Traditional credit agencies have long dictated who gets access to financial opportunity, using centralized databases and rigid scoring formulas. But as the digital economy surges forward, decentralized credit bureaus are rewriting the rules of the game. These blockchain-powered platforms don’t just tweak the old systems – they flip them inside out, promising transparency, privacy, and global accessibility for billions. Let’s break down what sets decentralized credit bureaus apart from their legacy counterparts – and why this matters more than ever in today’s evolving financial landscape.

Centralization vs. Decentralization: Who Controls Your Data?

The core difference between traditional and decentralized credit scoring is who owns and controls your financial data. Traditional agencies like Equifax and Experian act as gatekeepers, collecting and storing your credit history in massive, centralized databases. This setup makes them prime targets for data breaches – as history has shown – and leaves individuals with little say over how their information is used or shared.

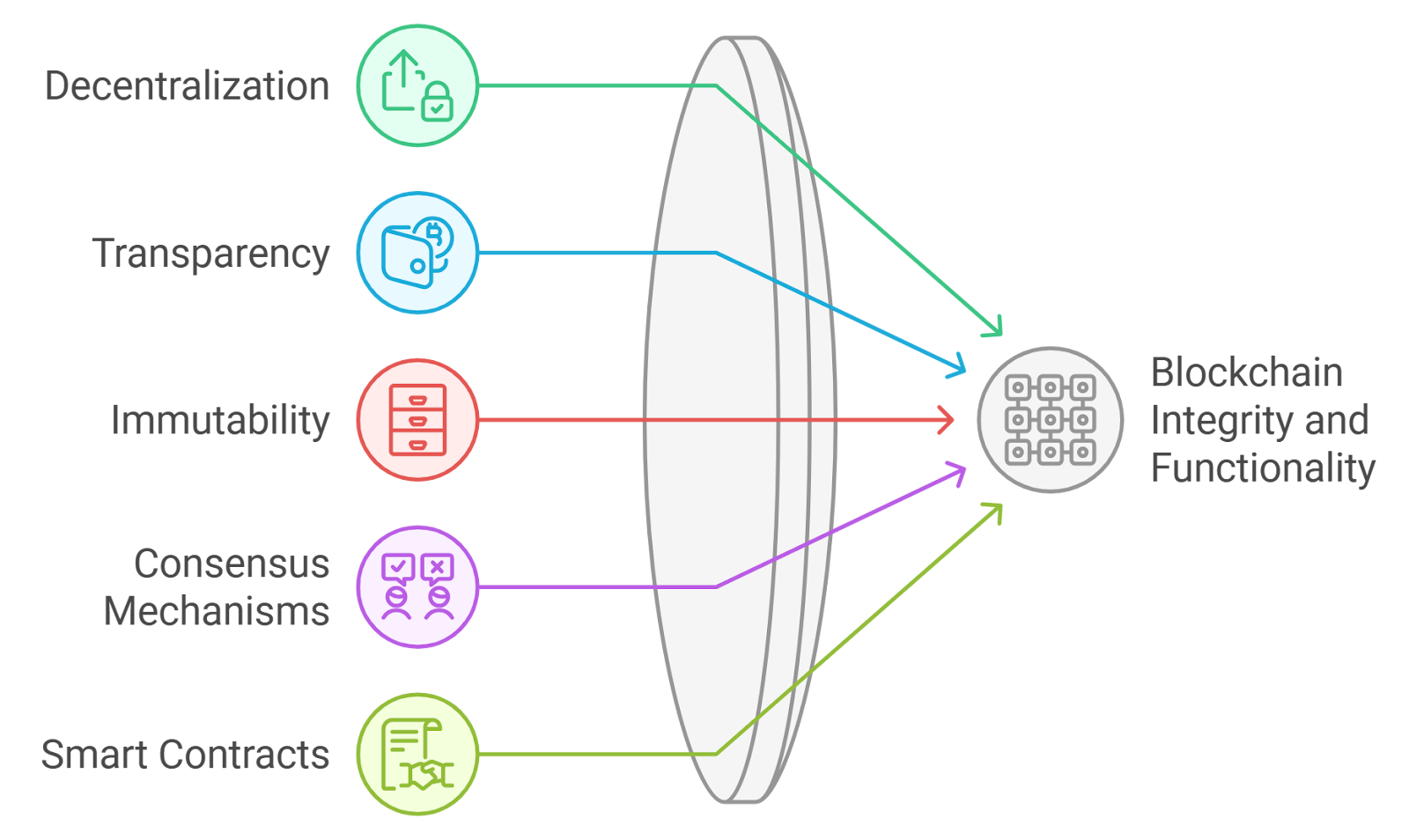

Decentralized credit bureaus flip this model on its head. Built on blockchain technology, these platforms record financial activities on distributed ledgers that are cryptographically secure and tamper-proof. No single authority controls the data; instead, users retain sovereignty over their information through private keys and decentralized identifiers (DIDs). This not only reduces the risk of hacks but also empowers individuals to decide who accesses their data – a seismic shift in personal privacy.

Transparency and Trust: Opaque Formulas vs. Open Algorithms

If you’ve ever tried to decipher your FICO score, you know how murky traditional credit scoring can be. Agencies use proprietary algorithms that are rarely disclosed to consumers or regulators, making it tough to challenge errors or understand what drives your score up or down.

Decentralized systems thrive on transparency. Blockchain’s public ledger means all scoring logic can be open source and auditable by anyone. Users see exactly which transactions influence their scores – whether it’s regular loan repayments, on-chain activity, or participation in DeFi protocols. This transparency builds trust among users and lenders alike while slashing opportunities for manipulation or bias.

Top 5 Benefits of Decentralized Credit Bureaus

-

Enhanced Data Privacy & Security: Decentralized credit bureaus leverage blockchain technology to store credit data across a distributed ledger, greatly reducing the risk of data breaches and unauthorized access compared to centralized databases used by traditional agencies.

-

Greater Consumer Control: Individuals have direct ownership and control over their financial data, often managed through decentralized identifiers (DIDs), enabling them to decide who can access their credit information.

-

Inclusive Credit Assessment: By incorporating alternative data sources—such as utility payments, rent history, and on-chain activity—decentralized bureaus can provide credit scores for people with little or no traditional credit history, expanding financial inclusion.

-

Transparency & Auditability: All credit transactions and scoring methodologies are recorded on a public blockchain, allowing users and regulators to verify data integrity and fairness, unlike the often opaque processes of traditional agencies.

-

Global Accessibility: Decentralized credit bureaus are not limited by national borders, enabling cross-border credit assessments and access to financial services for individuals worldwide, especially in underbanked regions.

Inclusivity and Alternative Data: Expanding Access to Credit

The biggest promise of decentralized credit bureaus is widening access to fair finance. Traditional agencies often exclude people with thin files – those without mortgages or lengthy banking histories. This leaves millions worldwide locked out of loans or forced into predatory lending arrangements.

Decentralized models cast a much wider net by incorporating alternative data sources like utility payments, gig economy earnings, remittance flows, even social signals from verified blockchain activity. By evaluating real-world behaviors rather than just formal banking records, these systems unlock new opportunities for underserved populations – from freelancers in emerging markets to digital nomads living off crypto wallets.

Yet, this shift to alternative data isn’t without its own challenges. While decentralized credit bureaus can tap into a broader spectrum of financial signals, questions remain around data accuracy and standardization. Not all alternative data sources are equally reliable or regulated, and integrating them into a robust, automated scoring system requires rigorous validation. Still, the momentum is clear: as more DeFi protocols and blockchain projects adopt these models, the pressure mounts on legacy agencies to innovate or risk obsolescence.

Another crucial distinction lies in user empowerment. In the traditional model, consumers often have little recourse if their credit report contains errors, disputes can drag on for months, with little transparency in the resolution process. Decentralized platforms flip this script by giving users direct oversight over their credit profile. Through cryptographic proofs and smart contracts, individuals can verify their transactions and contest inaccuracies in real time, no waiting on hold with a call center required.

Automation and Efficiency: Smart Contracts Replace Red Tape

Traditional credit agencies are notorious for slow processes and bureaucratic friction. Loan approvals can take days or weeks as paperwork crawls through centralized systems. In contrast, decentralized credit bureaus harness smart contracts to automate verification and scoring. This means faster decisions for borrowers and lenders alike, sometimes within minutes, while slashing operational costs across the board.

This efficiency isn’t just about speed; it’s also about fairness. Automated algorithms remove much of the human bias that plagues legacy systems, offering a level playing field regardless of geography or background. And because every step is recorded on-chain, there’s an immutable audit trail for every decision made.

How Smart Contracts Streamline Decentralized Credit Assessment

-

Automated Credit Evaluation: Smart contracts on platforms like Aave instantly assess borrower eligibility by analyzing on-chain transaction history and wallet activity, eliminating manual review delays.

-

Transparent Decision Logic: Protocols such as Compound use open-source smart contracts, allowing anyone to audit the rules and criteria used for credit scoring—unlike opaque traditional models.

-

Real-Time Alternative Data Integration: Platforms like Goldfinch leverage smart contracts to incorporate alternative data sources—such as repayment history and on-chain behavior—enabling more inclusive and dynamic credit assessments.

-

Self-Sovereign Identity Verification: Decentralized identity solutions, including SpruceID, use smart contracts to let users control and share their financial credentials securely, streamlining KYC without centralized gatekeepers.

-

Instant, Trustless Loan Execution: With protocols like TrueFi, smart contracts automatically execute loan approvals and disbursements based on pre-set criteria, reducing human error and increasing efficiency.

Security and Privacy: Resilience in a Digital Age

The world has seen high-profile breaches at major credit agencies that exposed sensitive data of millions. With cyber threats on the rise, security is non-negotiable. Decentralized credit bureaus leverage blockchain’s inherent resilience: distributed ledgers are nearly impossible to tamper with or take down thanks to their networked design.

Privacy also gets an upgrade. Instead of handing over your entire financial life to a single entity, you selectively share only what’s necessary for each transaction using zero-knowledge proofs or similar cryptographic tools. This minimizes exposure while maximizing control, a win-win for privacy-conscious users navigating an increasingly digital financial landscape.

The Road Ahead: Building Trust in Web3 Credit Markets

The rise of decentralized credit bureaus marks a paradigm shift with massive implications for individuals and institutions alike. As these platforms mature, expect ongoing debates around governance standards, interoperability between chains, and regulatory frameworks that balance innovation with consumer protection.

What’s certain is that blockchain-powered credit scoring is not just a technical upgrade, it’s a philosophical one. It puts power back into the hands of users while opening doors for millions who’ve been sidelined by legacy systems. For anyone navigating Web3 finance, whether you’re lending stablecoins or building new DeFi apps, understanding this transformation isn’t optional; it’s essential.