In the fast-paced world of DeFi, borrowing has always come with a hefty price tag: massive over-collateralization that ties up your assets and inflates costs. But as we hit late 2025, on-chain credit scores like Veera FIS are flipping the script. These blockchain-native tools analyze your transaction history, repayment patterns, and on-chain behavior to deliver a reliable financial identity score DeFi users can actually use. The result? Lower borrow rates without the collateral handcuffs, making DeFi lending feel more like a smart financial move than a high-stakes gamble.

The Collateral Crunch Is Fading Fast

Picture this: back in early DeFi days, you'd lock up 163% more value than your loan just to borrow stablecoins at steep rates. Fast forward to Q3 2025, and over-collateralization ratios have dropped significantly, thanks to advanced DeFi credit scoring. Galaxy Research notes lending apps now dominate over 80% of the on-chain market, dwarfing CDPs which sit at a mere 16%. This shift isn't random; it's fueled by systems like Veera FIS that let protocols gauge risk through verifiable on-chain data.

Why does this matter for your wallet? Traditional DeFi forced everyone into the same over-padded box, ignoring individual track records. Now, a strong on-chain credit score signals to lenders you're low-risk, unlocking rates that compete with CeFi without the KYC hassle. Artemis Analytics pegs average lending yields at 4.8% on Ethereum and up to 5.6% on Polygon as of mid-2025, but borrowers with top scores see even sweeter deals on the flip side.

I've seen this firsthand in my analytics work: users who build consistent habits on-chain aren't just scoring points; they're reshaping market dynamics. OAK Research reports on-chain lending TVL soaring past $120 billion, cementing it as DeFi's powerhouse sector.

Veera FIS: Building Credit Where It Counts

At its core, Veera FIS is more than a number; it's a dynamic blockchain credit bureau score that evolves with your activity. Every earn, spend, loan repayment, or investment on Veera nudges it higher. This isn't gamified fluff, it's pragmatic risk assessment baked into the blockchain. Platforms integrate it to offer tiered rates: high FIS holders snag undercollateralized loans, slashing effective costs.

Think of it as your decentralized FICO score, but transparent and tamper-proof. In a market where crypto-collateralized borrowing hit a record $73.6 billion in Q3 per IndexBox, demand for these scores explodes. Borrowers chase yields despite higher base rates, as ScienceDirect studies highlight yield-seeking behavior. Veera FIS cuts through that by personalizing access.

Boost Your Veera FIS Score in 2025

- Consistent Loan Repayments: Timely repayments on DeFi loans via Veera, such as those on Aave or Compound, build trust and directly raise your FIS score by demonstrating reliability.

- Diversified Investments: Spread assets across protocols like Morpho and networks (Ethereum, Polygon) to show balanced risk management, boosting your score as Veera rewards varied on-chain activity.

- Regular Earning Activities: Lend stablecoins on platforms integrated with Veera to earn yields (e.g., 5-10% APY on Aave), increasing your score through consistent positive cash flow and activity.

- Healthy Spending Patterns: Use Veera for everyday on-chain spends, avoiding over-borrowing, to signal financial stability and improve your FIS profile over time.

Top Platforms Riding the Wave

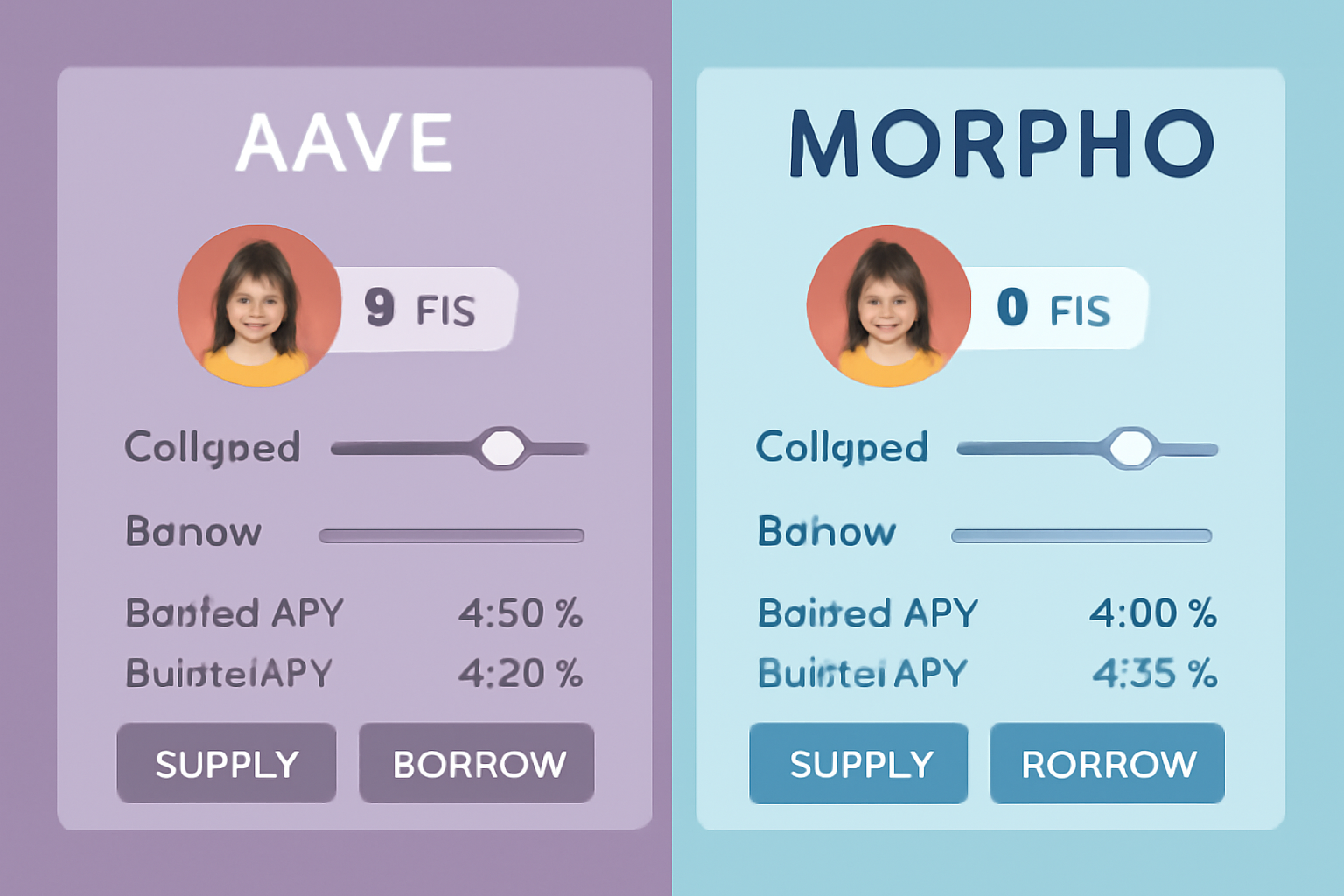

Major players are all in. Aave boasts over $9.5 billion TVL with stablecoin APYs from 5% to 10%. Compound holds $2.1 billion TVL at 3-8% APYs. Morpho? It's up 55%, smashing $41 billion ATH on better incentives and collateral options. These aren't isolated wins; ChainCatcher's leverage analysis shows on-chain lending setting records across DeFi and CeFi.

This growth ties directly to DeFi credit scoring integrations. As borrowing demand rebounded from April's deleverage dip, per CoinDesk, protocols reward scored users with prime rates. For everyday users, it means more capital efficiency: borrow more, collateralize less, and keep yields in your pocket.

Veera FIS stands out because it rewards real behavior. Want to improve on-chain score 2025? It's not about hoarding; it's active participation. Platforms like these are lowering barriers, drawing in crypto enthusiasts and institutions alike. The data backs it: P2P volumes eye half a trillion by 2027, powered by scoring tech.

Risk Meets Reward in Real Time[/h2>

Don't get me wrong, DeFi still packs risks, but on-chain scores add guardrails. Yield seekers pile into higher-rate loans, yet FIS users sidestep the worst by proving reliability upfront. Polytrade highlights how these platforms revolutionize on-chain credit, blending RWA with pure DeFi for hybrid models.

Hybrid models like these are popping up everywhere, pulling in real-world assets to back loans and further compress rates for scored borrowers. It's a pragmatic evolution: DeFi isn't ditching collateral entirely, but it's scaling it smartly based on proven behavior.

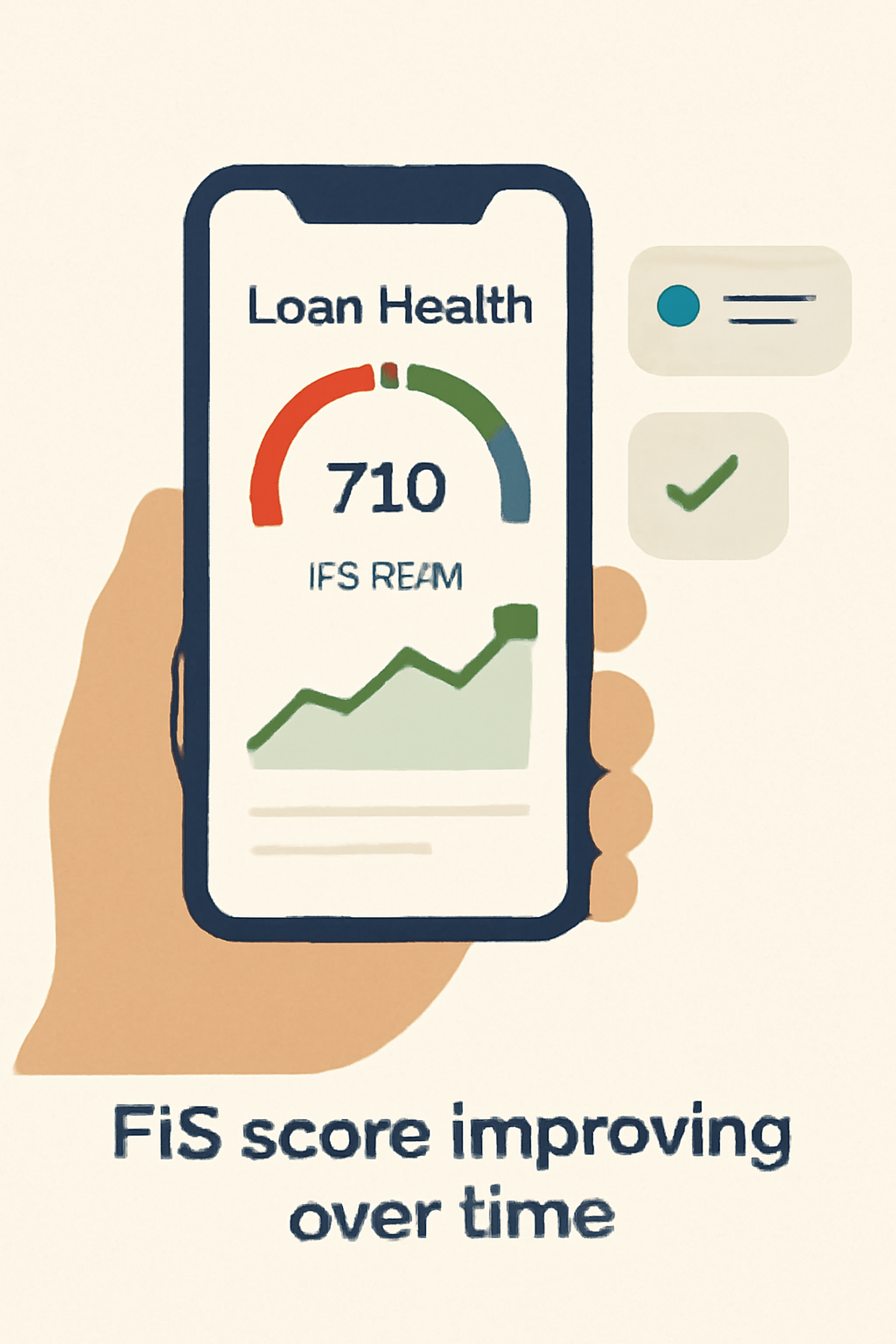

Hands-On: Boosting Your Veera FIS for Real Savings

Enough theory - let's get tactical. In my five years crunching crypto data, I've learned that improve on-chain score 2025 boils down to deliberate, trackable actions. Veera FIS rewards the grind: consistent repayments build trust, diversified investments show savvy, and steady earning keeps the score climbing. High scorers aren't lucky; they're methodical.

Unlock Lower DeFi Rates: Veera FIS Signup to Aave/Morpho Borrowing in 2025

Follow that path, and you'll see borrow rates dip below those 4.8% stablecoin averages. Platforms factor your FIS directly into pricing algorithms, so a jump from average to elite can shave 2-3% off your APR. That's not pocket change when you're leveraging $10,000 positions.

Take Morpho's surge: up 55% to $41 billion TVL on optimized collateral and incentives. Users with strong financial identity score DeFi profiles access premium pools first. Compound and Aave echo this, holding steady at $2.1 billion and $9.5 billion TVL respectively, with APYs flexing 3-10% based on demand and risk tiers. Galaxy's Q3 report underscores the dominance - lending apps at 80% of on-chain activity signals capital flowing where scores shine.

Yield Chasing Without the Crash

Yield seekers drive this market, undeterred by rates, as that ScienceDirect paper nails it. But here's my take: blind chasing leads to ruin. On-chain scores flip the script, letting you borrow aggressively yet responsibly. ChainCatcher's analysis of leverage trends across DeFi and CeFi shows records being set because protocols now distinguish signal from noise.

Artemis data from June backs the baseline yields - 4.8% Ethereum, 5.6% Polygon - but top scorers beat them handily. Over-collateralization sliding from 163% last year proves the point: DeFi credit scoring unlocks efficiency. Hedera's take on getting involved rings true - pick your market, but now with a score edge.

Glance at broader trends: OAK Research's $120 billion DeFi lending TVL cements the shift. P2P volumes barreling toward half a trillion by 2027? Credit tech like Veera FIS is the engine. Even after April's deleverage wobble, Q3 borrowing exploded to $73.6 billion, per IndexBox and CoinDesk. Confidence is back, and it's scored.

As a risk guy who's seen protocols crumble under uniform risk models, I appreciate Veera's nuance. It turns anonymous chains into accountable ecosystems. Everyday users borrow smarter, lenders deploy capital sharper, and the whole pie grows. SoluLab's peek at 2026 platforms hints at more integrations ahead.

Your move: dive into Veera, stack those on-chain wins, and watch rates melt. In DeFi's wild ride, a solid on-chain credit score is your best collateral. Knowledge - and now verifiable history - pays dividends.

No comments yet. Be the first to share your thoughts!