Imagine wanting to borrow in DeFi but being forced to lock up $150,000 worth of crypto just to snag a $100,000 loan. That's the reality for most today, with Ethereum hovering at $3,032.64, making every overcollateralized position feel like dead capital. On-chain credit scores are flipping this script, paving the way for undercollateralized DeFi loans that trust your wallet's track record over bloated deposits. At Crypto Credit Scores, we're at the forefront, turning blockchain footprints into financial superpowers.

These scores analyze your on-chain behavior - think transaction patterns, DeFi interactions, and asset management - to gauge trustworthiness without peeking into your off-chain life. No more excluding newcomers or those light on holdings; it's about proven reliability unlocking real capital efficiency.

Why Overcollateralization Stifles DeFi Growth

DeFi's flagship lending protocols like Aave and Compound demand borrowers post collateral exceeding loan value by 150% or more. It's a smart hedge against volatility - after all, with ETH dipping to $3,026.15 in the last 24 hours - but it ties up billions in idle assets. Borrowers can't maximize their stacks, lenders face liquidation risks from price swings, and the whole ecosystem misses out on trillions in untapped liquidity. On-chain credit scores cut through this by introducing nuance to risk assessment, letting strong performers borrow with just 100% or even less collateral.

This shift isn't hype; it's backed by protocols already live. Projects like Crediflex use dynamic loan-to-value ratios based on your on-chain credit scores, rewarding consistent repayers with better terms. Suddenly, that $3,032.64 ETH you hold works harder for you.

Decoding On-Chain Credit Scores

At their core, on-chain credit scores are like a blockchain CV for your wallet. They crunch data from public ledgers: repayment history, borrowing frequency, wallet age, even cross-protocol engagement. Advanced models, sometimes powered by AI, assign probabilistic risk scores - think OCCR Score from recent research - without compromising privacy via zero-knowledge proofs.

What sets them apart from FICO? Immutability and transparency. Lenders verify scores on-chain, slashing fraud, while borrowers build credit through everyday DeFi use. Platforms like ours at Crypto Credit Scores aggregate this data securely, serving it to protocols for instant underwriting. The result? Loans issued in minutes, not days, with terms tailored to your digital footprint.

Ethereum (ETH) Price Prediction 2026-2031

Forecast driven by DeFi growth from on-chain credit scores enabling undercollateralized loans, boosting capital efficiency and TVL

| Year | Minimum Price | Average Price | Maximum Price | YoY % Change (Avg) |

|---|---|---|---|---|

| 2026 | $2,800 | $4,800 | $7,200 | +58% (from 2025) |

| 2027 | $3,900 | $6,700 | $10,000 | +40% |

| 2028 | $4,800 | $9,000 | $14,000 | +34% |

| 2029 | $6,000 | $11,500 | $18,000 | +28% |

| 2030 | $7,500 | $14,500 | $23,000 | +26% |

| 2031 | $9,000 | $18,500 | $30,000 | +28% |

Price Prediction Summary

Ethereum's price is forecasted to experience substantial growth from 2026-2031, propelled by DeFi innovations like on-chain credit scores from protocols such as Crediflex, Credora, and Teller Finance. These enable undercollateralized loans, unlocking trillions in liquidity and enhancing ETH demand as the leading DeFi chain. Average price could surge over 500% from current $3,033 levels by 2031 amid bull cycles, adoption, and tech upgrades.

Key Factors Affecting Ethereum Price

- DeFi TVL explosion from undercollateralized lending improving capital efficiency

- On-chain credit scoring (e.g., OCCR Score, Teller with Chainlink) expanding user base

- Ethereum's L1 dominance in DeFi protocols like Aave, Compound, Morpho

- Market cycles aligned with BTC halvings and institutional inflows

- Regulatory progress fostering mainstream adoption

- Scalability upgrades (e.g., L2s) supporting higher throughput

- Risks: Competition from L1s, macroeconomic downturns, oracle/security issues

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis. Actual prices may vary significantly due to market volatility, regulatory changes, and other factors. Always do your own research before making investment decisions.

Pioneering Protocols Making It Happen

Crediflex leads with activity-based scoring for dynamic LTVs, letting users borrow beyond collateral if their history shines. Credora, partnering on Flow Blockchain, pushes up to 200% borrowing via on-chain scores in MORE Markets. Teller Finance integrates Chainlink's DECO for hybrid on-off chain data, enabling undercollateralized loans while keeping privacy intact.

These aren't outliers. Maple Finance bridges institutions with on-chain infra, and emerging players like Wing Finance experiment similarly. As Ethereum stabilizes around $3,032.64, expect more to follow, supercharging DeFi borrowing without collateral.

I've seen wallets transform from loan-denied to power users overnight with solid scores. It's empowering - your chain actions speak louder than holdings. But how exactly do these scores translate to safer, smarter lending? That's where the real magic unfolds.

Let's break it down: these scores feed into smart contracts that adjust collateral requirements in real time. A wallet with flawless repayment history might borrow at 80% LTV, while riskier ones stick closer to 120%. Lenders win too, as scores predict defaults better than collateral alone, cutting bad debt and boosting yields. At Crypto Credit Scores, our models draw from thousands of data points to deliver just that precision.

Real-World Impact on Capital Efficiency

Picture this: with Ethereum steady at $3,032.64, a trader posts $10,000 ETH collateral. Traditional DeFi caps the loan at around $6,700. But with a top-tier on-chain score? That same collateral unlocks $12,000 or more. It's not fantasy; Credora's Flow integration already delivers 200% LTV for qualified users. This multiplies liquidity across DeFi, drawing in sidelined capital and fueling growth. I've watched portfolios balloon because users could finally leverage without overextending.

Key DeFi Loan Advantages

- Capital Efficiency: Borrowers unlock more funds with less than 150% collateral, optimizing assets for other DeFi uses like trading or staking.

- Accessibility: Opens DeFi to users without big crypto holdings, boosting financial inclusion via wallet-based credit scores.

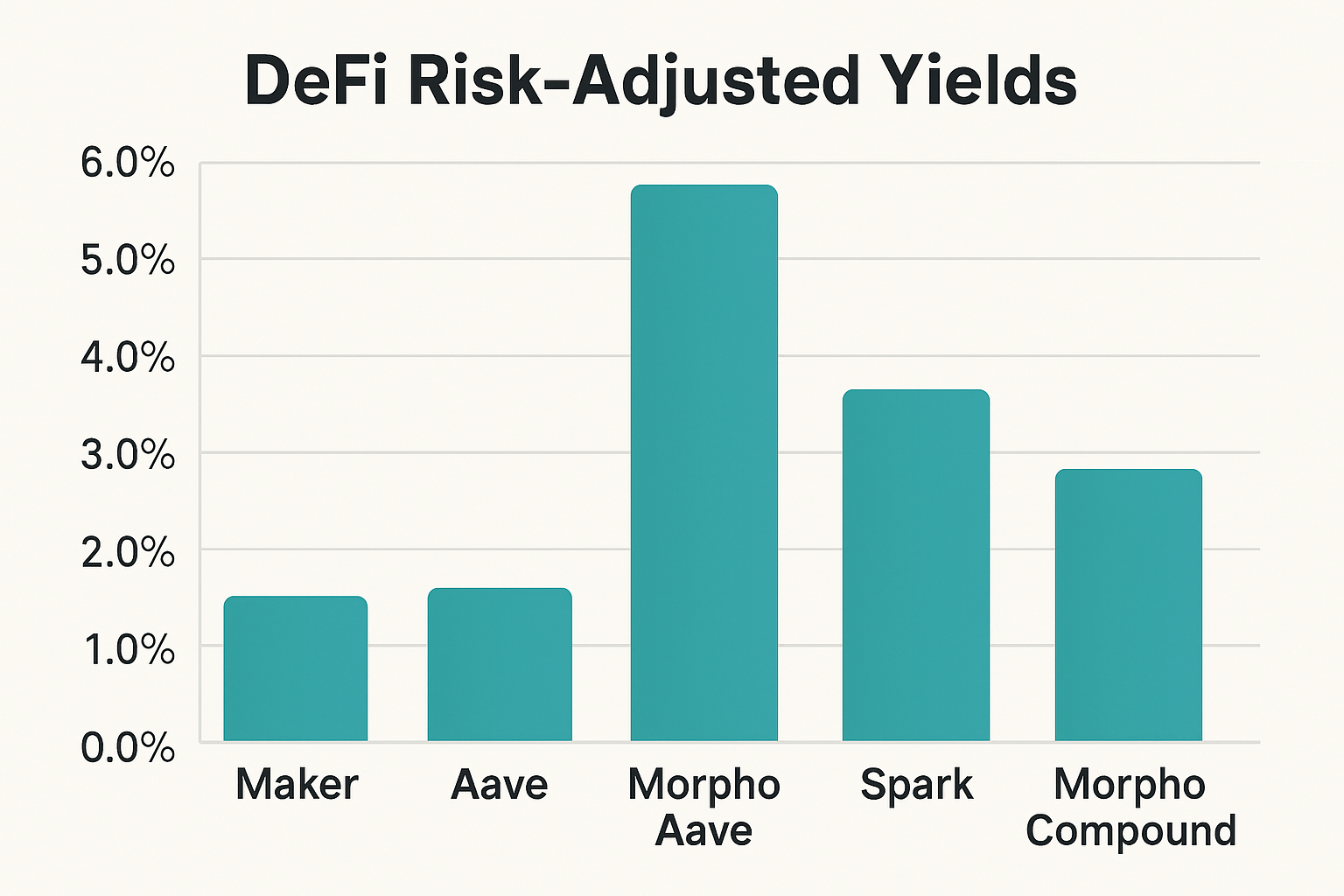

- Risk-Adjusted Yields: Lenders gain higher, smarter returns through transparent on-chain credit assessments like Credora's scores.

Skeptics worry about defaults spiking without fat collateral buffers. Fair point, but data disagrees. Protocols layer in insurance pools, oracle-monitored liquidations, and even social recovery mechanisms. Plus, on-chain transparency lets anyone audit borrower behavior, fostering community-vetted trust. It's riskier than 200% overcollateralization, sure, but calibrated scores make it sustainable - think 2-5% default rates versus 1% in CeFi, with far higher throughput.

Building and Boosting Your Score

Ready to level up? Start small: repay loans on time, diversify DeFi interactions, and maintain a mature wallet. Avoid red flags like frequent liquidations or mixer use. Platforms like ours track over 50 metrics, from borrowing velocity to peer graph analysis. Over six months, consistent activity can jump your score 30-50 points, unlocking prime borrower status. It's addictive - every tx builds equity in your DeFi passport.

Comparison of Top On-Chain Credit Protocols

| Protocol | Blockchain | Max Borrow Ratio | Key Features |

|---|---|---|---|

| Crediflex | Ethereum | Dynamic LTV (>100%) | On-chain activity-based credit scoring enabling undercollateralized loans with adjustable ratios based on user activity |

| Credora | Flow | 200% LTV | On-chain credit scores for borrowing up to 200% of collateral via collaboration with More Protocol |

| Teller | Multi-chain | Varies (undercollateralized) | Hybrid on/off-chain data using Chainlink DECO for secure, privacy-preserving credit assessment |

Of course, hurdles persist. Data silos across chains complicate scoring, and sybil attacks threaten integrity. Solutions? Cross-chain aggregators and AI anomaly detection. Privacy hawks appreciate ZK tech, but scaling it remains tricky. Still, with ETH's 24-hour range from $3,026.15 to $3,062.83 showing market maturity, DeFi's primed for this evolution.

Why This Changes Everything for DeFi

Undercollateralized lending isn't just nicer terms; it's DeFi's bridge to mainstream adoption. Billions locked in overcollateralized vaults could flood markets, supercharging yields and innovation. Lenders get institutional-grade tools without KYC headaches, borrowers gain true financial freedom. At Crypto Credit Scores, we're scaling this daily, powering protocols that trust data over deposits.

Jump in now. Connect your wallet, rack up positive signals, and watch doors open. With Ethereum at $3,032.64, the timing's perfect to turn your on-chain story into borrowing power. DeFi's future rewards the reliable - go build yours.

No comments yet. Be the first to share your thoughts!