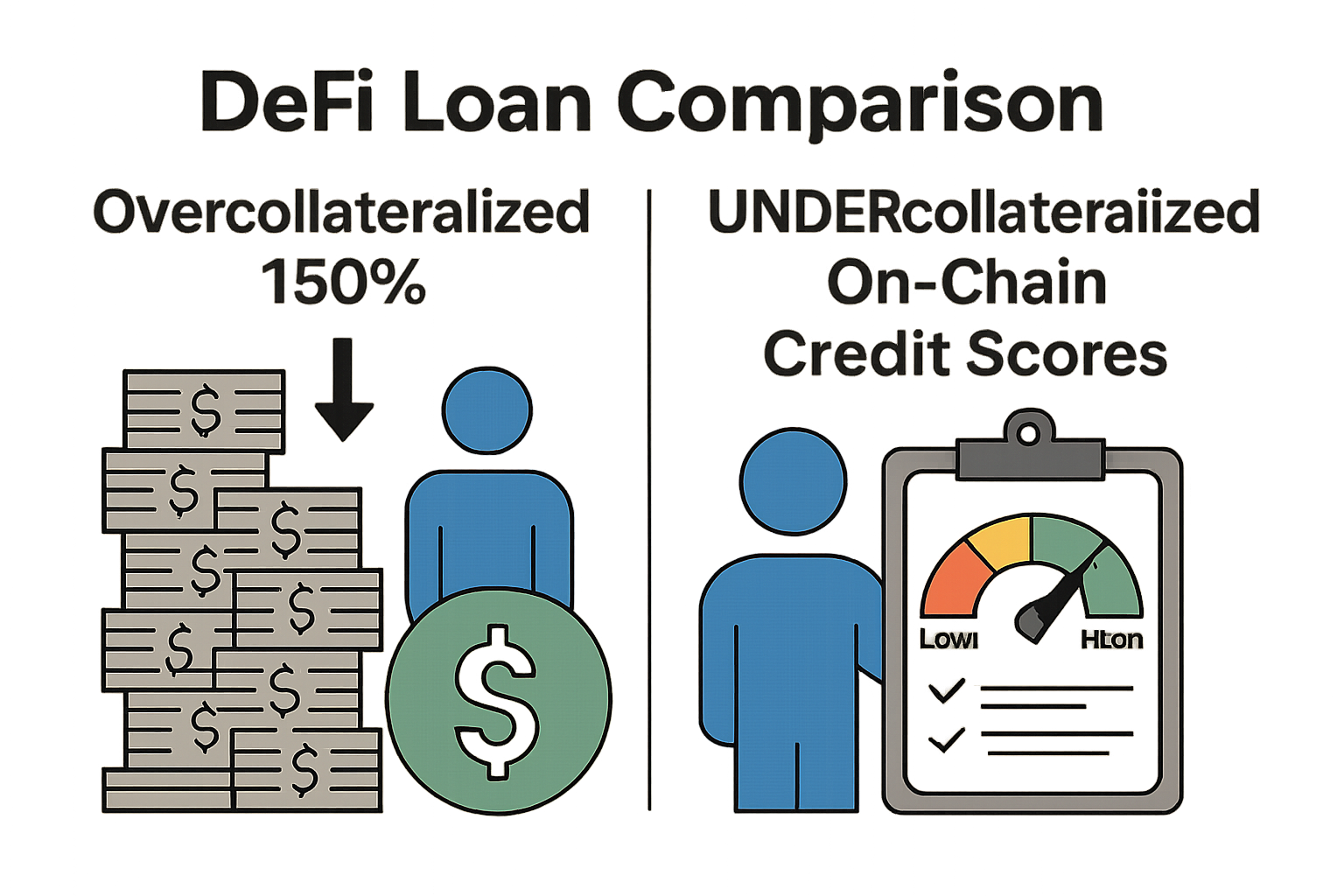

Imagine wanting to borrow $1,000 in DeFi but having to lock up $1,500 worth of crypto just to get started. That's the reality for most borrowers today, a system designed to shield lenders from defaults but one that ties up capital and sidelines countless users. On-chain credit scores are flipping this script, slashing collateral needs from 150% overcollateralization down to undercollateralized levels by turning blockchain history into a trusted risk signal. As someone who's analyzed both TradFi credit models and DeFi protocols, I see this as the bridge we've needed to make decentralized lending as efficient as centralized banks, without the gatekeepers.

DeFi's growth has been explosive, with total value locked hitting records amid low rates and innovative structures like collateralized loan obligations. Yet, the core lending mechanic remains rigid: overcollateralization. Platforms demand borrowers deposit more value than they borrow, often 150% or higher, to buffer against volatility. This protects lenders in a trustless environment, but it creates massive inefficiencies. Capital sits idle, opportunity costs soar, and only those with surplus assets can participate. Small holders or new entrants? They're often locked out, limiting DeFi's promise of financial inclusion.

The Collateral Trap Holding DeFi Back

Overcollateralization made sense in DeFi's early days. Without centralized credit checks, protocols like Aave or Compound relied on crypto deposits exceeding loan amounts. A borrower seeking $10,000 in stablecoins might stake $15,000 in ETH, praying prices don't tank before repayment. Defaults trigger liquidations, but the excess collateral cushions lenders. The downside? Capital efficiency suffers. That $15,000 isn't earning yield elsewhere; it's frozen as insurance.

Recent data underscores the scale. Studies show high-reputation users could see collateral requirements drop by 40% with better risk signals. Yet without them, DeFi lending stays capital-intensive, deterring retail users and stifling growth. Enter on-chain credit scores from platforms like Crypto Credit Scores, our Web3 credit bureau. These scores draw from immutable blockchain data, offering a privacy-preserving alternative to personal identities.

How On-Chain Credit Scores Work Their Magic

At their core, on-chain credit scores are dynamic ratings tied to wallet addresses, not names or SSNs. They analyze a wallet's full transaction history: repayment track records, borrowing frequency, interaction diversity across protocols, even liquidity patterns. Machine learning models weigh these factors to predict default risk, much like FICO does for banks but fully decentralized and transparent.

Privacy is baked in. Scores are pseudonymized, assessable via wallet without KYC. Platforms like Clearpool and ARCx's DeFi Passports exemplify this. ARCx users earn scores from on-chain behavior, unlocking loans with reduced collateral. Huma Finance's on-chain credit systems further decentralize lending, using blockchain-native data for real-time assessments. No more one-size-fits-all 150%; scores enable tailored terms.

This isn't hype. Moody's rated on-chain credits signal institutional buy-in, while Chainlink's DECO tech secures off-chain data feeds for hybrid models. Borrowers build scores organically through responsible activity, fostering a virtuous cycle of trust and access.

Real-World Shifts: Cutting Collateral in Action

Let's break it down with numbers. Traditional DeFi demands 150-200% collateral. High on-chain scores drop this to 100-120%, and top tiers approach undercollateralized territory below 100%.

| Score Tier | Collateral Ratio | Example Platforms |

|---|---|---|

| Low | 150-200% | Aave, Compound |

| Medium | 120-150% | Clearpool |

| High | Under 100% | ARCx, Sky Protocol |

ARCx's DeFi Passports let strong scorers borrow with far less locked capital, boosting efficiency. TechRxiv research confirms 40% reductions for reputable wallets. Galaxy Research notes DeFi TVL surges tied to these risk-managed approaches, with protocols like Grove pioneering $1B CLOs backed by on-chain signals.

Smart contracts automate it all: higher scores mean lower LTV ratios, softer liquidations, dynamic rates. Lenders win with better risk pricing; borrowers gain freedom. This evolution, powered by crypto credit scoring, positions DeFi to capture trillions, as Onchain predicts for uncollateralized loans.

Picture a DeFi borrower today: a mid-tier wallet holder with consistent repayments but modest holdings. Under legacy rules, they're stuck overcollateralizing at 150%, barely scraping by. With a solid on-chain score, that same user accesses loans at 80% collateral or less, freeing up assets to farm yields elsewhere. This isn't just math; it's empowerment. Lenders, too, refine their portfolios, channeling funds to low-risk borrowers while charging premiums to riskier ones. The result? A thriving ecosystem where capital flows smarter.

Risk Without the Roulette: Smarter Protections

Critics worry undercollateralized loans invite chaos, but on-chain credit scores layer in safeguards that traditional overcollateralization can't match. Scores incorporate real-time signals like wallet liquidity, cross-protocol health, and even social graph interactions from platforms experimenting with on-chain profiles. TechRxiv's findings back this: reputable wallets slash collateral by 40% without spiking defaults. Protocols blend this with oracles for hybrid verification, as Chainlink's DECO demonstrates, piping secure off-chain data into smart contracts.

Dynamic adjustments keep things tight. A borrower's score dips from volatile trades? Collateral requirements nudge up automatically, interest ticks higher. Lenders sleep easier knowing risk is priced continuously, not statically. Galaxy Research highlights this in DeFi's TVL boom, where risk-managed lending like Sky Protocol's Grove $1 billion CLO leverages Moody's-rated on-chain credits for scale.

Traditional DeFi Lending vs. On-Chain Credit Scored Lending

| Risk Metric | Traditional (150% Collateral) | On-Chain Scores |

|---|---|---|

| Default Protection | Overcollateralization ensures lender recovery on liquidation | Precise risk assessment via on-chain data enables undercollateralized loans with low defaults 📊 |

| Capital Efficiency | Low: Borrowers lock 150%+ assets, limiting usable capital | High: Dynamic collateral reduction (e.g., 40% less for high scores) unlocks more funds 💰 |

| Borrower Access | Limited to those with excess collateral | Broadened: Based on wallet history/reputation, includes uncollateralized users 🌐 |

| Default Rate Reduction | Baseline: Relies on liquidation only | Significant: Historical patterns and scores lower defaults via better selection 🔻 |

I've consulted for fintechs transitioning to Web3, and the data convinces me: crypto credit scoring isn't a gimmick. It's the analytical backbone enabling DeFi undercollateralized loans. Platforms reduce DeFi collateral dynamically, turning wallet histories into balance sheets banks envy.

Case Study Spotlight: ARCx and Beyond

Take ARCx's DeFi Passports. Users build scores through on-chain activity, earning tiered access. A high scorer borrows against 70% collateral, where others need 150%. Clearpool mirrors this in its marketplace, matching institutional lenders with scored borrowers. Huma Finance pushes further, fully on-chain credit for seamless borrowing. These aren't outliers; they're the vanguard. Mitosis University details how protocols fuse on-chain and off-chain data for precision scoring, issuing undercollateralized loans safely.

Block3 Finance notes 2025's on-chain identity wave reshaping borrowing. No more blind overcollateralization; lenders see proven payers. Borrowers without TradFi histories shine, their blockchain ledger speaking louder than any credit report.

Challenges persist, sure. Score gaming via sybil attacks or short histories demand vigilance. Solutions emerge: zero-knowledge proofs for privacy, multi-chain aggregation for robustness. Crypto Credit Scores, as a Web3 credit bureau, tackles this head-on with audited models. The payoff? Trillions inbound, per Onchain's forecast, as onchain lending collateral requirements plummet.

Geopolitics and rates favor this shift too. With TradFi tightening, DeFi's transparent risk tools draw capital. Hedera's lending guides show users picking markets wisely, amplified by scores.

Responsible builders prioritize this. Start tracking your wallet's score today; engage protocols, repay promptly. Watch as on-chain credit scores unlock doors once bolted shut. DeFi matures not by mimicking banks, but surpassing them through data democracy. The collateral era fades; efficiency reigns.

No comments yet. Be the first to share your thoughts!