NFT lending is rapidly evolving, reshaping how digital assets are leveraged in the decentralized finance (DeFi) ecosystem. While NFTs (non-fungible tokens) originally gained traction as digital collectibles and art, their role as collateral for loans has become a key innovation. However, this new frontier also brings unique risks and challenges, especially when it comes to assessing borrower trustworthiness and managing the volatility of NFT-backed loans.

Why Credit Scores Matter in NFT Lending

Traditional DeFi lending protocols often require borrowers to over-collateralize their loans – sometimes by two or three times the loan amount – due to the lack of credit assessment tools. This high barrier limits participation, locking out many potential borrowers who might otherwise responsibly utilize their NFT holdings.

Enter on-chain credit scores: these blockchain-native assessments analyze wallet activity, borrowing history, repayment behavior, and even social signals to build a transparent risk profile for each user. By integrating these scores into NFT lending platforms, protocols can offer more flexible terms and lower collateral requirements without sacrificing security.

“Decentralized credit scoring calculates a borrower’s creditworthiness much like traditional systems – but with greater transparency and privacy controls. “

How On-Chain Credit Scoring Works for NFT Collateralization

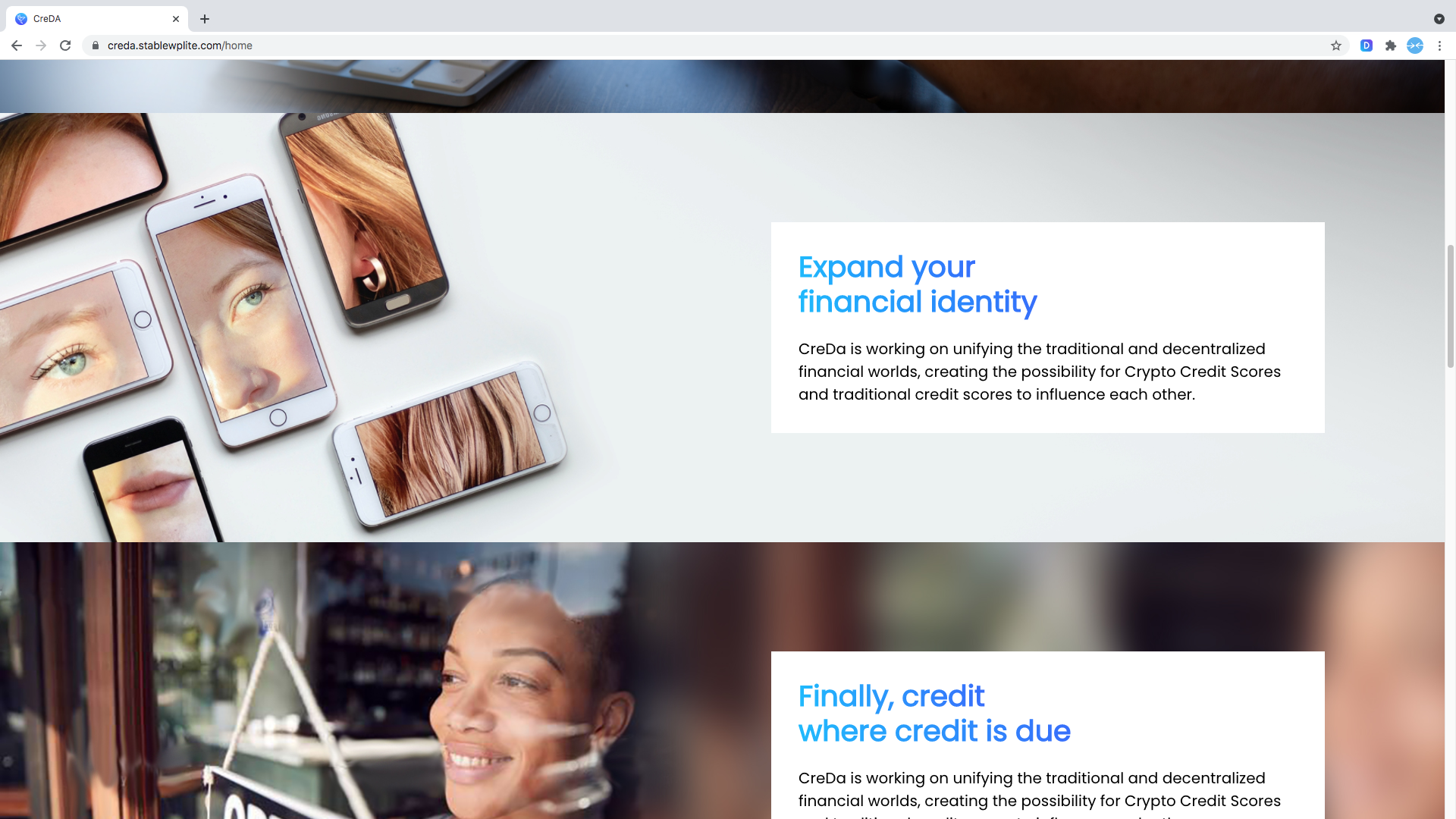

On-chain credit scores leverage blockchain analytics and decentralized data sources to evaluate user behavior across multiple protocols. For example, CreDA (Credit DeFi Alliance) uses AI models to analyze activities such as timely loan repayments, asset management habits, and overall financial interactions on-chain. The resulting Crypto Credit Score is then minted into a Credit NFT (cNFT), which acts as a verifiable credential within the DeFi ecosystem.

This cNFT can be presented to lending platforms like FilDA or ParaSpace to unlock preferential rates or access low- or even no-collateral loans. As long as your portfolio’s health score remains above a set threshold – calculated based on both your cNFT score and the quality of your collateralized NFTs – you avoid liquidation events that would otherwise threaten your digital assets.

Real-World Innovations: Bundled Collateralization and Portfolio Health Scores

The integration of on-chain credit scoring with advanced portfolio management features is redefining how risk is assessed in NFT lending. Platforms like ParaSpace now allow users to bundle multiple NFTs together as collateral under one loan agreement. Instead of tracking each asset individually for liquidation risk, these platforms generate an overall health score for the entire portfolio. As long as that score stays above critical thresholds, users retain control over all their NFTs – greatly reducing unnecessary liquidations during market volatility.

Key Benefits of On-Chain Credit Scores in NFT Lending

-

Reduced Over-Collateralization: Platforms like CreDA use on-chain credit scores to assess borrower risk, allowing for lower collateral requirements compared to traditional DeFi lending. This makes NFT-backed loans more accessible.

-

Improved Accessibility: On-chain credit scoring enables a wider range of users to participate in NFT lending by evaluating wallet behavior and transaction history, rather than relying solely on large collateral amounts.

-

Personalized Loan Terms: Borrowers with strong on-chain credit scores can access preferential interest rates and flexible repayment terms, as seen in CreDA’s partnership with FilDA.

-

Enhanced Risk Management for Lenders: Credit scoring mechanisms, such as ParaSpace’s health score system, help lenders better evaluate borrower risk and manage loan portfolios more effectively.

-

Greater Capital Efficiency: By using bundled collateralization and full-position leverage, platforms like ParaSpace allow users to maximize borrowing power without triggering immediate liquidation, as long as the portfolio health score remains strong.

-

Fostering Financial Inclusion: On-chain credit scores promote a more inclusive DeFi ecosystem by enabling users with limited traditional credit history to access NFT-backed loans based on their blockchain activity.

This approach not only increases capital efficiency but also makes borrowing against NFTs more accessible and less stressful for users who maintain good on-chain reputations.

As the NFT lending sector matures, the convergence of on-chain credit scores and innovative collateralization models is creating a more nuanced, data-driven approach to blockchain risk assessment. Instead of treating every borrower with a broad-brush policy, protocols now have the tools to reward responsible behavior and unlock financial opportunities for a wider range of participants.

For example, by leveraging decentralized credit scoring, platforms like FilDA can offer dynamic interest rates and flexible loan-to-value ratios based on each user’s unique profile. This means that borrowers with strong repayment histories and robust wallet activity may access loans with significantly lower collateral requirements, sometimes even approaching traditional finance standards. The result? A more inclusive ecosystem where NFT holders can tap liquidity without fear of punitive over-collateralization.

Challenges and Considerations

Despite these advances, several challenges remain. The volatility inherent in NFT valuations makes accurate pricing difficult, especially for rare or thinly traded assets. While bundled collateralization and health scores mitigate some risks, protocols must continue to refine their models to avoid systemic vulnerabilities.

Privacy is another area of focus. Although on-chain data is transparent by design, platforms are increasingly adopting privacy-preserving techniques, such as zero-knowledge proofs, to ensure sensitive information isn’t unnecessarily exposed while still enabling robust credit assessments. Additionally, cross-chain interoperability is becoming crucial as users operate across multiple blockchains and DeFi ecosystems.

Key Considerations for NFT-Backed Borrowers

-

Understand On-Chain Credit Scoring Platforms: Platforms like CreDA and ParaSpace assess your creditworthiness using on-chain activity, impacting your borrowing terms and collateral requirements.

-

Evaluate Collateral Valuation and Liquidity: The value and market liquidity of your NFT significantly affect loan eligibility and risk. Illiquid or volatile NFTs may lead to stricter terms or higher collateral ratios.

-

Monitor Your Portfolio Health Score: On platforms like ParaSpace, maintaining a strong health score across your collateralized assets reduces liquidation risk and may allow for more favorable loan terms.

-

Review Loan-to-Value (LTV) Ratios and Over-Collateralization: Even with credit scoring, many platforms still require you to provide collateral worth more than the loan. Compare LTV ratios and over-collateralization requirements across lending protocols.

-

Check for KYC and Compliance Requirements: Some protocols, especially those integrating with traditional finance, may require KYC (Know Your Customer) verification or proof of creditworthiness via self-sovereign identity solutions.

-

Assess Risk of Liquidation and Insurance Options: Understand the triggers for liquidation on your chosen platform and explore whether insurance products are available to protect your NFT collateral.

The Road Ahead: Expanding Access and Trust in DeFi

The integration of on-chain credit scores into NFT lending isn’t just about reducing collateral requirements, it’s about building trust in a decentralized world. By providing transparent, verifiable risk metrics, these systems empower both lenders and borrowers to make informed decisions without relying on opaque intermediaries or outdated TradFi norms.

Looking forward, expect continued growth in NFT collateralization solutions that blend advanced analytics with user-centric privacy controls. As protocols experiment with new forms of self-sovereign identity and interoperable credit attestations, we’ll see the barriers between traditional finance and Web3 continue to blur, unlocking trillions in value for the global decentralized economy (source).