Decentralized finance (DeFi) has unlocked unprecedented access to global lending markets, but the absence of trust-minimized credit risk assessment has kept the sector overly reliant on over-collateralization. This capital inefficiency locks out a vast segment of potential borrowers and restricts liquidity for lenders. Enter on-chain credit scoring: a data-driven innovation that leverages blockchain transparency to transform how risk is measured and credit is extended across DeFi protocols.

Why DeFi Needs On-Chain Credit Scoring Now

The DeFi ecosystem has matured rapidly, but its growth remains hampered by the inability to distinguish between high- and low-risk borrowers in a decentralized manner. Traditional finance relies on centralized bureaus and opaque algorithms, while most DeFi lending platforms demand collateralization ratios between 120% and 200%. This model is not only exclusionary but also results in suboptimal capital allocation.

The current context, as highlighted by recent research (arXiv: OCCR Score), underscores how an On-Chain Credit Risk Score (OCCR) can quantify wallet-level risk using probabilistic models based on blockchain activity. By evaluating user behavior, repayment history, asset diversity, and protocol interactions, these scores allow protocols to calibrate interest rates, leverage limits, and loan terms with greater precision.

The Mechanics: How Blockchain Credit Bureaus Work

A new breed of blockchain credit bureaus, such as Creditlink and RociFi, are pioneering composable modules that analyze a user’s on-chain footprint. These systems ingest transaction histories, protocol participation data, wallet balances over time, and even cross-chain behaviors. The result? Dynamic crypto credit scores that are portable across DeFi platforms.

For example:

- Creditlink: Uses AI to parse behavioral signals from wallets, like frequency of repayments or staking patterns, to assign trust levels usable by DAOs and lending pools.

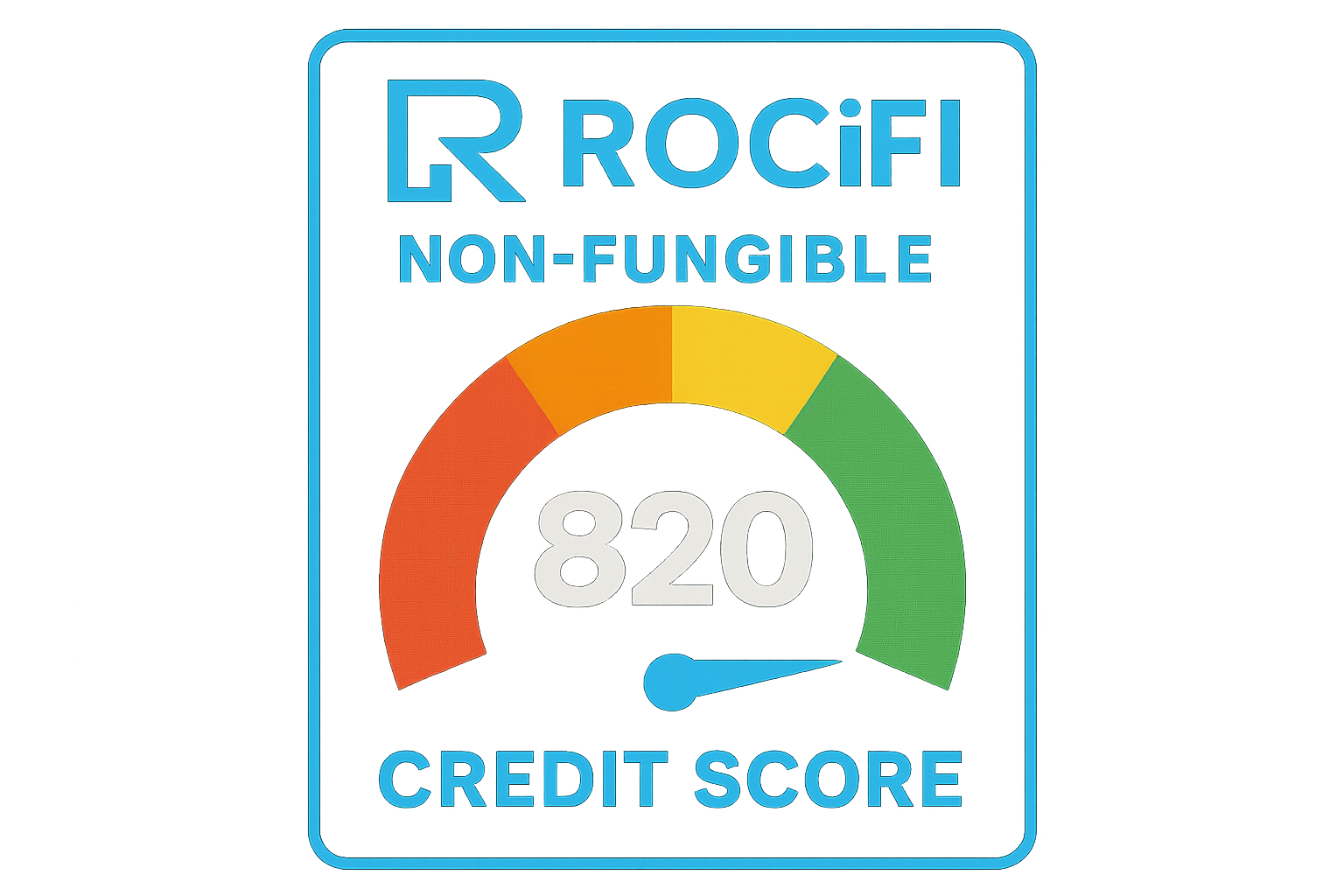

- RociFi: Issues Non-Fungible Credit Scores (NFCS), which are soulbound tokens representing a user’s unique risk profile based exclusively on their on-chain actions.

- Reputation DAO: Blends off-chain identity with smart contract logic to bridge real-world reputation into Web3 borrowing decisions.

- DeCredit and TrueFi: Aggregate both blockchain-native and external financial data to enable true under-collateralized or even uncollateralized loans, a key step toward parity with TradFi lending models.

This evolution means that DeFi lenders can move beyond blunt collateral requirements toward nuanced risk-based pricing, ultimately increasing yields for lenders while broadening access for responsible borrowers.

Key Benefits of Decentralized Credit Scoring in DeFi

-

Enables Under-Collateralized Lending: On-chain credit scoring allows DeFi protocols to assess borrower risk more accurately, reducing the need for excessive collateral and enabling under-collateralized or even uncollateralized loans. This boosts capital efficiency across platforms like RociFi and DeCredit.

-

Promotes Financial Inclusion: By evaluating users’ on-chain activity, decentralized credit scoring offers access to credit for individuals without significant crypto assets, fostering inclusion for the unbanked. Platforms such as Creditlink and Reputation DAO are at the forefront of this movement.

-

Enables Dynamic and Transparent Credit Profiles: On-chain credit scores, such as RociFi’s Non-Fungible Credit Scores (NFCS), are updated in real-time based on blockchain activity, ensuring transparency and up-to-date borrower profiles.

-

Facilitates Cross-Platform and Cross-Chain Lending: Composable credit modules, like those developed by Creditlink, allow users to port their creditworthiness across DeFi protocols and chains, expanding borrowing opportunities and trust throughout the ecosystem.

Transforming DeFi Lending Risk Assessment

The integration of on-chain credit scoring into lending protocols is already reshaping risk management strategies across the sector. Lenders now have actionable insights into borrower reliability without sacrificing privacy or decentralization. According to recent analyses from GARP and Huma Finance, this enables differentiated interest rates based on real-time user profiles rather than one-size-fits-all policies.

This shift brings several implications:

- Enhanced Capital Efficiency: By allowing under-collateralized loans based on reliable scores, more capital can flow through protocols without excessive lockups.

- Increased Accessibility: Users with limited assets but strong on-chain reputations gain access to fairer borrowing terms, a major leap for financial inclusion in Web3.

- Evolving Risk Models: Protocols can now build predictive analytics around borrower performance using transparent data sources rather than black-box algorithms or social graphs alone.

If you want a deeper dive into how these mechanisms lower systemic risk while empowering users, see our guide on how on-chain credit scores power trust and lower risk in DeFi lending.

As decentralized credit scoring becomes more sophisticated, the landscape of DeFi lending is evolving rapidly. Protocols are leveraging real-time blockchain analytics to refine risk assessment models, creating a feedback loop that rewards responsible behavior and penalizes risky actors. This dynamic approach not only aligns incentives for both borrowers and lenders but also helps protocols respond to emerging threats and opportunities in a volatile crypto environment.

One of the most promising outcomes is the ability to establish a verifiable, portable reputation across platforms. With innovations like RociFi’s Non-Fungible Credit Scores (NFCS) and Creditlink’s AI-driven modules, users can build a persistent credit identity that unlocks better terms as they demonstrate reliability. This marks a significant departure from siloed, protocol-specific evaluations toward an open, interoperable reputation layer for Web3 finance.

Challenges and Considerations for Crypto Enthusiasts

While the promise of on-chain credit scoring is substantial, several challenges remain. Privacy concerns persist despite advances in zero-knowledge proofs and selective disclosure mechanisms; users must weigh the benefits of improved access against potential risks to their data sovereignty. Additionally, score manipulation, such as wash trading or orchestrated repayment histories, remains a threat that protocols must mitigate through robust anomaly detection and multi-factor analysis.

Furthermore, the integration of off-chain signals (e. g. , real-world income or identity) introduces new vectors for centralization and regulatory scrutiny. Projects like Reputation DAO are experimenting with hybrid models that balance transparency with compliance, but the optimal blend is still an open question for DeFi architects.

What’s Next? The Road Ahead for Decentralized Credit Bureaus

The next wave of innovation will likely focus on composability, enabling users to leverage their crypto credit scores across borrowing, insurance, governance participation, and even employment within DAOs. As protocols like DeCredit push toward eliminating collateral requirements altogether by combining on- and off-chain data in decentralized oracles, we may see DeFi lending rival traditional finance not just in accessibility but also in sophistication.

Top Real-World Use Cases of On-Chain Credit Bureaus in DeFi

-

Under-Collateralized and Uncollateralized Lending: Platforms like RociFi use Non-Fungible Credit Scores (NFCS) to enable borrowers with strong on-chain reputations to access loans with reduced or no collateral requirements, unlocking capital efficiency in DeFi lending.

-

Dynamic Interest Rate and Leverage Adjustments: Protocols such as Creditlink analyze on-chain behavior to assign credit scores, allowing lenders to tailor interest rates and leverage based on borrower risk profiles, optimizing returns and reducing defaults.

-

Cross-Protocol Credit Portability: DeCredit builds decentralized credit oracles that aggregate on-chain and off-chain data, enabling users to carry their creditworthiness across multiple DeFi protocols and ecosystems for seamless borrowing experiences.

-

Bridging DeFi and Traditional Finance: Reputation DAO allows users to leverage real-world identity and financial data in smart contracts, facilitating access to DeFi loans for those with established off-chain credit histories.

-

Automated, Transparent Risk Assessment: TrueFi combines on-chain and off-chain data to generate crypto-native credit scores, enabling automated and transparent risk evaluation for institutional and retail lenders.

For crypto enthusiasts navigating this new paradigm, staying informed about evolving standards and best practices is crucial. Participating in governance decisions around risk parameters or contributing to open-source scoring models can help shape a safer, more inclusive ecosystem.

The bottom line: on-chain credit scoring stands poised to unlock trillions of dollars in latent capital for DeFi by lowering barriers to entry while maintaining rigorous risk controls. As adoption accelerates and methodologies mature, expect decentralized lending markets to become fairer, more transparent, and fundamentally more efficient than ever before.