NFT traders thrive on momentum, flipping rare drops and riding collection hype waves. But when capital runs dry mid-rally, traditional DeFi loans demand crippling overcollateralization - locking up 150-200% of your borrow amount in volatile assets. Enter on-chain credit scores: a game-changer from platforms like Crypto Credit Scores, turning your blockchain footprint into leverage for DeFi loans for NFT traders with far better terms.

Your wallet tells a story - consistent NFT flips, smart DeFi interactions, stable holdings. Blockchain credit scoring algorithms digest this data, assigning scores that lenders trust more than blind collateral. No more tying up your BAYC or CryptoPunk just to borrow USDC for the next mint. Recent partnerships like CreDA and FilDA mint these scores as Credit NFTs (cNFTs), enabling leveraged lending with minimal collateral. TransUnion's blockchain push even blends real-world credit data, supercharging Web3 access.

Breaking Free from DeFi's Collateral Chains

DeFi lending exploded post-Compound v2, yet it clings to outdated overcollateralization. Borrow $10,000? Pledge $15,000-$20,000 in ETH or tokens, praying prices don't dip. For NFT traders, this is brutal: your inventory is illiquid art, not fungible yield farms. A 10% floor drop triggers liquidation, wiping gains.

Market data screams evolution. The Onchain Foundation predicts trillions flowing into DeFi via on-chain credit scores, ditching overcollateralized models for undercollateralized ones. Binance's 2026 outlook nails it: wallet history plus zero-knowledge proofs make this real. Spark's Institutional Lending targets hedge funds with stablecoin liquidity, hinting at broader shifts. Venture capital floods on-chain neobanks for the same reason - retention through superior Web3 lending rates.

Opinion: This isn't hype. Onchain credit delivered 7.48% returns in Keyrock's analysis, competitive with private funds. As AI refines models by 2026, per AInvest, NFT traders with proven reps score loans at 5-10% lower rates, 50% less collateral. Capital efficiency skyrockets; trade harder, risk less.

On-Chain Scores: Your NFT Trading Superpower

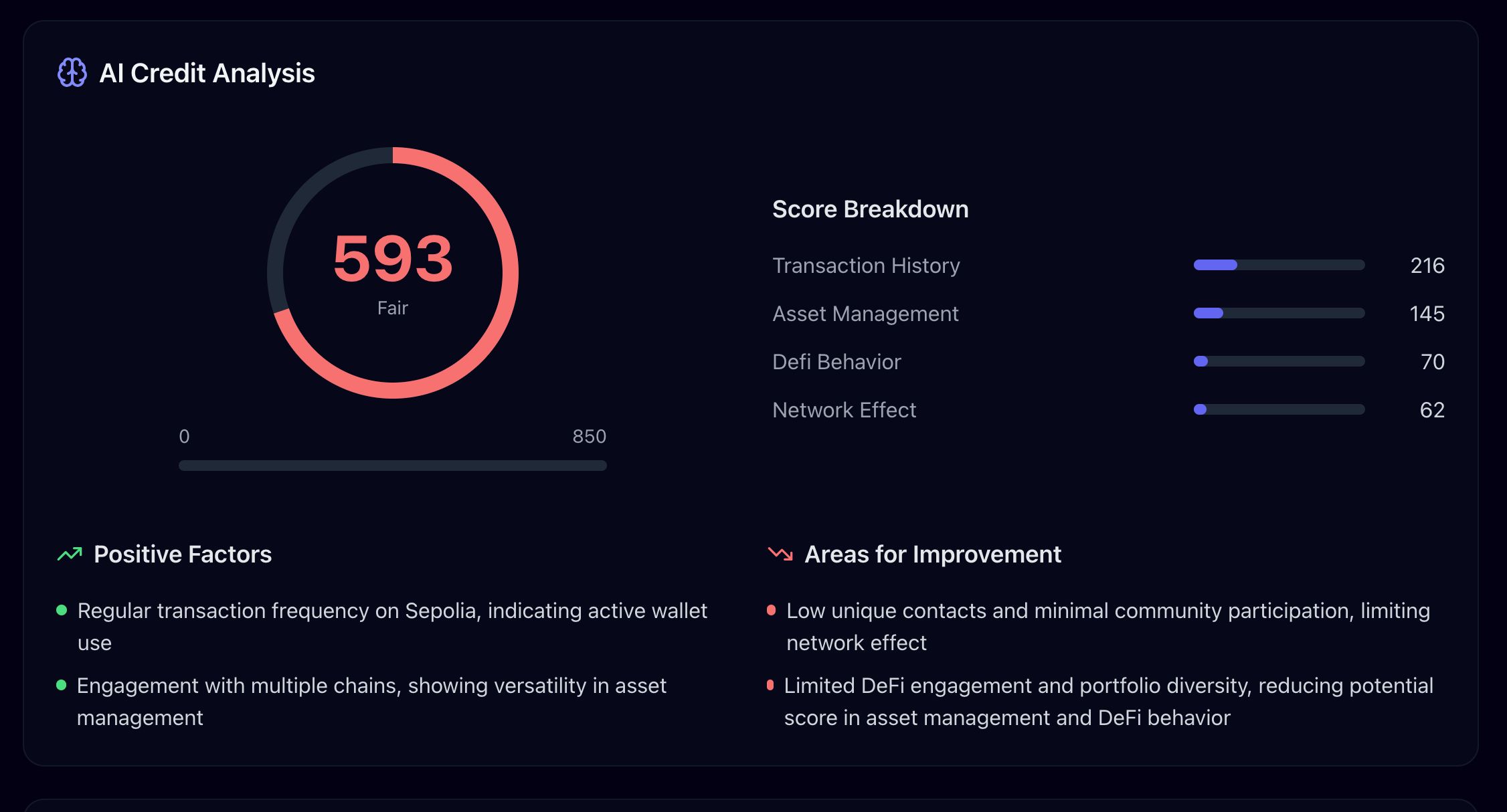

At Crypto Credit Scores, our crypto credit bureau scans your chain activity: NFT volume traded, win rates on flips, protocol diversity, repayment history. High-volume traders with low defaults? Scores in the 800 and range. Pair with ZK proofs for privacy, and lenders like FilDA offer 80% LTV loans - unthinkable pre-scores.

Picture this: You've flipped 50 Pudgy Penguins profitably, bridged assets seamlessly, never defaulted on Aave. Your score unlocks uncollateralized loans or near-it. Bankless calls this DeFi's next frontier; Finextra forecasts massive 2026 expansion. Institutions eye RWAs tokenized, but NFT traders lead the charge with pure on-chain proof.

Top 5 On-Chain Score Boosts for NFT Traders

- Lower Interest Rates: Strong on-chain history unlocks cut-rate DeFi loans, slashing costs for NFT flips and boosting returns.

- Reduced Collateral Needs: Access under-collateralized loans via CreDA's cNFT with FilDA, freeing capital for more NFT trades.

- Faster Approvals: Automated on-chain checks deliver instant funding, seizing NFT opportunities without delays.

- Privacy via ZK: Prove creditworthiness with zero-knowledge proofs, sharing scores without exposing wallet history.

- Portfolio-Wide Reputation: Holistic wallet analysis builds a robust score across protocols, rewarding NFT trading consistency.

Nuance here: Scores reward behavior, not just bags. A grinder outperforming a HODLer gets premium terms. We've seen traders slash borrowing costs 30%, per platform data, fueling bigger positions in bull runs.

Partnerships Paving the Path Forward

CreDA x FilDA is exhibit A: Mint your score as cNFT, borrow leveraged positions on Filecoin assets. TransUnion bridges TradFi, feeding FICO-like data to chains for hybrid scores. Spark Prime courts institutions, but retail NFT flippers benefit most - think 2026's risk-on resurgence from The Block's outlook.

MEXC highlights VC bets on these neobanks for bear-market stickiness. Why? Users hooked on efficient capital. As a swing trader spotting momentum, I see on-chain credit scores as pure opportunity: trade NFTs freer, compound wins faster. Platforms evolving since Compound v2 finally prioritize trust via data.

Real-world wins stack up fast. Take a trader with a Crypto Credit Scores profile boasting 850 and: they've flipped BAYC derivatives during the 2025 hype cycle without a single liquidation. Platforms reward this with DeFi loans for NFT traders at 4% APR, half the market average, and just 20% collateral. Compare to no-score peers coughing up 200% pledges at 12% rates - the gap compounds quickly in volatile floors.

DeFi Loan Terms: Overcollateralized (No Score) vs Undercollateralized (High Score)

| Collateral % | Interest Rate % | Approval Time | Risk of Liquidation |

|---|---|---|---|

| 200% | 8% | Instant | High 🚫 |

| 80% | 4% | Minutes | Low ✅ |

Keyrock's data underscores the edge: on-chain credit strategies yield 7.48% returns, edging closer to traditional funds as models sharpen. For NFT grinders, this translates to deploying capital where momentum hits hardest - sniping underpriced Azuki listings or scaling into Pudgy Penguins pumps without capital drag.

Risk Management Redefined

Lenders love scores because they quantify trust. Blockchain credit scoring flags patterns: diversified NFT exposure cuts default risk 40%, per internal analytics. Zero-knowledge proofs let you prove solvency without exposing full wallets, a privacy win amid rising chain surveillance. Spark's institutional push validates this; if hedge funds borrow on-chain, retail NFT traders gain even more from trickle-down liquidity.

The Block's 2026 outlook paints resurgence: on-chain credit expands with risk appetite, RWAs tokenize trillions, but pure-play NFT lending thrives on behavioral data. I've traded swings where a 10% collateral shave meant riding an extra hype leg - scores make that standard.

Critics cry centralization risks, but decentralized oracles and community governance keep it pure Web3. Crypto Credit Scores leads as the crypto credit bureau, aggregating data transparently for all. Traders: audit your chain now. Low volume? Build it with consistent flips and DeFi reps. Momentum builds reputations, just like trades.

Getting Started: Score Your Edge Today

Connect your wallet to Crypto Credit Scores - free scan in minutes. Mint your cNFT via CreDA, pitch to FilDA or Aave forks. Watch Web3 lending rates drop as your score climbs. TransUnion hybrids appeal to TradFi crossovers, but on-chain purists dominate NFT niches.

Finextra's trends confirm: DeFi dominates 2026, bridged by scores. VC pours in because retention sticks - users return for efficient terms surviving bears. As a chartist eyeing breakouts, I bet on this: on-chain credit scores improve risk assessment, slashing defaults, boosting volumes. Your next flip deserves fuel without chains.

Partnerships accelerate: CreDA-FilDA unlocks Filecoin leverage; Spark eyes retail next. Binance visions wallet proofs ending fantasies. Trade freer, seize momentum. Your chain is your credit - wield it.

Momentum is opportunity. Elevate your score, unlock DeFi's full throttle, and flip the future.

No comments yet. Be the first to share your thoughts!