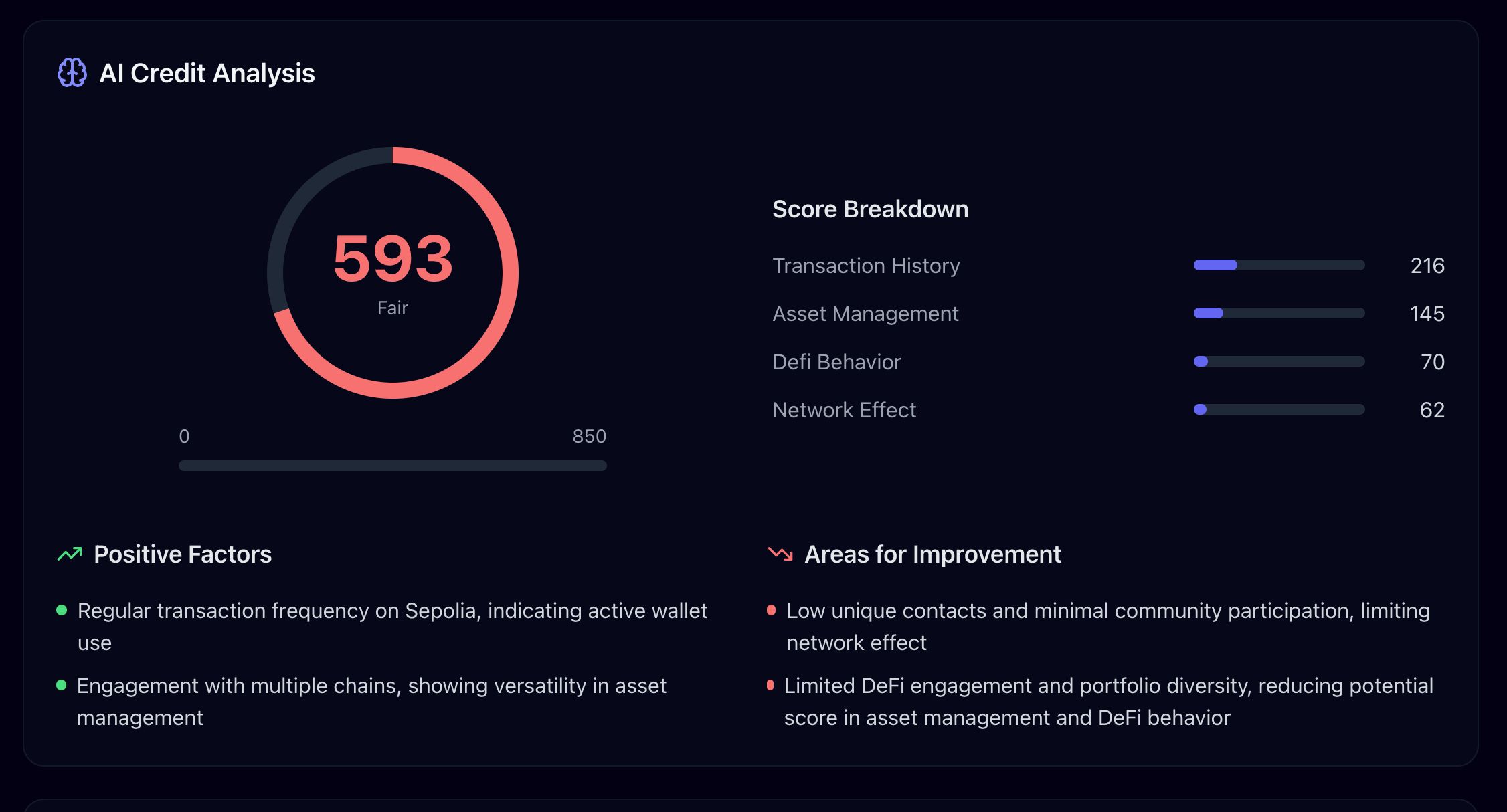

In the bustling world of decentralized finance, every cryptocurrency purchase ripples through more than just your wallet; it shapes your on-chain credit score, a vital metric for unlocking DeFi opportunities. Unlike traditional credit scores hidden behind opaque bureaus, on-chain scores draw directly from your blockchain activity, offering transparency but demanding discipline. As platforms like Crypto Credit Scores pioneer this space, understanding how buying crypto influences your DeFi lending scores becomes essential for savvy users navigating Web3.

Decoding On-Chain Credit Scores in DeFi

On-chain credit scores represent a paradigm shift from legacy systems, leveraging blockchain data to evaluate creditworthiness without centralized gatekeepers. Platforms analyze transaction histories, asset holdings, and interaction patterns across protocols to generate scores that power undercollateralized lending. According to insights from the Onchain Foundation, these scores could unlock trillions in DeFi by enabling alternatives to overcollateralized loans, fostering broader financial inclusion.

Traditional crypto loans sidestep credit checks and bureau reporting, as noted by APX Lending, but DeFi evolves this model. Here, your entire blockchain activity scoring tells the story: consistent behaviors signal reliability, while volatility raises flags. I see this as a double-edged sword; it empowers users with control over their financial narrative but requires mindful on-chain habits to avoid unintended dents in your profile.

Transaction History: The First Layer of Impact

When you buy crypto, you're etching a record into the immutable blockchain ledger. Regular, responsible purchases demonstrate financial stability and activity, potentially elevating your on-chain credit score impact. For instance, steady accumulation via dollar-cost averaging on reputable exchanges can portray you as a prudent actor, much like timely payments bolster FICO scores.

Yet, the flip side looms large. Erratic buying sprees, especially during hype cycles, or frequent small trades hinting at speculation, might flag you as high-risk. DeFi protocols, drawing from sources like HashKey's analysis, prioritize objective on-chain data for transparent evaluations. In my experience managing hybrid portfolios, this mirrors how volatility in holdings correlates with risk-adjusted returns; the blockchain simply quantifies it publicly.

Crypto Buy Impacts on Credit

- Steady buys of crypto like BTC or ETH demonstrate consistent financial activity and stability, positively boosting your on-chain credit score by showing reliability to DeFi protocols.

- Volatile trades with frequent high-risk buys signal erratic behavior, negatively impacting your score as they suggest poor risk management in on-chain analysis.

- Diverse assets holdings (e.g., BTC, ETH, stablecoins) reflect financial strength and collateral potential, enhancing creditworthiness in DeFi lending.

- Meme coins dominance indicates high volatility and speculation, viewed as risky by on-chain scorers, lowering your credit profile.

- Long-term holds (HODLing) build a history of responsible ownership, positively signaling low risk and improving loan eligibility.

- Quick flips (rapid buys/sells) mimic gambling patterns on-chain, harming your score by highlighting short-term speculation over stability.

Asset Holdings and Collateral Potential

Beyond transactions, the assets you acquire matter profoundly. Building a diversified portfolio of blue-chip cryptos enhances perceived financial strength, signaling collateralization readiness for loans. This boosts your score, as protocols view ample holdings as a buffer against defaults, aligning with Galaxy's views on stablecoins and DeFi credit creation.

Conversely, amassing volatile or low-liquidity tokens could undermine your standing. DeFi risks, highlighted by the Bank for International Settlements, underscore that while decentralization promises freedom, on-chain visibility demands caution. Owning substantial, stable assets not only pads your score but positions you for favorable borrowing terms, a nuance often overlooked by newcomers chasing quick gains.

Thoughtfully curating purchases thus becomes a strategic lever. Pair this with repayment diligence and protocol interactions for holistic score improvement, setting the stage for deeper DeFi engagement.

Deeper DeFi engagement hinges on how your crypto buys integrate with loan repayments and protocol usage. A strong purchase history alone won't suffice; protocols scrutinize repayment patterns to gauge reliability. Timely repayments after borrowing against your holdings reinforce a positive crypto purchases credit score trajectory, much like consistent deposits build trust in traditional banking.

Repayment Patterns: Amplifying Purchase Signals

Once you've acquired assets, deploying them as collateral in DeFi lending protocols tests your score's resilience. Successful repayments, especially on undercollateralized loans enabled by advanced scoring, elevate your profile. Insights from Hedera highlight how smart contracts facilitate selective lending, where your full blockchain activity scoring informs rates and limits. In my portfolio management practice, I've observed that users prioritizing low-leverage borrows post-purchase maintain superior scores, avoiding liquidation spirals that tarnish reputations on-chain.

Neglect this, however, and even prudent buys falter. Defaults or near-misses, visible forever on the blockchain, can suppress your score for extended periods. GARP's risk management lens on DeFi emphasizes trustless anonymity, yet reputational credit emerges from patterns; erratic repayments undercut the stability your purchases aim to project.

Strategies to Boost On-Chain Credit

- Dollar-Cost Average Stable Assets: Regularly purchase USDC or DAI via platforms like Uniswap to build a consistent transaction history, signaling stability to on-chain scoring models.

- Repay Loans Promptly to Build History: Borrow against your crypto in MakerDAO and repay on time, as on-chain repayment records directly enhance your creditworthiness in DeFi.

- Diversify Across Blue-Chips Before Lending: Accumulate BTC, ETH, and wstETH before supplying liquidity to money markets, showcasing diversified, low-volatility holdings.

Navigating Risks and Building Resilience

Crypto purchases carry inherent risks that protocols factor into scores. Volatility in asset values can trigger liquidations, indirectly harming your standing. Bruegel's critique of DeFi as 'good technology, bad finance' rings true here; decentralized loans bypass basics like credit checks, but on-chain scores impose market discipline. Yellow. com's explanation of crypto credit ratings shows how risk scoring has matured, penalizing heavy exposure to speculative tokens bought in frenzy.

To counter this, adopt a measured approach. Accumulate during dips, hold through cycles, and avoid overextending into illiquid assets. Yeshiva University's take on crypto-native scores underscores parallels to traditional models, where financial inclusion demands balanced behavior. Thoughtful purchasing, paired with monitoring tools from platforms like Crypto Credit Scores, mitigates downsides while capitalizing on upsides.

As on-chain metrics evolve, they promise trillions in unlocked capital per the Onchain Foundation, shifting DeFi toward sustainable growth. Your buying habits today forge tomorrow's access, demanding vigilance in this transparent arena.

Optimizing for the Web3 Credit Bureau Era

Platforms serving as Web3 credit bureaus aggregate vast on-chain data for nuanced DeFi lending scores. Beyond buys, they weigh network effects: cross-protocol consistency, governance participation, and even stablecoin usage per Galaxy's analysis. I advocate treating your wallet as a portfolio under perpetual audit; curate purchases with an eye on holistic impact.

Start small: track your score via dashboards, adjust based on feedback. Over time, this discipline yields lower rates, higher limits, and novel opportunities like undercollateralized credit. In a space where every transaction counts, intentional buying transforms from mere acquisition to score-building mastery. Crypto Credit Scores equips you with these insights, bridging blockchain activity to real financial empowerment.

No comments yet. Be the first to share your thoughts!