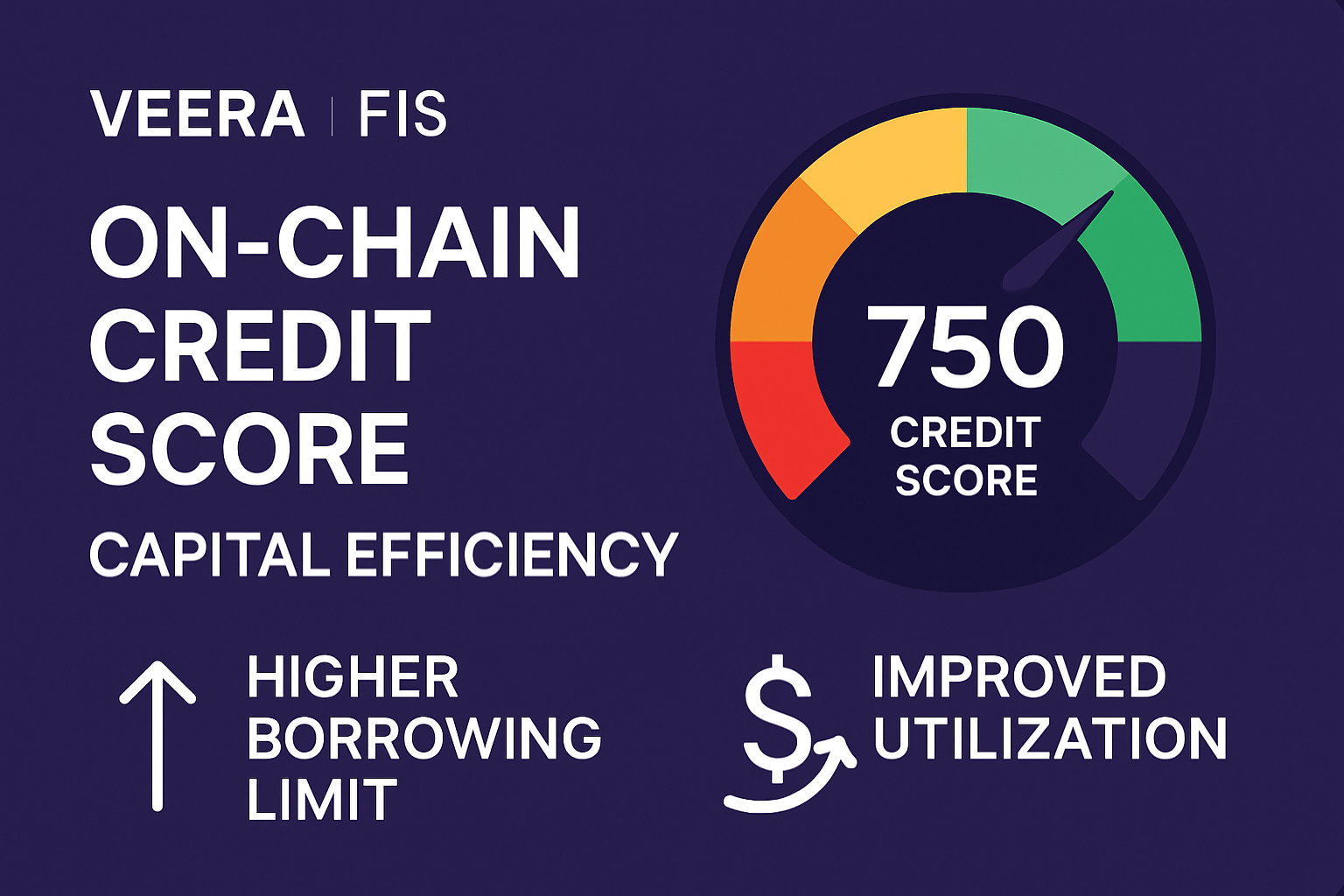

Imagine borrowing in DeFi without locking up twice the value of your loan in collateral. That's the reality on-chain credit scores like Veera FIS are making possible in 2025, transforming how we think about lending in Web3. No more overcollateralization barriers that keep everyday users sidelined; instead, your wallet's history speaks for you, opening doors to undercollateralized DeFi loans.

DeFi has exploded, but traditional lending models still demand borrowers post assets worth 150% or more of the loan. This setup works for whales with deep pockets, yet it squeezes out retail traders and newcomers. Enter blockchain credit scoring: protocols now scan your on-chain activity, from repayment patterns to protocol interactions, to gauge trustworthiness. Veera FIS stands out by routing assets through top DeFi protocols for optimal rates while building your personal Financial Identity Score.

Why Overcollateralization Holds DeFi Back

Picture this: Aave and Compound, which handled 89% of on-chain lending volume in August 2025, rely heavily on overcollateralized positions. Borrowers lock stablecoins or ETH exceeding loan amounts, tying up capital that could fuel trades or yields elsewhere. It's safe for lenders, sure, but inefficient. Capital sits idle, and users without hefty holdings can't participate. Sources like Visa highlight this as a massive untapped opportunity for stablecoin lending beyond payments.

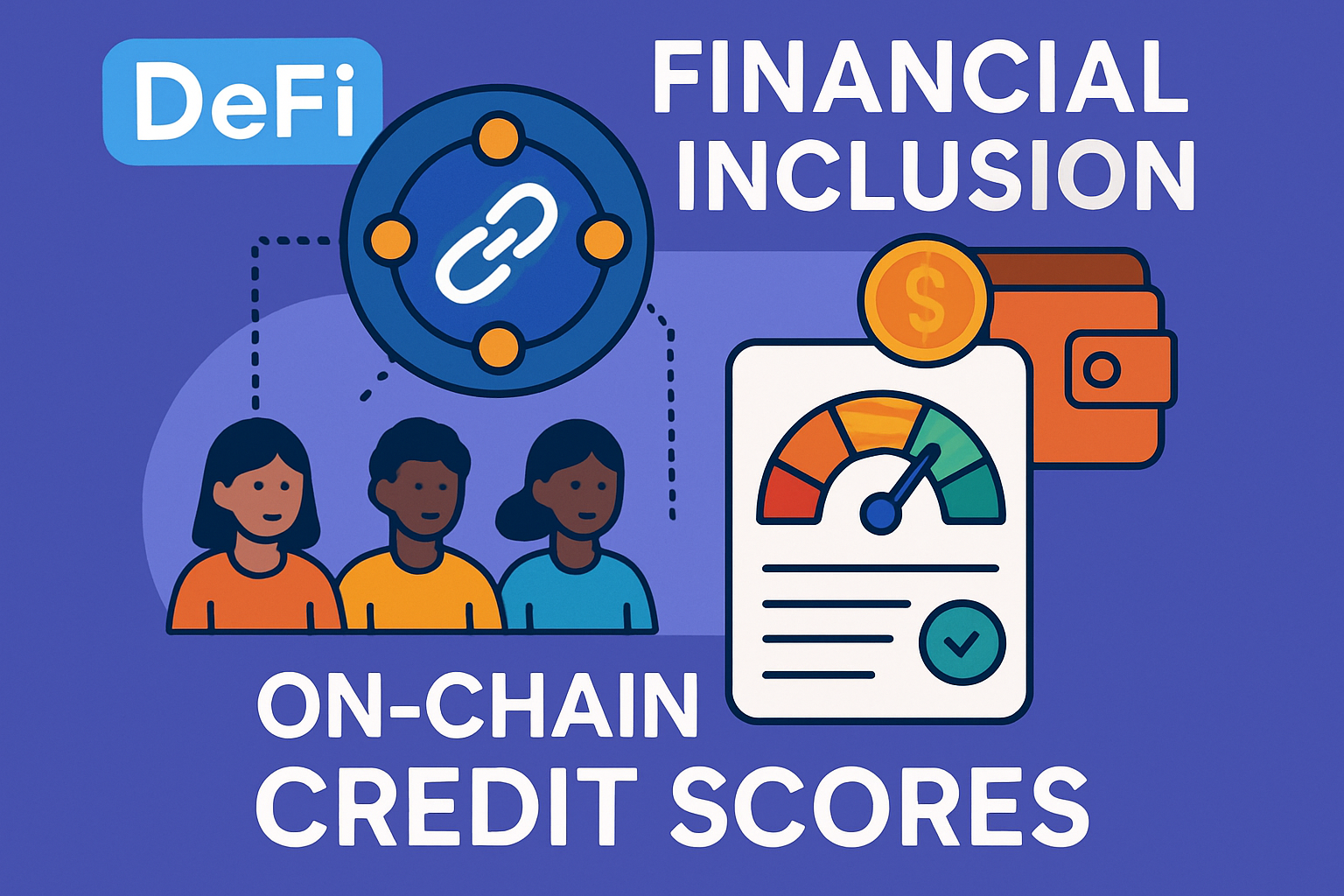

This rigidity excludes billions. On-chain data changes that. By analyzing transaction history, loan repayments, and even social proofs from protocols like Union, lenders assess real risk. No more one-size-fits-all 150% ratios; scores enable tailored terms, slashing collateral needs for proven borrowers.

Top 5 On-Chain Credit Benefits

- Higher Capital Efficiency: Ditch overcollateralization—scores like Veera FIS let you borrow with less locked assets, freeing capital for more DeFi action.

- Broader Financial Inclusion: No big crypto stash needed; on-chain history via platforms like Credora opens loans to everyday users worldwide.

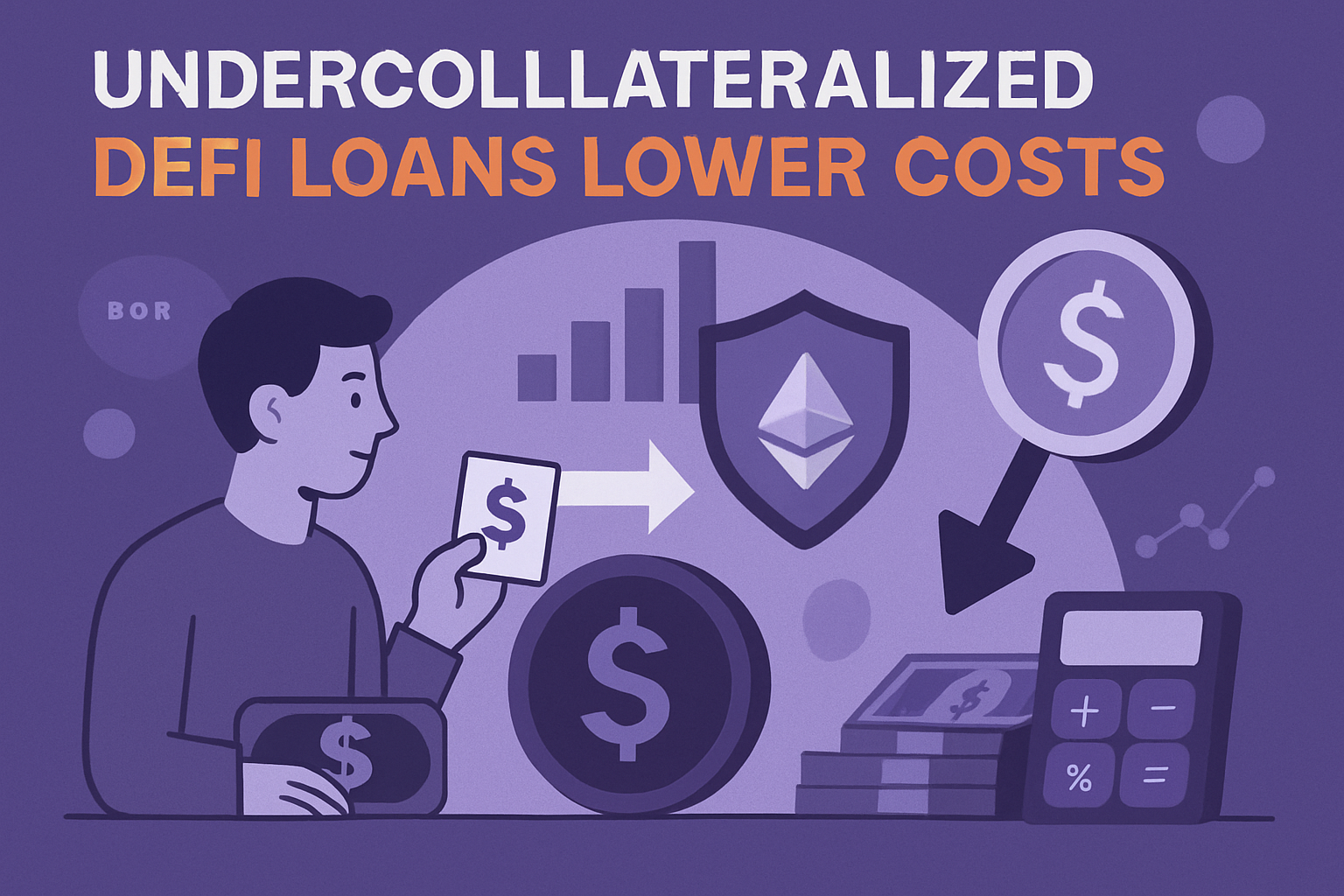

- Lower Borrowing Costs: Strong scores from protocols like RociFi mean reduced collateral and better rates, saving you money on loans.

- Privacy-Preserving Assessments: Wallet-based scoring keeps your data private while lenders like Union Protocol trust the on-chain rep.

- Real-Time Dynamic Scoring: AI-powered updates from transaction data enable instant adjustments, powering fluid lending in Aave and Compound.

Decoding On-Chain Credit Scores

At their core, on-chain credit scores are like a decentralized FICO for crypto. They pull from public blockchain data: your borrowing history, liquidity provision, NFT flips, even cross-chain behavior. Veera FIS takes it further with a holistic Financial Identity Score, factoring DeFi yield farming and repayment velocity. Decentralized credit bureaus aggregate this into standardized scores, interoperable across chains.

AI amps it up. Algorithms spot patterns humans miss, like fraud signals or loyalty to protocols, generating dynamic profiles. Platforms like Credora and RociFi use these for institutional-grade decisions. Result? Borrowers with solid scores snag loans at DeFi borrowing rates 2025 that beat CeFi, often collateral-free. It's permissionless too; any Ethereum address builds credit via Union-style accumulation.

On-chain reputation unlocks undercollateralized lending, powering fraud-resistant systems in 2025 DeFi.

Veera FIS: Pioneering the Shift

Veera FIS isn't just another score; it's your Web3 credit bureau in one. By optimizing routes across DeFi protocols, it boosts yields while scoring activity. Strong FIS? Access undercollateralized pools with minimal skin in the game. Think RociFi's reduced collateral or Union's trust-based lines, but user-friendly. As DeFi evolves, this empowers everyone from yield chasers to builders. Early adopters report smoother borrowing, proving on-chain history trumps holdings.

Check out deeper dives like how these scores cut rates or reputation powering lending. The momentum builds; trillions could flow in as scores mature.

Building a strong on-chain credit score starts with consistent activity, and Veera FIS makes it straightforward by rewarding everyday DeFi moves. I've seen users jump from sidelined to favored borrower just by stacking small wins like timely repayments and diversified interactions. It's not about how much you hold; it's about how you behave on-chain.

Steps to Boost Your Veera FIS and Unlock Loans

Follow those steps, and watch your Financial Identity Score climb. Protocols like RociFi already slash collateral for high scorers, sometimes down to 20% or less. Union's permissionless credit lines let any address accrue limits over time, no KYC nonsense. This shifts power to users; lenders compete on terms, driving down DeFi borrowing rates 2025 across the board.

But let's get real about the numbers. Overcollateralized loans tie up billions in idle capital, while undercollateralized ones free it for rotation. Aave and Compound still dominate at 89% volume, yet newcomers like those powered by Credora are carving niches with score-based pools. Borrowers build equity in their reputation, turning history into leverage.

Overcollateralized vs Undercollateralized DeFi Loans

| Aspect | Overcollateralized (Aave/Compound) | Undercollateralized (Veera FIS/RociFi) |

|---|---|---|

| Collateral Ratio | 150% | 0-50% |

| Capital Efficiency | Low | High |

| Accessibility | Whales only | All users |

| Risk Model | Liquidation heavy | Score-based |

| Borrowing Cost | Higher rates | Lower dynamic rates |

That table tells the story: undercollateralized setups win on efficiency and inclusion. Sure, risks exist, like smart contract bugs or oracle fails, but on-chain scores layer in fraud detection via AI pattern spotting. Dynamic profiles adjust in real-time; miss a payment, and your score dips, prompting better behavior. Decentralized credit bureaus standardize it all, making your Web3 credit bureau score portable from Ethereum to Solana.

Take Veera FIS users who've routed assets for optimal yields; their scores reflect that savvy, qualifying for loans that fuel bigger plays. It's opinionated, but I say this beats CeFi hands down, no banks gatekeeping. Early 2025 data shows trillions in potential as stablecoin lending evolves beyond payments, per Visa insights. Protocols aggregate data openly, ensuring fairness without doxxing.

Risks and Safeguards in Play

Lenders aren't blind optimists. Scores incorporate off-chain signals where permissioned, like Credora's institutional models, blending with pure blockchain metrics. AI flags sybil attacks or wash trading, keeping pools clean. For borrowers, it's encouraging: prove yourself once, borrow freely forever. I've mentored traders who turned modest wallets into powerhouses this way.

Looking ahead, as blockchain credit scoring matures, expect AI-driven aggregators to dominate. DeFi 2025 isn't just bigger; it's smarter, with fraud-resistant undercollateralized lending as the norm. Platforms like Mitosis University predict seamless on/off-chain hybrids, pulling trillions into play. Veera FIS leads by example, proving your wallet's story unlocks real freedom.

Ready to level up? Start tracking your on-chain moves today. Your next loan might need zero collateral, all thanks to scores paving the way. Dive deeper at this guide on score-enabled lending. The DeFi revolution feels personal now.

No comments yet. Be the first to share your thoughts!