DeFi lending has exploded in popularity, but its full potential is still limited by a fundamental problem: trust. In traditional finance, your credit score acts as a passport to borrowing opportunities. But in DeFi, pseudonymous wallets and the lack of reliable credit metrics have forced most protocols to demand overcollateralization. That means you often need to lock up more value than you borrow, a massive barrier for many users and a clear drag on capital efficiency.

Why Overcollateralized Lending Holds DeFi Back

Overcollateralized lending might keep lenders safe, but it also keeps trillions of dollars on the sidelines. Imagine needing $10,000 in crypto just to borrow $7,000, hardly an open invitation for new users or underserved communities. This approach was necessary in the early days of DeFi due to the anonymity of blockchain addresses and the absence of any established DeFi credit reputation.

The result? DeFi lending is largely accessible only to those who already have significant assets. It’s efficient for whales and power users, but it leaves out individuals who could benefit most from decentralized financial services.

On-Chain Credit Scores: The Game Changer

This is where on-chain credit scores step in, and why they’re being hailed as a trillion-dollar unlock for DeFi. By analyzing blockchain activity such as transaction history, loan repayments, protocol interactions, and wallet behavior, these scores provide a decentralized alternative to legacy credit checks. Suddenly, lenders can assess borrower risk with real data while keeping everything transparent and privacy-preserving.

Cred Protocol, for example, quantifies lending risk by building decentralized credit scores that aim to expand access for individuals previously locked out of DeFi lending. Spectral Finance has introduced the MACRO score, an on-chain equivalent of FICO, ranging from 300 to 850 based on your wallet’s activity across multiple protocols.

Leading Projects in Decentralized Credit Scoring for DeFi

-

Cred Protocol quantifies on-chain lending risk by building decentralized credit scores, aiming to expand DeFi lending access for individuals and underserved communities.

-

Spectral Finance introduces the Multi-Asset Credit Risk Oracle (MACRO) score, an on-chain equivalent to traditional credit scores, assessing transaction history and loan activity to generate a FICO-like score.

-

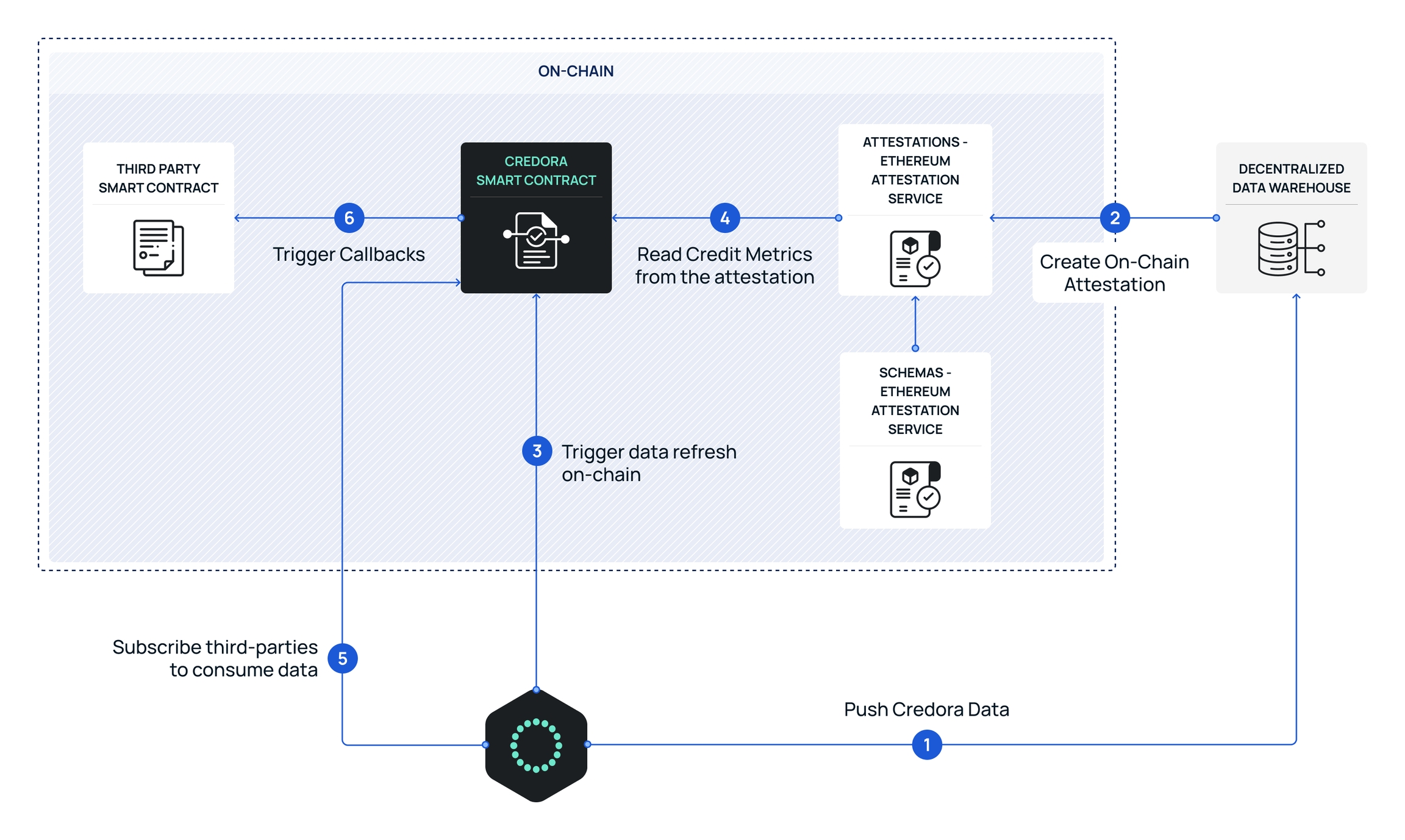

Credora provides on-chain credit assessments by monitoring borrowers’ on-chain assets and liabilities, leveraging zero-knowledge proofs to preserve privacy while enabling risk evaluation.

-

Teller Finance collaborates with Chainlink to issue undercollateralized crypto loans, using zero-knowledge proofs to verify off-chain financial data without exposing sensitive information on-chain.

The beauty here is that all this happens without sacrificing privacy or decentralization. For instance, Credora leverages zero-knowledge proofs so lenders can verify borrower solvency without ever seeing private details, a win-win for both sides.

How Undercollateralized DeFi Lending Actually Works

The mechanics are surprisingly elegant: instead of demanding 150% collateral up front, protocols use blockchain credit assessment tools to gauge your trustworthiness based on your wallet’s past actions. Repay loans reliably? Your score goes up. Get liquidated or default? Your score drops, and so does your future borrowing power.

This shift unlocks more capital and creates new opportunities for everyday users, not just crypto insiders with deep pockets. It also allows protocols to offer differentiated terms based on each user’s risk profile rather than treating everyone as equally risky by default.

The Tech Behind Decentralized Credit Scoring

Building robust wallet reputation DeFi systems isn’t easy. Developers are tackling challenges like pseudonymity (how do you know someone isn’t just spinning up new wallets?), massive data volumes (think millions of transactions per day), and bots trying to game the system. That’s why many projects are layering in AI-powered analytics and privacy-preserving cryptography, like zero-knowledge proofs, to keep things fair and secure.

As the infrastructure matures, we’re seeing a convergence between decentralized credit scoring and privacy tech. Tools like zero-knowledge proofs allow protocols to verify off-chain financial data or sensitive on-chain activity without ever revealing the raw information. This means users can prove their creditworthiness while maintaining control over their personal details, something nearly impossible in traditional finance.

Take Teller Finance, which has teamed up with Chainlink to bring undercollateralized loans to DeFi. Their approach uses zero-knowledge proofs to validate bank balances and other key metrics, enabling borrowers to unlock liquidity without oversharing. Similarly, Credora’s real-time monitoring of on-chain assets and liabilities gives lenders a dynamic view of borrower health while keeping sensitive data private.

What This Means for DeFi Users and Protocols

The shift toward undercollateralized lending isn’t just about capital efficiency, it’s about broadening access. Projects now have the tools to serve users who were previously excluded due to lack of crypto wealth, limited transaction history, or concerns over privacy. As these scoring models become more sophisticated, expect a wave of new products: microloans for emerging markets, student financing for Web3 education, even buy-now-pay-later options for NFT marketplaces.

Lenders also benefit from more granular risk management. Instead of one-size-fits-all terms, they can tailor rates and collateral requirements based on each user’s evolving profile. This flexibility encourages responsible borrowing and rewards good behavior, an essential feedback loop for any thriving credit ecosystem.

Undercollateralized DeFi lending is not just a technical upgrade, it’s a cultural shift toward trust-minimized finance where your blockchain reputation becomes your passport to opportunity.

The Road Ahead: Challenges and Opportunities

No system is perfect yet. Challenges remain around sybil resistance (preventing users from gaming scores by creating multiple wallets), cross-chain interoperability (tracking credit across different blockchains), and standardizing metrics so scores mean the same thing everywhere. But progress is rapid: new standards are emerging, and projects like Spectral Finance are already offering plug-and-play APIs for developers who want to integrate DeFi lending innovation into their dApps.

The real promise? As wallet reputation systems mature and adoption grows, we could see an explosion in both the volume and variety of DeFi lending products, potentially unlocking trillions in value that’s currently sitting idle due to overcollateralization requirements (source). For users with strong on-chain histories but limited up-front capital, this is nothing short of revolutionary.

If you’re curious how this might impact your own DeFi journey, or if you’re a developer looking to build fairer financial tools, now’s the time to explore decentralized credit scoring platforms. By participating early, you help shape a more open and efficient financial future where opportunity isn’t locked behind arbitrary barriers.