Decentralized finance (DeFi) is rapidly evolving, and the emergence of cross-chain credit layers is at the heart of its latest transformation. For years, DeFi lending protocols have been hampered by over-collateralization and limited credit assessment tools, often requiring users to lock up more value than they borrow. Now, the integration of interoperable credit infrastructure across multiple blockchains is unlocking a new era of financial inclusivity and efficiency.

Cross-Chain Credit Layers: The Backbone of Next-Gen DeFi Lending

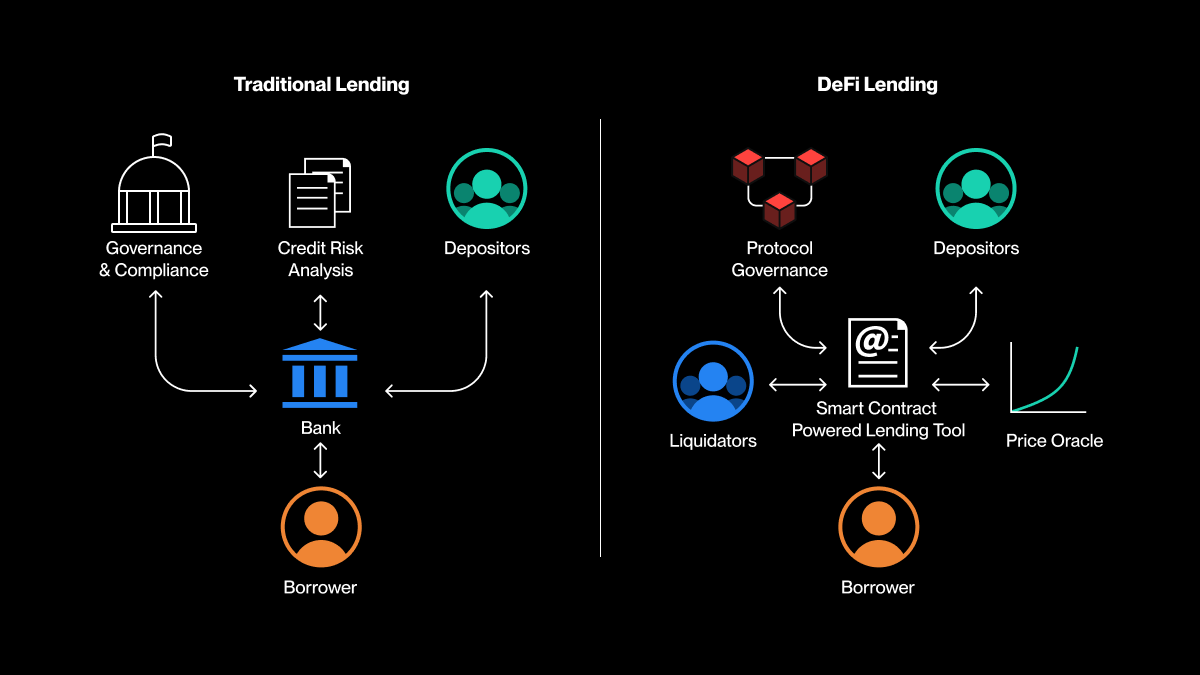

The concept of a cross-chain credit layer refers to a decentralized system that enables the transfer of both assets and verifiable credit data across different blockchain networks. Unlike siloed lending pools limited to one chain, these universal credit layers allow borrowers and lenders to interact seamlessly regardless of where their assets reside.

Protocols like Lendvest are leading this movement by integrating Chainlink’s Cross-Chain Interoperability Protocol (CCIP), making it possible for users’ on-chain behaviors on Ethereum to influence their borrowing terms on Avalanche or other chains. This not only improves capital efficiency but also lays the groundwork for under-collateralized or even uncollateralized loans in DeFi.

The rise of LayerZero DeFi, Axelar, and CCIP exemplifies how messaging protocols are tackling the technical hurdles of secure cross-chain communication. These solutions are essential for building trustless bridges that transmit both tokens and sensitive credit data without relying on centralized custodians.

On-Chain Credit Scores: From Theory to Reality

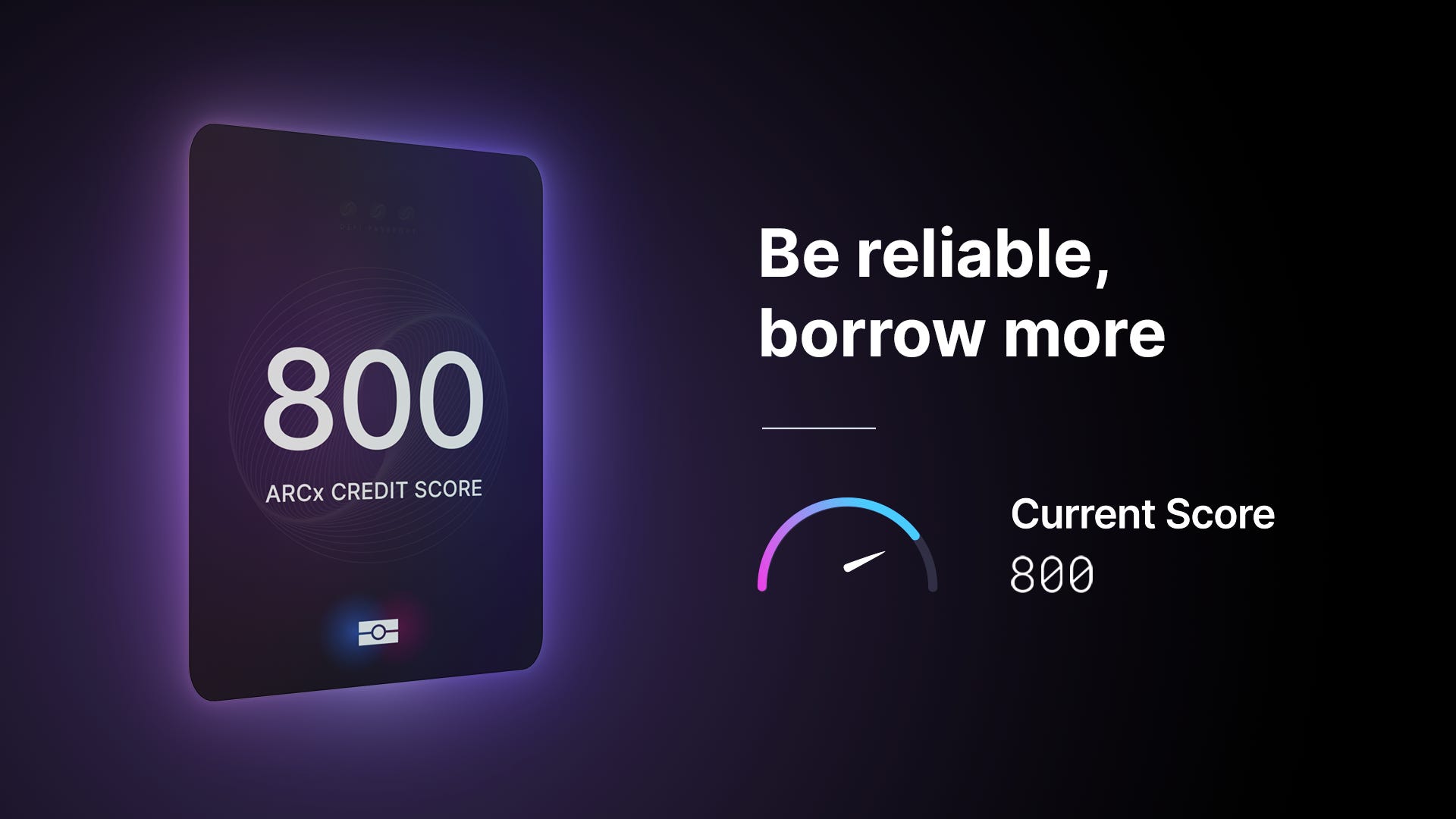

The next leap in DeFi lending comes from robust on-chain credit scores. Unlike traditional FICO scores, these assessments are built using transparent blockchain activity – wallet histories, protocol interactions, repayment records, and more. Projects such as Creditlink employ AI-powered analytics to distill complex on-chain behavior into composable modules for DAOs and lending platforms (source). Similarly, ARCx’s “DeFi Passport” assigns a score based on multi-protocol activity that can travel with users across ecosystems (source).

This innovation is already reshaping risk management in DeFi:

Key Benefits of On-Chain Credit Scores in DeFi

-

Reduced Over-Collateralization: On-chain credit scores, as implemented by platforms like Credora and ARCx, allow borrowers to access under-collateralized or even uncollateralized loans, making DeFi lending more accessible and capital-efficient.

-

Enhanced Risk Assessment: Lenders benefit from transparent, immutable records of borrower activity, with solutions from Creditlink and ARCx DeFi Passport providing real-time creditworthiness data to inform safer lending decisions.

-

Cross-Chain Interoperability: Protocols such as Lendvest (using Chainlink CCIP) and LayerZero enable seamless transfer of credit data and assets across multiple blockchains, expanding lending opportunities and market reach.

-

AI-Powered Credit Insights: Platforms like Ozean and Kylix Finance leverage AI to analyze on-chain behavior, providing more accurate and dynamic credit ratings for borrowers and lenders across networks like Ethereum and Solana.

-

Greater Transparency and Trust: On-chain credit scoring systems, such as those offered by Credora and Creditlink, operate on public blockchains, ensuring that credit assessments are verifiable and resistant to manipulation.

The ability to verify a user’s trustworthy track record – even if it spans multiple blockchains – means that protocols can confidently offer lower collateral requirements or preferential rates. As more sophisticated AI models enter the space (as seen with Ozean and Kylix Finance), these scores become increasingly predictive while maintaining privacy through zero-knowledge proofs.

Real-World Examples: LayerBank and The Universal Credit Layer

LayerBank, as highlighted by Nansen’s research, exemplifies how modern DeFi platforms are embracing cross-chain lending. By supporting asset management across several EVM-compatible chains from a single dashboard, LayerBank empowers users to maximize yield opportunities without being locked into one ecosystem. This flexibility is only possible because underlying universal credit layers ensure that reputation and risk profiles can be ported between chains without friction.

Lagrange Labs’ work with state proofs further demonstrates how secure validation of off-chain or cross-chain data can underpin reliable lending decisions (source). Instead of requiring repeated manual verification steps or custodial intermediaries, these cryptographic proofs automate trust between disparate networks – making scalable cross-chain lending truly viable.

As cross-chain credit infrastructure matures, we’re witnessing a dramatic shift in how capital flows across the decentralized economy. The move from isolated, single-chain lending pools to interoperable, data-rich credit layers is not just a technical upgrade but a fundamental change in DeFi’s value proposition. Users are no longer defined by a single wallet or chain; instead, their on-chain reputation is composable and portable, opening doors to new financial products and fairer access to liquidity.

Platforms like Credora are already making waves by embedding on-chain credit scoring directly into DeFi lending markets. By partnering with a range of protocols, they’re enabling lenders to evaluate risk with unprecedented transparency. This is a radical improvement over the opaque, over-collateralized systems of the past, and it’s catching the attention of both institutional players and crypto-native communities alike.

The Road Ahead: Universal Credit Layers and DeFi’s Next Growth Wave

What does the future hold for cross-chain credit layers? As more protocols adopt interoperable standards, we’re likely to see:

Key Trends in Universal Credit Layers for DeFi

-

AI-Powered On-Chain Credit Scoring: Platforms like Creditlink and Credora are leveraging artificial intelligence and on-chain data to assess borrower creditworthiness, enabling under-collateralized or even uncollateralized loans in DeFi.

-

Cross-Chain Interoperability Protocols: Solutions like Chainlink CCIP and LayerZero are enabling seamless data and asset transfers between blockchains, forming the backbone for universal credit layers.

-

Composable Credit Modules: Projects such as Creditlink are building modular credit systems that can be integrated across DeFi and DAO ecosystems, allowing for flexible and programmable credit assessment.

-

DeFi Passports and On-Chain Identity: Platforms like ARCx DeFi Passport are creating digital identities based on users’ on-chain activities, standardizing credit scores and influencing loan terms across multiple protocols.

-

AI-Enhanced Cross-Chain Lending Platforms: Protocols such as Ozean, Kylix Finance, and LayerBank are integrating AI-powered credit ratings and supporting lending across networks like Ethereum, Solana, SUI, and Polkadot.

-

Transparent and Immutable Credit Histories: On-chain credit layers provide public, tamper-proof records of borrower histories, improving risk management and transparency for lenders and borrowers alike.

One particularly exciting development is the potential for zero-collateral loans. As Lendvest and others demonstrate, when a user’s trustworthy history is recognized across chains, lenders can confidently extend credit without demanding excessive collateral. Combined with privacy-preserving AI analytics, this could unlock trillions in untapped value and finally bridge the gap between Web3 and real-world finance.

Of course, challenges remain. Ensuring the security of cross-chain messaging (the focus of LayerZero and Axelar), maintaining user privacy, and preventing Sybil attacks are all active areas of research. But the momentum is undeniable. As more lending platforms, DAOs, and even traditional institutions experiment with these new credit primitives, DeFi’s credit infrastructure will become more robust, inclusive, and efficient.

Why This Matters: Beyond Hype to Real Utility

The promise of cross-chain lending and on-chain credit scores isn’t just about technical novelty – it’s about empowering users with real financial agency. Whether you’re a DAO contributor seeking an uncollateralized loan, a protocol treasurer optimizing capital efficiency, or a newcomer building a reputation from scratch, these innovations are lowering barriers and expanding opportunity.

Ultimately, the rise of universal credit layers marks a turning point for DeFi. By aligning incentives, reducing risk, and fostering interoperability, this new paradigm invites a broader audience into the decentralized economy. The next chapter isn’t just about composability or yield – it’s about trust, reputation, and sustainable growth for everyone.