeper, but rather an enabler of inclusion. Protocols must also guard against manipulation and sybil attacks, ensuring that credit scores reflect genuine behavior rather than gaming.

Key Challenges and Solutions for On-Chain Credit Scoring Adoption

-

Challenge: Data Privacy and User Anonymity – On-chain credit scoring requires access to users’ financial histories, raising concerns about privacy and potential exposure of sensitive data.Solution: Platforms like RociFi use Non-Fungible Credit Scores (NFCS) and cryptographic techniques to analyze on-chain activity while preserving user anonymity.

-

Challenge: Limited Off-Chain Data Integration – Many DeFi users lack an on-chain history, making it difficult to assess creditworthiness solely from blockchain data.Solution: TrueFi combines on-chain and off-chain data to create crypto-native credit scores, enabling reputation-based lending and expanding access to under-collateralized loans.

-

Challenge: Cross-Platform and Cross-Chain Compatibility – Fragmented DeFi ecosystems hinder the portability of credit scores across different platforms and blockchains.Solution: Creditlink builds composable credit modules using AI and on-chain behavior, optimizing trust and credit flows across DeFi, DAOs, and cross-chain environments.

-

Challenge: Identity Verification and Sybil Resistance – Ensuring that each credit score corresponds to a unique individual or entity is crucial for preventing fraud and gaming of the system.Solution: Reputation DAO leverages real-world financial data and decentralized identity verification to bridge DeFi and traditional finance, enhancing trust and sybil resistance.

-

Challenge: Over-Collateralization and Capital Inefficiency – Traditional DeFi lending often requires borrowers to lock up excessive collateral due to lack of reliable credit assessment.Solution: On-chain credit scoring platforms like RociFi and TrueFi enable under-collateralized lending by evaluating users’ on-chain behavior, improving capital efficiency and expanding lending opportunities.

Despite these obstacles, the momentum is undeniable. As more protocols integrate on-chain credit modules and decentralized reputation layers, the DeFi landscape is rapidly evolving from a collateral-first paradigm to a risk-adjusted, trustless ecosystem. This transformation is not just about efficiency, it’s about rewriting the rules of who gets access to capital and on what terms.

Unlocking the Future of Permissionless Lending

Looking ahead, the convergence of AI-driven analytics, privacy technologies, and interoperable credit bureaus points toward a future where borderless lending is the norm, not the exception. Imagine a world where your Web3 credit score is as portable and impactful as a passport, opening doors to capital, partnerships, and opportunities wherever you go in the decentralized economy.

For DeFi lenders, this means new avenues for risk-adjusted yield and global market access. For borrowers, it’s a chance to build financial reputations from scratch, untethered from traditional gatekeepers. And for the ecosystem as a whole, it signals a move toward a more inclusive, resilient, and efficient financial system, one where yield is more than a number, and trust is algorithmic, not institutional.

To explore further how these innovations are transforming risk and opportunity in decentralized lending, see our analysis on how on-chain credit scoring transforms DeFi lending.