Decentralized finance (DeFi) is rewriting the rules of lending. Traditionally, crypto loans required borrowers to over-collateralize – locking up more value than they borrowed – to protect lenders from defaults. While this reduced risk, it also limited access and capital efficiency. Now, a new wave of innovation is sweeping across DeFi: on-chain credit scores. These blockchain-native reputation engines are paving the way for zero collateral loans in crypto, making DeFi unsecured lending a reality for the first time.

The Rise of On-Chain Credit Scores: A Trust Layer for DeFi

At its core, an on-chain credit score is a decentralized, transparent assessment of a wallet’s financial behavior and trustworthiness. Instead of relying on opaque TradFi bureaus, these scores analyze blockchain data – transaction history, asset movements, protocol interactions – to build an immutable profile. The result? A privacy-preserving yet powerful way to gauge creditworthiness without requiring users to lock up capital.

This paradigm shift has major implications. As highlighted in recent market analysis (Zeru Finance), integrating decentralized credit scoring could unlock trillions in untapped liquidity by bringing real-world credit dynamics on-chain. No longer do users need to be whales or hold idle assets just to access basic financial services.

Pioneering Platforms: How Zero-Collateral Loans Are Becoming Possible

The vision of zero-collateral loans isn’t science fiction anymore. Several innovative projects are already deploying wallet reputation engines and decentralized credit systems that assess risk based on blockchain activity:

Top DeFi Platforms Using On-Chain Credit Scores for Zero-Collateral Loans

-

Zeru Finance: Zeru introduces the ZScore, an on-chain credit score that reflects users’ reputation and activity within its ecosystem. By engaging in lending, borrowing, and timely repayments, users earn credit tokens, which can be used to secure zero-collateral loans. An insurance fund, the Protocol Controlled Value Reserve (PCVR), backs these loans to protect against defaults.

-

3Jane Protocol: 3Jane offers non-collateralized cryptocurrency lending by combining on-chain credit scores with traditional credit data. It assesses borrowers’ future cash flows and verifiable financial proofs, enabling instant USDC credit lines without requiring traditional collateral. The protocol also utilizes on-chain auctions and licensed debt collectors for risk mitigation.

-

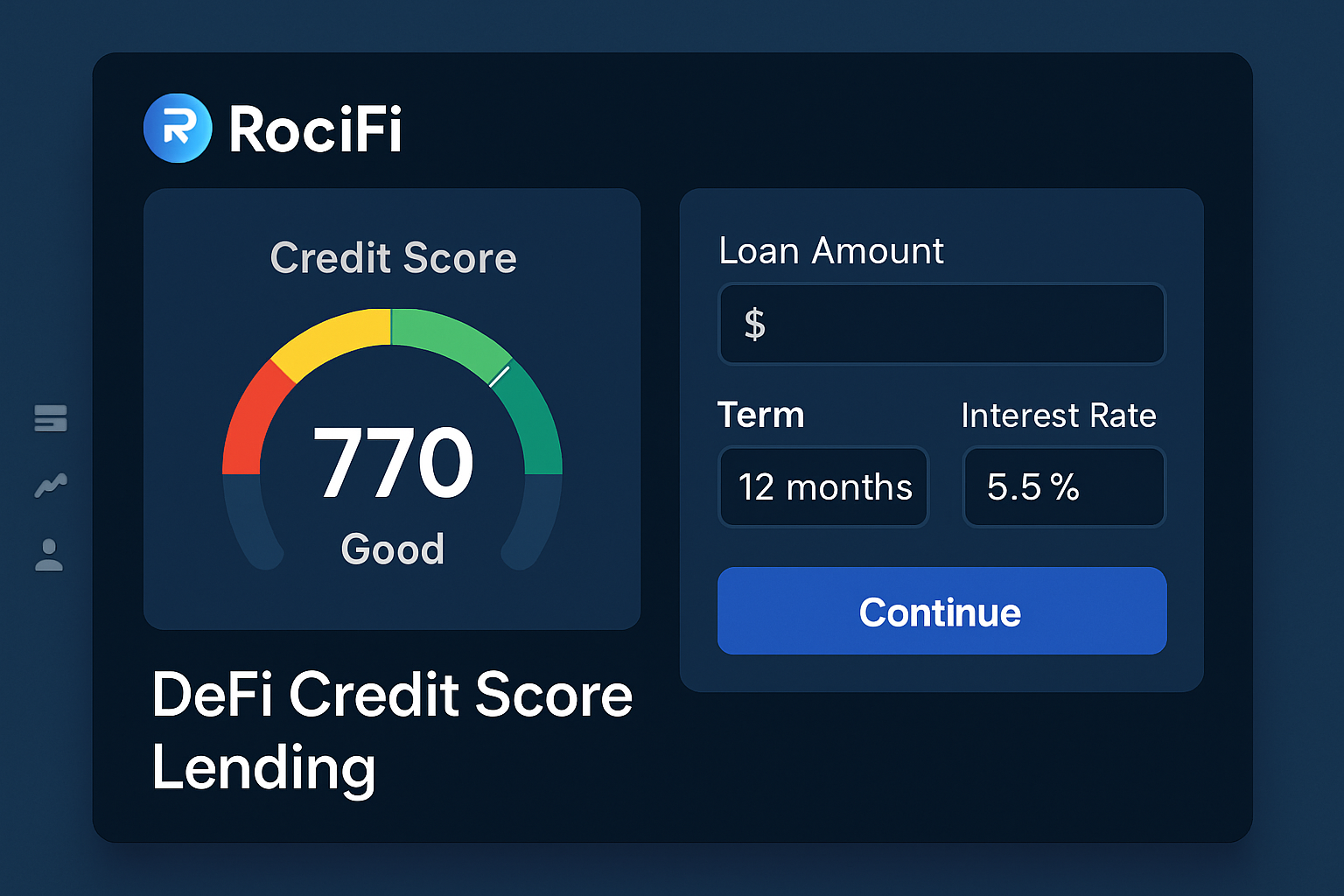

RociFi: RociFi leverages decentralized identity and on-chain reputation to enable under-collateralized and zero-collateral lending. The platform issues Non-Fungible Credit Scores (NFCS)—non-transferable tokens representing a user’s creditworthiness—allowing borrowers to access loans based on their blockchain activity and reputation.

Zeru Finance stands out with its ZScore system, rewarding positive protocol engagement and enabling users with strong reputations to access unsecured loans backed by an insurance fund (the Protocol Controlled Value Reserve). For full details on how Zeru’s ecosystem works, see their explainer at Zeru Finance.

3Jane Protocol takes a hybrid approach by blending on-chain and off-chain data. It evaluates future cash flows and even traditional credit information alongside wallet analytics to determine instant USDC borrowing limits, no collateral required. Their integration with licensed debt collectors via smart contracts adds another layer of risk management (source).

RociFi, meanwhile, issues non-transferable NFT-based Non-Fungible Credit Scores (NFCS) that reflect your blockchain reputation and enable under-collateralized or even zero-collateral borrowing opportunities (learn more here).

The Mechanics of Decentralized Credit Scoring in Practice

The engine behind these protocols is sophisticated yet elegant. By evaluating factors like repayment history, frequency and size of transactions, participation in governance or liquidity pools, and even social signals (via soulbound token credit scores), platforms can create nuanced risk profiles that evolve over time.

This dynamic scoring system means responsible borrowers are rewarded with better rates and higher limits, just like in traditional finance but without intermediaries or privacy trade-offs. Conversely, defaults lead to lower scores and higher future costs, creating natural incentives for good behavior.

Key Advantages of Decentralized vs Traditional Credit Scoring

-

Global Accessibility: Decentralized credit scoring enables anyone with a blockchain wallet to build a credit history and access lending services, bypassing geographic, bureaucratic, and documentation barriers common in traditional finance.

-

Transparency and Immutability: On-chain credit scores are based on publicly verifiable blockchain data, ensuring that credit assessments are transparent, tamper-proof, and resistant to manipulation—unlike opaque traditional credit bureaus.

-

Privacy and User Control: DeFi platforms often let users maintain control over their financial data, sharing only what’s necessary for credit assessment, whereas traditional credit scoring involves centralized agencies collecting and storing sensitive personal information.

-

Real-Time Credit Assessment: On-chain credit scores update dynamically based on users’ blockchain activity, enabling instant, up-to-date evaluations, while traditional credit scores can lag behind actual financial behavior.

-

Zero or Under-Collateralized Lending: Platforms like Zeru Finance, 3Jane Protocol, and RociFi use on-chain credit scores to offer loans with little or no collateral, improving capital efficiency and financial inclusion—something rarely possible in traditional banking.

-

Programmable Risk Management: DeFi protocols can automate risk mitigation—such as adjusting interest rates or limiting borrowing power—based on real-time credit score changes, while traditional systems rely on slower, manual processes.

This is only the beginning. As more protocols embrace wallet reputation engines as their primary DeFi trust layer, the landscape for unsecured lending will continue to expand, fueling inclusion and efficiency across the Web3 economy.

We’re witnessing the early stages of a financial revolution that brings real-world credit logic to the blockchain, but with a crucial twist: transparency and user empowerment are at its core. Unlike legacy systems where credit scores are hidden and difficult to challenge, decentralized credit scoring protocols allow users to see, verify, and even improve their scores in real time.

This shift isn’t just theoretical. For example, Zeru Finance lets users actively build their ZScore by participating in lending, borrowing, and repaying activities. The more responsibly you interact with the protocol, the more trust you earn, unlocking larger zero-collateral loans over time. Meanwhile, RociFi’s soulbound token credit scores (non-transferable NFTs) offer a new model for persistent wallet reputation that can’t be gamed or transferred.

Risk Management: How Protocols Safeguard Zero-Collateral Lending

Of course, removing collateral raises an obvious question: what happens if borrowers default? Here’s where smart contract automation and innovative insurance mechanisms come into play. Platforms like Zeru use dedicated insurance reserves (the PCVR) to cover losses from defaults without spreading risk across all users. Others, like 3Jane, trigger on-chain auctions for debt recovery, sometimes even involving licensed debt collectors.

This multi-layered approach is designed to keep protocols solvent while protecting honest borrowers from systemic shocks. If your wallet defaults on a loan, your on-chain credit score takes a hit, not just with one protocol but potentially across any integrated DeFi platform. This creates powerful incentives for responsible borrowing and repayment.

Top Risk Management Tools in Zero-Collateral DeFi Lending

-

On-Chain Credit Scores: Platforms like Zeru Finance and RociFi use on-chain credit scores to assess borrower risk by analyzing blockchain transaction history, DeFi activity, and wallet reputation. This transparent scoring system helps lenders gauge trustworthiness without traditional collateral.

-

Insurance Funds: Protocols such as Zeru Finance’s PCVR maintain dedicated insurance reserves that absorb losses from loan defaults, protecting lenders and ensuring the platform’s stability even when borrowers fail to repay.

-

Non-Fungible Credit Scores (NFCS): RociFi issues NFCS tokens—non-transferable digital assets representing a user’s on-chain creditworthiness. These tokens are used to determine borrowing limits and interest rates, incentivizing responsible repayment.

-

Hybrid Credit Assessment: 3Jane Protocol combines on-chain credit data with off-chain financial information, such as traditional credit scores and verifiable income, to create a comprehensive risk profile for each borrower.

-

On-Chain Debt Recovery Mechanisms: Platforms like 3Jane utilize on-chain auctions and partner with licensed debt collection agencies to recover non-performing loans, increasing the likelihood of repayment and reducing systemic risk.

What’s Next? The Road Ahead for DeFi Unsecured Lending

The momentum behind decentralized credit scoring is only accelerating. As more protocols adopt interoperable wallet reputation engines and begin sharing data through privacy-preserving means, we’re likely to see:

- Broader access: Users without large crypto holdings can finally access liquidity based on merit rather than wealth.

- Lower rates: Improved risk assessment means lenders can offer competitive rates without requiring heavy collateralization.

- Composability: Wallet reputation may become portable across DeFi apps, imagine building your score in one protocol and borrowing in another.

- Synergies with TradFi: Hybrid models like 3Jane’s could bridge off-chain and on-chain data for even more accurate scoring.

The implications reach far beyond crypto natives. Real-world businesses and underbanked populations could soon leverage their digital activity for affordable loans, no traditional bank account required. As these decentralized trust layers mature, expect increased capital efficiency and deeper liquidity pools throughout Web3.

Final Thoughts

The days of one-size-fits-all collateral requirements are numbered. By leveraging transparent on-chain data and innovative risk controls, DeFi unsecured lending is moving from theory into daily practice, offering new opportunities for both borrowers and lenders worldwide. The next wave of adoption will hinge on user education, robust privacy protections, and continued innovation in decentralized identity systems.